Reading: Lesson 1 - Cash Distributions

1. An Overview of Cash Distributions

- Because a company’s value depends on its ability to generate free cash flow (FCF), most of this book has focused on aspects of FCF generation, including measurement, forecasts, and risk analysis. In contrast, this chapter focuses on the use of FCF for cash distributions to shareholders. Here are the central issues addressed in this chapter: Can a company increase its value through its choice of distribution policy, defined as (1) the level of distributions, (2) the form of distributions (cash dividends versus stock repurchases), and (3) the stability of distributions? Do different groups of shareholders prefer one form of distribution over the other? Do shareholders perceive distributions as signals regarding a firm’s risk and expected future free cash flows? Before addressing these questions, let’s take a look at the big picture regarding cash distributions.

- A company must have cash before it can make a cash distribution to shareholders, we will examine a company’s sources of cash.

- Occasionally the cash comes from a recapitalization or the sale of an asset, but in most cases it comes from the company’s internally generated free cash flow. Recall that FCF is defined as the amount of cash flow available for distribution to investors after expenses, taxes, and the necessary investments in operating capital. Thus, the source of FCF depends on a company’s investment opportunities and its effectiveness in turning those opportunities into realities. Notice that a company with many opportunities will have large investments in operating capital and might have negative FCF even if it is profitable. When growth begins to slow, a profitable company’s FCF will be positive and very large. Home Depot and Microsoft are good examples of once-fast-growing companies that are now generating large amounts of free cash flows.

- There are only five potentially “good” ways to use free cash flow: (1) pay interest expenses (after tax), (2) pay down the principal on debt, (3) pay dividends, (4) repurchase stock, or (5) buy short-term investments or other non-operating assets. If a company’s FCF is negative, then its “uses” of FCF must also be negative. For example, a growing company often issues new debt rather than repaying debt and issues new shares of stock rather than repurchasing outstanding shares. Even after FCF becomes positive, some of its “uses” can be negative, as we explain next.

- A company’s capital structure choice determines its payments for interest expenses and debt principal. A company’s value typically increases over time, even if the company is mature, which implies its debt will also increase over time if the company maintains a target capital structure. If a company instead were to pay off its debt, then it would lose valuable tax shields associated with the deductibility of interest expenses. Therefore, most companies make net additions to debt over time rather than net repayments, even if FCF is positive. The addition of debt is a “negative use” of FCF, which provides even more FCF for other uses.

- A company’s working capital policies determine its level of short-term investments, such as T-bills or other marketable securities.Recognize that the decision involves a trade-off between the benefits and costs of holding a large amount of short-term investments. In terms of benefits, a large holding reduces the risk of financial distress should there be an economic downturn. Also, if growth opportunities turn out to be better than expected, short-term investments provide a ready source of funding that does not incur the flotation or signaling costs due to raising external funds. However, there is a potential agency cost: If a company has a large investment in marketable securities, then managers might be tempted to squander the money on perks (such as corporate jets) or high-priced acquisitions.

- However, many companies have much bigger short-term investments than the previous reasons can explain. For example, Apple has over $100 billion and Microsoft has about $60 billion. The most rational explanation is that such companies are using short-term investments temporarily until deciding how to use the cash.

- Purchasing short-term investments is a positive use of FCF, and selling short-term investments is negative use. If a particular use of FCF is negative, then some other use must be larger than it otherwise would have been.

- In summary, a company’s investment opportunities and operating plans determine its level of FCF. The company’s capital structure policy determines the amount of debt and interest payments. Working capital policy determines the investment in marketable securities. The remaining FCF should be distributed to shareholders, with the only question being how much to distribute in the form of dividends versus stock repurchases.

- Obviously this is a simplification, because companies (1) sometimes scale back their operating plans for sales and asset growth if such reductions are needed to maintain an existing dividend, (2) temporarily adjust their current financing mix in response to market conditions, and (3) often use marketable securities as shock absorbers for fluctuations in short-term cash flows. Still, there is an interdependence among operating plans (which have the biggest impact on free cash flow), financing plans (which have the biggest impact on the cost of capital), working capital policies (which determine the target level of marketable securities), and shareholder distributions.

2. Procedures for Cash Distributions

- Companies can distribute cash to shareholders via cash dividends or stock repurchases. In this section we describe the actual procedures used to make cash distributions.

- Companies normally pay dividends quarterly, and, if conditions permit, increase the dividend once each year. For example, Katz Corporation paid a $0.50 dividend per share in each quarter of 2013, for an annual dividend per share of $2.00. In common financial parlance, we say that in 2013 Katz’s regular quarterly dividend was $0.50, and its annual dividend was $2.00. In late 2013, Katz’s board of directors met, reviewed projections for 2014, and decided to keep the 2014 dividend at $2.00. The directors announced the $2 rate, so stockholders could count on receiving it unless the company experienced unanticipated operating problems.

