Reading: Lesson 2 - Bond Valuation & Changes in Bond Values Overtime

5.2.A - Bond Valuation & Changes in Bond Values Overtime

1. Bond Valuation

- The value of any financial asset—a stock, a bond, a lease, or even a physical asset such as an apartment building or a piece of machinery—is simply the present value of the cash flows the asset is expected to produce. The cash flows from a specific bond depend on its contractual features. The following section shows the time line and cash flows for a bond.

- For a standard coupon-bearing bond, the cash flows consist of interest payments during the life of the bond plus the amount borrowed when the bond matures (usually a $1,000 par value):

The following general equation, written in several forms, can be used to find the value of any bond, Vb:

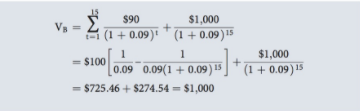

3. Recall that the firm issued a 15-year bond with an annual coupon rate of 9% and a par value of $1,000. To find the value of the firm's bond by using a formula, insert values for the firm’s bond into the equation above:

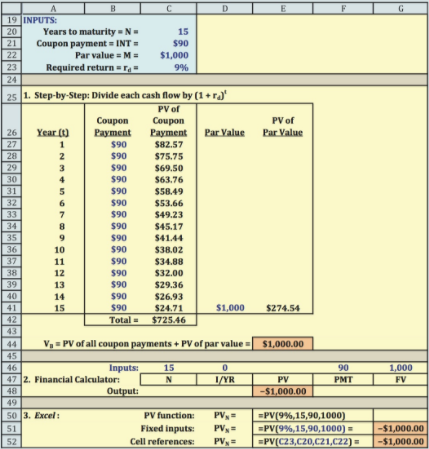

You could use the first line of Equation above to discount each cash flow back to the present and then sum these PVs to find the bond’s value of $1,000; see the figure above. This procedure is not very efficient, especially if the bond has many years to maturity. Alternatively, you could use the formula in the second line of the equation above with a simple or scientific calculator. As shown in the third line of the equation above, the total bond value of $1,000 is the sum of the coupons’ present values ($725.46) and the par value’s present value ($274.54). This is easier than the step-by-step approach, but it is still somewhat cumbersome.

A financial calculator is ideally suited for finding bond values:

4. InputN=15,I/YR=rd =9,INT=PMT=90,andM=FV=1000;thenpressthePV key to find the value of the bond, $1,000. Because the PV is an outflow to the investor, it is shown with a negative sign. The calculator is programmed to solve Equation above: It finds the PV of an annuity of $100 per year for 15 years, discounted at 10%, then it finds the PV of the $1,000 maturity payment, and then it adds these two PVs to find the value of the bond. Notice that even though the bond has a total cash flow of $1,090 at Year 15, you should not enter FV = 1090! When you entered N = 15 and PMT = 90, you told the calculator that there is a $90 payment at Year 15. Thus, setting FV = 1000 accounts for any extra payment at Year 15, above and beyond the $90 payment. With Excel, it is easiest to use the PV function: =PV(I,N,PMT,FV,0). For MicroDrive’s bond, the function is =PV(0.09,15,90,1000,0) with a result of −$1,000. Like the financial calculator solution, the bond value is negative because PMT and FV are positive. Excel also provides specialized functions for bond prices based on actual dates. For example, in Excel you could find the firm's bond value as of the date it was issued by using the function wizard to enter this formula:

= PRICE(DATE(2013,1,5),DATE(2028,1,5),9%,9%,100,1,1)

2. Interest Rate Changes and Bond Prices

- In this example, the firm’s bond is selling at a price equal to its par value. Whenever the going market rate of interest, rd, is equal to the coupon rate, a fixed-rate bond will sell at its par value. Normally, the coupon rate is set at the going rate when a bond is issued, causing it to sell at par initially. The coupon rate remains fixed after the bond is issued, but interest rates in the market move up and down. Looking at Equation above, we see that an increase in the market interest rate (rd) will cause the price of an outstanding bond to fall, whereas a decrease in rates will cause the bond’s price to rise. For example, if the market interest rate on the firm’s bond increased by 5 percentage points to 14% immediately after it was issued, we would recalculate the price with the new market interest rate as follows:

2. The price would fall to $692.89. Notice that the bond would then sell at a price below its par value. Whenever the going rate of interest rises above the coupon rate, a fixed-rate bond’s price will fall below its par value, and it is called a discount bond. On the other hand, bond prices rise when market interest rates fall. For example, if the market interest rate on the firm’s bond decreased by 5 percentage points to 4%, then we would once again recalculate its price:

In this case, the price rises to $1,555.92. In general, whenever the going interest rate falls below the coupon rate, a fixed-rate bond’s price will rise above its par value, and it is called a premium bond.

3. Changes in Bond Values Over Time

- At the time a coupon bond is issued, the coupon is generally set at a level that will cause the market price of the bond to equal its par value. If a lower coupon were set, investors would not be willing to pay $1,000 for the bond, and if a higher coupon were set, investors would clamor for the bond and bid its price up over $1,000. Investment bankers can judge quite precisely the coupon rate that will cause a bond to sell at its $1,000 par value.

