Reading: Lesson 1 - Capital Budgeting, Project Analysis & Net Present Value

Requisitos de finalización

9.1.A - Capital Budgeting, Project Analysis & Net Present Value

1. An Overview of Capital Budgeting

- In earlier sections we discussed capital budgeting. In this section capital refers to long-term assets used in production, and a budget is a plan that outlines projected expenditures during a future period. Thus, the capital budget is a summary of planned investments of assets that will last for more than a year, and capital budgeting is the whole process of analyzing projects and deciding which ones to accept and thus include in the capital budget. Chapter 10 explains the measures companies use to evaluate projects, including the measures’ strengths and weaknesses.

- A firm’s ability to remain competitive and to survive depends on a constant flow of ideas for new products, improvements in existing products, and ways to operate more efficiently. Therefore, it is vital for a company to evaluate proposed projects accurately. However, analyzing project proposals requires skill, effort, and time. For certain types of projects, an extremely detailed analysis may be warranted, whereas simpler procedures are adequate for other projects. Accordingly, firms generally categorize projects and analyze those in each category somewhat differently:

1. Replacement needed to continue profitable operations. An example would be replacing an essential pump on a profitable offshore oil platform. The platform manager could make this investment without an elaborate review process.

2. Replacement to reduce costs. An example would be the replacement of serviceable but obsolete equipment in order to lower costs. A fairly detailed analysis would be needed, with more detail required for larger expenditures.

3. Expansion of existing products or markets. These decisions require a forecast of growth in demand, so a more detailed analysis is required. Go/no-go decisions are generally made at a higher level in the organization than are replacement decisions.

4. Expansion into new products or markets. These investments involve strategic decisions that could change the fundamental nature of the business. A detailed analysis is required, and top officers make the final decision, possibly with board approval.

5. Contraction decisions. Especially during bad recessions, companies often find themselves with more capacity than they are likely to need. Rather than continue to operate plants at, say, 50% of capacity and incur losses as a result of excessive fixed costs, management decides to downsize. That generally requires payments to laid-off workers and additional costs for shutting down selected operations. These decisions are made at the board level.

6. Safety and/or environmental projects. Expenditures necessary to comply with environmental orders, labor agreements, or insurance policy terms fall into this category. How these projects are handled depends on their size, with small ones being treated much like the Category 1 projects and large ones requiring expenditures that might even cause the firm to abandon the line of business.

7. Other. This catch-all includes items such as office buildings, parking lots, and executive aircraft. How they are handled varies among companies.

8. Mergers. Buying a whole firm (or division) is different from buying a machine or building a new plant. Still, basic capital budgeting procedures are used when making merger decisions. - Relatively simple calculations, and only a few supporting documents, are required for most replacement decisions, especially maintenance investments in profitable plants. More detailed analyses are required as we move on to more complex expansion decisions, especially for investments in new products or areas. Also, within each category projects are grouped by their dollar costs: Larger investments require increasingly detailed analysis and approval at higher levels. Thus, a plant manager might be authorized to approve maintenance expenditures up to $10,000 using a simple payback analysis, but the full board of directors might have to approve decisions that involve either amounts greater than $1 million or expansions into new products or markets.

- If a firm has capable and imaginative executives and employees, and if its incentive system is working properly, then many ideas for capital investment will be forthcoming. Some ideas will be good and should be funded, but others should be killed. Therefore, the following measures have been established for screening projects and deciding which to accept or reject:

1. Net Present Value (NPV)

2. Internal Rate of Return (IRR)

3. Modified Internal Rate of Return (MIRR)

4. Profitability Index (PI)

5. Regular Payback

6. Discounted Payback - As we shall see, the NPV is the best single measure, primarily because it directly relates to the firm’s central goal of maximizing intrinsic value. However, all of the measures provide some useful information, and all are used in practice.

