Reading: Lesson 3 - Capital Allocation, Financial Securities, & The Cost of Money

Completion requirements

1.3.A - Capital Allocation, Financial Securities, & The Cost of Money

1. An Overview of the Capital Allocation Process

- In the aggregate, individuals are net savers and provide most of the funds ultimately used by non-financial corporations. Although most non-financial corporations own some financial securities, such as short-term Treasury bills, non-financial corporations are net borrowers in the aggregate. In the United States federal, state, and local governments are also net borrowers in the aggregate, although many foreign governments, such as those of China and oil-producing countries, are actually net lenders. Banks and other financial corporations raise money with one hand and invest it with the other.

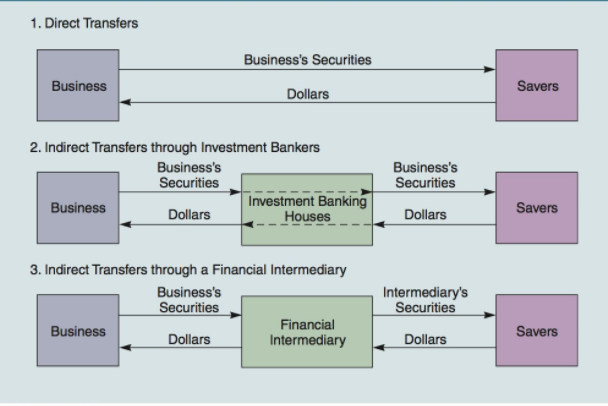

- Transfers of capital between savers and those who need capital take place in three different ways.

- Direct transfers of money and securities occur when a business (or government) sells its securities directly to savers. The business delivers its securities to savers, who in turn provide the firm with the money it needs.

- Indirect transfers may go through an investment banking house such as Goldman Sachs, which underwrites the issue. An underwriter serves as a middle-man and facilitates the issuance of securities. The company sells its stocks or bonds to the investment bank, which in turn sells these same securities to savers. Because new securities are involved and the corporation receives the proceeds of the sale, this is a “primary” market transaction.

- Transfers also can be made through a financial intermediary such as a bank or mutual fund. The intermediary obtains funds from savers in exchange for its own securities. The intermediary then uses this money to purchase and then hold businesses’ securities. For example, a saver might give dollars to a bank and receive a certificate of deposit, and then the bank might lend the money to a small business, receiving in exchange a signed loan. Thus, intermediaries literally create new types of securities.

There are three important characteristics of the capital allocation process. First, new financial securities are created. Second, financial institutions are often involved. Third, allocation between providers and users of funds occurs in financial markets.

2. Debt, Equity, or Derivatives

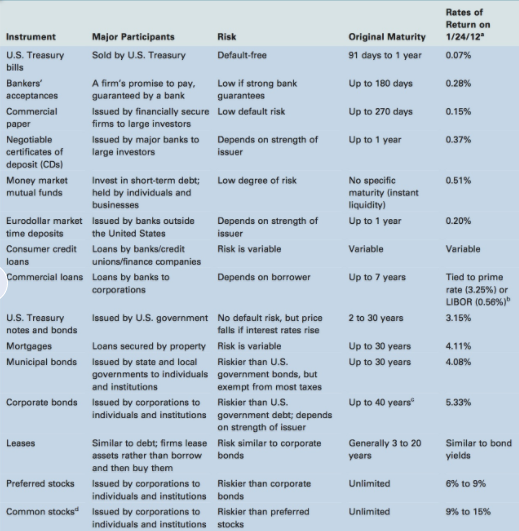

- Financial securities are simply pieces of paper with contractual provisions that entitle their owners to specific rights and claims on specific cash flows or values. Debt instruments typically have specified payments and a specified maturity. If debt matures in more than a year, it is called a capital market security. For example, an Alcoa bond might promise to pay 10% interest for 30 years, at which time it promises to make a $1,000 principal payment.

- If the debt matures in less than a year, it is a money market security. For example, Home Depot might expect to receive $300,000 in 75 days, but it needs cash now. Home Depot might issue commercial paper, which is essentially an IOU. In this example, Home Depot might agree to pay $300,000 in 75 days in exchange for $297,000 today. Thus, commercial paper is a money market security.