- A bond that has just been issued is known as a new issue. (Investment bankers classify a bond as a new issue for about a month after it has first been issued. New issues are usually actively traded and are called “on-the-run” bonds.) Once the bond has been on the market for a while, it is classified as an outstanding bond, also called a seasoned issue. Newly issued bonds generally sell very close to par, but the prices of seasoned bonds vary widely from par. Except for floating-rate bonds, coupon payments are constant, so when economic conditions change, a 9% coupon bond with a $90 coupon that sold at par when it was issued will sell for more or less than $1,000 thereafter.

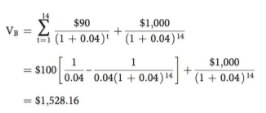

- The firm’s bonds with a 9% coupon rate were originally issued at par. If rd remained constant at 9%, what would the value of the bond be 1 year after it was issued? Now the term to maturity is only 14 years—that is, N = 14. With a financial calculator, just override N = 15 with N = 14, press the PV key, and you find a value of $1,000. If we continued, setting N = 13, N = 12, and so forth, we would see that the value of the bond will remain at $1,000 as long as the going interest rate remains equal to the coupon rate, 9%. Now suppose interest rates in the economy fell after the firm's bonds were issued and, as a result, rd fell below the coupon rate, decreasing from 9% to 4%. Both the coupon interest payments and the maturity value remain constant, but now 4% would have to be used for rd in the equation below. The value of the bond at the end of the first year would be $1,494.93:

With a financial calculator, just change rd = I/YR from 9 to 4, and then press the PV key to get the answer, $1,528.16. Thus, if rd fell below the coupon rate, the bond would sell above par, or at a premium. The arithmetic of the bond value increase should be clear, but what is the logic behind it? Because rd has fallen to 4%, with $1,000 to invest you could buy new bonds like the firm’s (every day some 10 to 12 companies sell new bonds), except that these new bonds would pay $40 of interest each year rather than $90. Naturally, you would prefer $90 to $40, so you would be willing to pay more than $1,000 for a firm's bond to obtain its higher coupons. All investors would react similarly; as a result, the firms bonds would be bid up in price to $1,528.16, at which point they would provide the same 4% rate of return to a potential investor as the new bonds.

4. Assuming that interest rates remain constant at 4% for the next 14 years, what would happen to the value of a firm's bond? It would fall gradually from $1,528.16 to $1,000 at maturity, when the firm will redeem each bond for $1,000. This point can be illustrated by calculating the value of the bond 1 year later, when it has 13 years remaining to maturity. With a financial calculator, simply input the values for N, I/YR, PMT, and FV, now using N = 13, and press the PV key to find the value of the bond, $1,499.28. Thus, the value of the bond will have fallen from $1,528.16 to $1,499.28, or by $28.88. If you were to calculate the value of the bond at other future dates, the price would continue to fall as the maturity date approached.

5. Note that if you purchased the bond at a price of $1,528.16 and then sold it 1 year later with rd still at 4%, you would have a capital loss of 28.88, or a total dollar return of $90.00 − $28.88 = $61.12. Your percentage rate of return would consist of the rate of return due to the interest payment (called the current yield) and the rate of return due to the price change (called the capital gains yield). This total rate of return is often called the bond yield, and it is calculated as follows:

6. Had interest rates risen from 9% to 14% during the first year after issue (rather than falling from 9% to 4%), then you would enter N = 14, I/YR = 14, PMT = 90, and FV = 1000, and then press the PV key to find the value of the bond, $699.90. In this case, the bond would sell below its par value, or at a discount. The total expected future return on the bond would again consist of an expected return due to interest and an expected return due to capital gains or capital losses. In this situation, the capital gains yield would be positive. The total return would be 14%. To see this, calculate the price of the bond with 13 years left to maturity, assuming that interest rates remain at 14%. With a calculator, enter N = 13, I/YR = 15, PMT = 90, and FV = 1000; then press PV to obtain the bond’s value, $707.88. Note that the capital gain for the year is the difference between the bond’s value at Year 2 (with 13 years remaining) and the bond’s value at Year 1 (with 14 years remaining), or $707.88 − $699.90 = $7.98. The interest yield, capital gains yield, and total yield are calculated as follows:

7. The figure below graphs the value of the bond over time, assuming that interest rates in the economy (1) remain constant at 9%, (2) fall to 4% and then remain constant at that level, or (3) rise to 14% and remain constant at that level. Of course, if interest rates do not remain constant, then the price of the bond will fluctuate. However, regardless of what future interest rates do, the bond’s price will approach $1,000 as it nears the maturity date (barring bankruptcy, which might cause the bond’s value to fall dramatically).

1.Whenever the going rate of interest, rd, is equal to the coupon rate, a fixed-rate bond will sell at its par value. Normally, the coupon rate is set equal to the going rate when a bond is issued, causing it to sell at par initially.

2. Interest rates do change over time, but the coupon rate remains fixed after the bond has been issued. Whenever the going rate of interest rises above the coupon rate, a fixed-rate bond’s price will fall below its par value. Such a bond is called a discount bond.

3. Whenever the going rate of interest falls below the coupon rate, a fixed-rate bond’s price will rise above its par value. Such a bond is called a premium bond.

4. Thus, an increase in interest rates will cause the prices of outstanding bonds to fall, whereas a decrease in rates will cause bond prices to rise.

5. The market value of a bond will always approach its par value as its maturity date approaches, provided the firm does not go bankrupt.

These points are very important, for they show that bondholders may suffer capital losses or make capital gains depending on whether interest rates rise or fall after the bond is purchased.