2. The First Step in Project Analysis

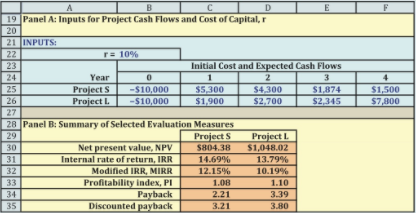

- In the sections that follow, we will evaluate two projects that Guyton Products Company (GPC) is considering. GPC is a high-tech “lab-bench-to-market” development company that takes cutting-edge research advances and translates them into consumer products. GPC has recently licensed a nano-fabrication coating technology from a university that promises to significantly increase the efficiency with which solar energy can be harvested and stored as heat. GPC is considering using this technology in two different product lines. In the first, code-named “Project S” for “solid,” the technology would be used to coat rock and concrete structures to be used as passive heat sinks and sources for energy- efficient residential and commercial buildings. In the second, code-named “Project L” for “liquid,” it would be used to coat the collectors in a high-efficiency solar water heater. GPC must decide whether to undertake either of these two projects.

- The first step in project analysis is to estimate the project’s expected cash flows. We will explain cash flow estimation for Project L , including the impact of depreciation, taxes, and salvage values. However, we want to focus now on the six evaluation measures, so we will specify the cash flows used in the following examples.

- A company’s weighted average cost of capital (WACC) reflects the average risk of all the company’s projects and that the appropriate cost of capital for a particular project may differ from the company’s WACC. In an earlier section we explained how to estimate a project’s risk-adjusted cost of capital, but for now assume that Projects L and S are equally risky and both have a 10% cost of capital. The Figure below shows the inputs for GPC’s Projects S and L, including the projects’ cost of capital and the time line of expected cash flows (with the initial cost shown at Year 0). Although Projects S and L are GPC’s “solid” and “liquid” coating projects, you may also find it helpful to think of S and L as standing for Short and Long. Project S is a short-term project in the sense that its biggest cash inflows occur relatively soon; Project L has more total cash inflows, but its largest cash flows occur in the later years.

3. Net Present Value (NPV)

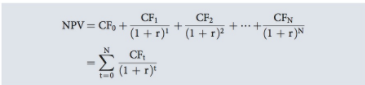

- The net present value (NPV) is defined as the present value of a project’s expected cash flows (including its initial cost) discounted at the appropriate risk-adjusted rate. The NPV measures how much wealth the project contributes to shareholders. When deciding which projects to accept, NPV is generally regarded as the best single criterion.

- We can calculate NPV with the following steps.

1. Calculate the present value of each cash flow discounted at the project’s risk-adjusted cost of capital, which is r = 10% in our example.

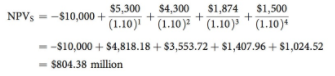

2. The sum of the discounted cash flows is defined as the project’s NPV. The equation for the NPV, set up with input data for Project S, is

Applying the Equation above to Project S, we have

Here CFt is the expected net cash flow at Time t, r is the project’s risk-adjusted cost of capital (or WACC), and N is its life. Projects generally require an initial investment—for example, developing the product, buying the equipment needed to make it, building a factory, and stocking inventory. The initial investment is a negative cash flow. For Projects S and L, only CF0 is negative; large projects often have outflows for several years before cash inflows begin.

4. Applying NPV as an Evaluation Measure

- Before using these NPVs in the decision process, we need to know whether Projects S and L are independent or mutually exclusive. The cash flows for independent projects are not affected by other projects. For example, if Walmart were considering a new store in Boise and another in Atlanta, those projects would be independent. If both had positive NPVs, Walmart should accept both.

- Mutually exclusive projects, on the other hand, are two different ways of accomplishing the same result, so if one project is accepted then the other must be rejected. A conveyor- belt system to move goods in a warehouse and a fleet of forklifts for the same purpose would be mutually exclusive—accepting one implies rejecting the other.

- What should the decision be if Projects S and L are independent? In this case, both should be accepted because both have positive NPVs and thus add value to the firm. However, if they are mutually exclusive, then Project L should be chosen because it has the higher NPV and thus adds more value than S. We can summarize these criteria with the following rules:

1. Independent projects: If NPV exceeds zero, accept the project. Because S and L both have positive NPVs, accept them both if they are independent.

2. Mutually exclusive projects: Accept the project with the highest positive NPV. If no project has a positive NPV, then reject them all. If S and L are mutually exclusive, the NPV criterion would select L. - Projects must be either independent or mutually exclusive, so one or the other of these rules applies to every project.

Última modificación: martes, 14 de agosto de 2018, 08:51