- Equity instruments are a claim upon a residual value. For example, Alcoa’s stockholders are entitled to the cash flows generated by Alcoa after its bondholders, creditors, and other claimants have been satisfied. Because stock has no maturity date, it is a capital market security.

- Notice that debt and equity represent claims upon the cash flows generated by real assets, such as the cash flows generated by Alcoa’s factories and operations. In contrast, derivatives are securities whose values depend on, or are derived from, the values of some other traded assets. For example, options and futures are two important types of derivatives, and their values depend on the prices of other assets. An option on Alcoa stock or a futures contract to buy pork bellies are examples of derivatives.

3. The Process of Securitization

- Many types of assets can be securitized, but we will focus on mortgages because they played such an important role in the global financial crisis. At one time, most mortgages were made by savings and loan associations (S&Ls), which took in the vast majority of their deposits from individuals who lived in nearby neighborhoods. The S&Ls pooled these deposits and then lent money to people in the neighborhood in the form of fixed-rate mortgages, which were pieces of paper signed by borrowers promising to make specified payments to the S&L. The new homeowners paid principal and interest to the S&L, which then paid interest to its depositors and reinvested the principal repayments in other mortgages. This was clearly better than having individuals lend directly to aspiring homeowners, because a single individual might not have enough money to finance an entire house or the expertise to know if the borrower was creditworthy. Note that the S&Ls were government-chartered institutions. They obtained money in the form of immediately withdrawable deposits and then invested most of it in the form of mortgages with fixed interest rates and on individual homes. Also, initially the S&Ls were not permitted to have branch operations—they were limited to one office to maintain their local orientation.

- These restrictions had important implications. First, in the 1950s there was a massive migration of people to the west, so there was a strong demand for funds in that area. However, the wealthiest savers were in the east. That meant that mortgage interest rates were much higher in California and other western states than in New York and the east. This created disequilibrium in the financial markets, something that can’t last forever.

- Second, note that the S&Ls’ assets consisted mainly of long-term, fixed-rate mortgages, but their liabilities were in the form of deposits that could be withdrawn immediately. The combination of long-term assets and short-term liabilities created another problem. If the overall level of interest rates increased, the S&Ls would have to increase the rates they paid on deposits or else savers would take their money elsewhere. However, the S&Ls couldn’t increase the rates on their outstanding mortgages because these mortgages had fixed interest rates. This problem came to a head in the 1960s, when the Vietnam War led to inflation, which pushed up interest rates. At this point, the “money market fund” industry was born, and it literally sucked money out of the S&Ls, forcing many of them into bankruptcy.

- The government responded by giving the S&Ls broader lending powers, permitting nationwide branching and allowing them to obtain funds as long-term debt in addition to immediately withdrawable deposits. Unfortunately, these changes had another set of unintended consequences. S&L managers who had previously dealt with a limited array of investments and funding choices in local communities could suddenly expand their scope of operations. Many of these inexperienced S&L managers made poor business decisions and the result was disastrous—virtually the entire S&L industry collapsed, with many S&Ls going bankrupt or being acquired in shotgun mergers with commercial banks.

- The demise of the S&Ls created another financial disequilibrium—a higher demand for mortgages than the supply of available funds from the mortgage lending industry. Savings were accumulating in pension funds, insurance companies, and other institutions, not in S&Ls and banks, the traditional mortgage lenders. This situation led to the development of “mortgage securitization,” a process whereby banks, the remaining S&Ls, and specialized mortgage-originating firms would originate mortgages and then sell them to investment banks, which would bundle them into packages and then use these packages as collateral for bonds that could be sold to pension funds, insurance companies, and other institutional investors. Thus, individual loans were bundled and then used to back a bond—a “security”—that could be traded in the financial markets.

- Congress facilitated this process by creating two stockholder-owned but government-sponsored entities, the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac). Fannie Mae and Freddie Mac were financed by issuing a relatively small amount of stock and a huge amount of debt.