- The actual payment procedure is as follows.

1. Declaration date. On the declaration date—say, on Thursday, November 14—the directors meet and declare the regular dividend, issuing a statement similar to the following: “On November 14, 2013, the directors of Katz Corporation met and declared the regular quarterly dividend of 50 cents per share, payable to holders of record as of Friday, December 13, payment to be made on Friday, January 3, 2014.” For accounting purposes, the declared dividend becomes an actual liability on the declaration date. If a balance sheet were constructed, an amount equal to $0.50 × n0, where n0 is the number of shares outstanding, would appear as a current liability, and retained earnings would be reduced by a like amount.

2. Holder-of-record date. At the close of business on the holder-of-record date, December 13, the company closes its stock transfer books and makes up a list of shareholders as of that date. If Katz Corporation is notified of the sale before 5 p.m. on December 13, then the new owner receives the dividend. However, if notification is received after 5 p.m. on December 13, the previous owner gets the dividend check.

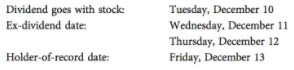

3. Ex-dividend date. Suppose Jean Buyer buys 100 shares of stock from John Seller on December 10. Will the company be notified of the transfer in time to list Buyer as the new owner and thus pay the dividend to her? To avoid conflict, the securities industry has set up a convention under which the right to the dividend remains with the stock until two business days prior to the holder-of-record date; on the second day before that date, the right to the dividend no longer goes with the shares. The date when the right to the dividend leaves the stock is called the ex-dividend date. In this case, the ex-dividend date is two days prior to December 13, which is December 11:

Therefore, if Buyer is to receive the dividend, she must buy the stock on or before December 10. If she buys it on December 11 or later, Seller will receive the dividend because he will be the official holder of record. Katz’s dividend amounts to $0.50, so the ex-dividend date is important. Barring fluctuations in the stock market, we would normally expect the price of a stock to drop by approximately the amount of the dividend on the ex-dividend date. Thus, if Katz closed at $30.50 on December 10, it would probably open at about $30 on December 11. 4. Payment date. The company actually pays the dividend on January 3, the payment date, to the holders of record.

4. Payment date. The company actually pays the dividend on January 3, the payment date, to the holders of record.

3. Stock Repurchase Procedures

- Stock repurchases occur when a company buys back some of its own outstanding stock. Three situations can lead to stock repurchases. First, a company may decide to increase its leverage by issuing debt and using the proceeds to repurchase stock; we discuss recapitalizations in more detail in Chapter 15. Second, many firms have given their employees stock options, and companies often repurchase their own stock to sell to employees when employees exercise the options. In this case, the number of outstanding shares reverts to its pre-repurchase level after the options are exercised. Third, a company may have excess cash. This may be due to a one-time cash inflow, such as the sale of a division, or the company may simply be generating more free cash flow than it needs to service its debt.

- Stock repurchases are usually made in one of three ways. (1) A publicly owned firm can buy back its own stock through a broker on the open market. (2) The firm can make a tender offer, under which it permits stockholders to send in (that is, “tender”) shares in exchange for a specified price per share. In this case, the firm generally indicates it will buy up to a specified number of shares within a stated time period (usually about two weeks). If more shares are tendered than the company wants to buy, purchases are made on a pro rata basis. (3) The firm can purchase a block of shares from one large holder on a negotiated basis. This is a targeted stock repurchase.

4. Patterns of Cash Distributions

- e occurrence of dividends versus stock repurchases has changed dramatically during the past 30 years. First, total cash distributions as a percentage of net income have remained fairly stable at around 26% to 28%, but the mix of dividends and repurchases has changed. The average dividend payout ratio fell from 22.3% in 1974 to 13.8% in 1998, while the average repurchase payout as a percentage of net income rose from 3.7% to 13.6%. Since 1985, large companies have repurchased more shares than they have issued. Since 1998, more cash has been returned to shareholders in repurchases than as dividend payments.

- Second, companies today are less likely to pay a dividend. In 1978, about 66.5% of NYSE, AMEX, and NASDAQ firms paid a dividend. In 1999, only 20.8% paid a dividend. Part of this reduction can be explained by the large number of IPOs in the 1990s, because young firms rarely pay a dividend. However, that doesn’t explain the entire story, as many mature firms now do not pay dividends. For example, consider the way in which a maturing firm will make its first cash distribution. In 1973, 73% of firms making an initial distribution did so with a dividend. By 1998, only 19% initiated distributions with dividends.

- Third, the aggregate dividend payouts have become more concentrated in the sense that a relatively small number of older, more established, and more profitable firms accounts for most of the cash distributed as dividends.

- Fourth, the Table below shows there is considerable variation in distribution policies, with some companies paying a high percentage of their income as dividends and others paying none. The next section discusses some theories about distribution policies.