- To illustrate the securitization process, suppose an S&L or bank is paying its depositors 5% but is charging its borrowers 8% on their mortgages. The S&L can take hundreds of these mortgages, put them in a pool, and then sell the pool to Fannie Mae. The mortgagees can still make their payments to the original S&L, which will then forward the payments (less a small handling fee) to Fannie Mae. Fannie Mae can take the mortgages it just bought, put them into a very large pool, and sell bonds backed by the pool to investors. The homeowner will pay the S&L, the S&L will forward the payment to Fannie Mae, and Fannie Mae will use the funds to pay interest on the bonds it issued, to pay dividends on its stock, and to buy additional mortgages from S&Ls, which can then make additional loans to aspiring homeowners. Notice that the mortgage risk has been shifted from Fannie Mae to the investors who now own the mortgage-backed bonds.

- How does the situation look from the perspective of the investors who own the bonds? In theory, they own a share in a large pool of mortgages from all over the country, so a problem in a particular region’s real estate market or job market won’t affect the whole pool. Therefore, their expected rate of return should be very close to the 8% rate paid by the home-owning mortgagees. (It will be a little less due to handling fees charged by the S&L and Fannie Mae and to the small amount of expected losses from the homeowners who could be expected to default on their mortgages.) These investors could have deposited their money at an S&L and earned a virtually risk-free 5%. Instead, they chose to accept more risk in hopes of the higher 8% return. Note, too, that mortgage-backed bonds are more liquid than individual mortgage loans, so the securitization process increases liquidity, which is desirable. The bottom line is that risk has been reduced by the pooling process and then allocated to those who are willing to accept it in return for a higher rate of return.

- Thus, in theory it is a win–win–win situation: More money is available for aspiring homeowners, S&Ls (and taxpayers) have less risk, and there are opportunities for investors who are willing to take on more risk to obtain higher potential returns. Although the securitization process began with mortgages, it is now being used with car loans, student loans, credit card debt, and other loans. The details vary for different assets, but the processes and benefits are similar to those with mortgage securitization: (1) increased supplies of lendable funds; (2) transfer of risk to those who are willing to bear it; and (3) increased liquidity for holders of the debt.

- Mortgage securitization was a win–win situation in theory, but as practiced in the last decade it has turned into a lose–lose situation. The demise of the S&Ls created another financial disequilibrium—a higher demand for mortgages than the supply of available funds from the mortgage lending industry. Savings were accumulating in pension funds, insurance companies, and other institutions, not in S&Ls and banks, the traditional mortgage lenders.

4. Fundamental Factors That Affect the Cost of Money

- In a free economy, capital from those with available funds is allocated through the price system to users who have a need for funds. The interaction of the providers’ supply and the users’ demand determines the cost (or price) of money, which is the rate users pay to providers. For debt, we call this price the interest rate. For equity, we call it the cost of equity, and it consists of the dividends and capital gains stockholders expect. Keep in mind that the “price” of money is a cost from a user’s perspective but a return from the provider’s point of view.

- The four most fundamental factors affecting the cost of money are (1) production opportunities, (2) time preferences for consumption, (3) risk, and (4) inflation. By production opportunities, we mean the ability to turn capital into benefits. If a business raises capital, the benefits are determined by the expected rates of return on its production opportunities. If a student borrows to finance his or her education, the benefits are higher expected future salaries (and, of course, the sheer joy of learning!). If a homeowner borrows, the benefits are the pleasure from living in his or her own home, plus any expected appreciation in the value of the home. Observe that the expected rates of return on these “production opportunities” put an upper limit on how much users can pay to providers.

- Providers can use their current funds for consumption or saving. By saving, they give up consumption now in the expectation of having more consumption in the future. If providers have a strong preference for consumption now, then it takes high interest rates to induce them to trade current consumption for future consumption. Therefore, the time preference for consumption has a major impact on the cost of money. Notice that the time preference for consumption varies for different individuals, for different age groups, and for different cultures. For example, people in Japan have a lower time preference for consumption than those in the United States, which partially explains why Japanese families tend to save more than U.S. families even though interest rates are lower in Japan.

- If the expected rate of return on an investment is risky, then providers require a higher expected return to induce them to take the extra risk, which drives up the cost of money. Inflation also leads to a higher cost of money. For example, suppose you earned 10% one year on your investment but inflation caused prices to increase by 20%. This means you can’t consume as much at the end of the year as when you originally invested your money. Obviously, if you had expected 20% inflation, you would have required a higher rate of return than 10%.

Last modified: Tuesday, August 14, 2018, 8:36 AM