Reading: Lesson 6 - Anatomy of a Recapitalization

12.6.A - Anatomy of a Recapitalization

1. Anatomy of a Recapitalization

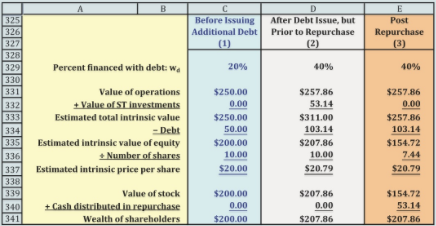

- Strasburg should recapitalize, meaning that it should issue enough additional debt to optimize its capital structure, and then use the debt proceeds to repurchase stock. As shown in a previous Figure, a capital structure with 40% debt is optimal. But before tackling the recap, as it is commonly called, let’s consider the sequence of events, starting with the situation before Strasburg issues any additional debt. Another previous Figure shows the valuation analysis of Strasburg at a capital structure consisting of 20% debt and 80% equity. These results are repeated in Column 1 of the Figure below, along with the shareholder wealth, which consists entirely of $200 million in stock before the repurchase. The next step is to examine the impact of Strasburg’s debt issuance.

The next step in the recap is to issue debt and announce the firm’s intent to repurchase stock with the newly issued debt. At the optimal capital structure of 40% debt, the value of the firm’s operations is $257.86 million as shown in the Figure above. This value of operations is greater than the $250 million value of operations for wd = 20% because the WACC is lower. Notice that Strasburg raised its debt from $50 million to $103.14 million, an increase of $53.14 million. Because Column 2 reports data prior to the repurchase, Strasburg has short-term investments in the amount of $53.14 million, the amount that was raised in the debt issuance but that has not yet been used to repurchase stock. As the Figure above shows, Strasburg’s intrinsic value of equity is $207.86 million.

Because Strasburg has not yet repurchased any stock, it still has 10 million shares outstanding. Therefore, the price per share after the debt issue but prior to the repurchase is:

Column 2 of the Figure above summarizes these calculations and also shows the wealth of the shareholders. The shareholders own Strasburg’s equity, which is worth $207.86 million. Strasburg has not yet made any cash distributions to shareholders, so the total wealth of shareholders is $207.86 million. The new wealth of $207.86 million is greater than the initial wealth of $200 million, so the recapitalization has added value to Strasburg’s shareholders. Notice also that the recapitalization caused the intrinsic stock price to increase from $20.00 to $20.79.

Summarizing these results, we see that the issuance of debt and the resulting change in the optimal capital structure caused (1) the WACC to decrease, (2) the value of operations to increase, (3) shareholder wealth to increase, and (4) the stock price to increase.

2. Strasburg Repurchases Stock

- What happens to the stock price during the repurchase? Note that a repurchase does not change the stock price. It is true that the additional debt will change the WACC and the stock price prior to the repurchase (PPrior), but the subsequent repurchase itself will not affect the post-repurchase stock price (PPost). Therefore, PPost = PPrior. (Keep in mind that PPrior is the price immediately prior to the repurchase, not the price prior to the event that led to the cash available for the repurchase, such as the issuance of debt in this example.)

- Strasburg uses the entire amount of cash raised by the debt issue to repurchase stock. The total cash raised is equal to DNew − DOld. The number of shares repurchased is equal to the cash raised by issuing debt divided by the repurchase price:

Strasburg repurchases ($103.14 − $50)/$20.79 = 2.56 million shares of stock. The number of remaining shares after the repurchase, nPost, is equal to the initial number of shares minus the number that is repurchased:

For Strasburg, the number of remaining shares after the repurchase is

Column 3 of the Figure above summarizes these post-repurchase results. The repurchase doesn’t change the value of operations, which remains at $257.86 million. However, the short-term investments are sold and the cash is used to repurchase stock. Strasburg is left with no short-term investments, so the intrinsic value of equity is:

After the repurchase, Strasburg has 7.44 million shares of stock. We can verify that the intrinsic stock price has not changed:

Shareholders now own an equity position in the company worth only $154.72 million, but they have received a cash distribution in the amount of $53.14 million, so their total wealth is equal to the value of their equity plus the amount of cash they received: $154.72 + $53.14 = $207.86.

Here are some points worth noting. As shown in Column 3 of the Figure above, the change in capital structure clearly added wealth to the shareholders, increased the price per share, and increased the cash (in the form of short-term investments) temporarily held by the company. However, the repurchase itself did not affect shareholder wealth or the price per share. The repurchase did reduce the cash held by the company and the number of shares outstanding, but shareholder wealth stayed constant. After the repurchase, shareholders directly own the funds used in the repurchase; before the repurchase, shareholders indirectly own the funds. In either case, shareholders own the funds. The repurchase simply takes them out of the company’s account and puts them into the shareholders’ personal accounts.

The approach we’ve described here is based on the corporate valuation model, and it will always provide the correct value for SPost, nPost, and PPost. However, there is a quicker way to calculate these values if the firm has no short-term investments either before or after the recap (other than the temporary short-term investments held between the time debt was issued and shares repurchased). After the recap is completed, the percentage of equity in the capital structure, based on market values, is equal to 1 − wd if the firm holds no other short- term investments. Therefore, the value of equity after the repurchase is where we use the subscript “New” to indicate the value of operations at the new capital structure and the subscript “Post” to indicate the post-repurchase intrinsic value of equity.

The post-repurchase number of shares can be found using this equation:

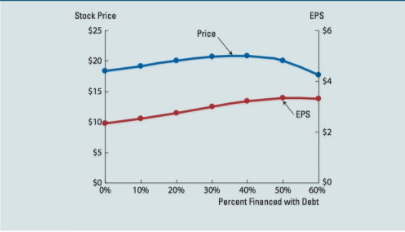

The Figure below also reports the earnings per share for the different levels of debt. The Figure below graphs the intrinsic price per share and the earnings per share. Notice that the maximum earnings per share is at 50% debt even though the optimal capital structure is at 40% debt. This means that maximizing EPS will not maximize shareholder wealth.

3. Recapitalization: A Post-Mortem

- In a previous Unit, we saw how a company can increase its value by improving its operations. There is good news and bad news regarding this connection. The good news is that small improvements in operations can lead to huge increases in value. The bad news is that it’s often difficult to improve operations, especially if the company is already well managed and is in a competitive industry.

- If instead you seek to increase a firm’s value by changing its capital structure, we again have good news and bad news. The good news is that changing capital structure is easy—just call an investment banker and issue debt (or issue equity if the firm has too much debt). The bad news is that this will add only a relatively small amount of value. Of course, any additional value is better than none, so it’s hard to understand why there are some mature firms with zero debt.

- Finally, some firms have more debt than is optimal and should recapitalize to a lower debt level. This is called deleveraging. We can use exactly the same approach and the same formulas as we used for Strasburg. The difference is that the debt will go down and the number of shares will go up. In other words, the company will issue new shares of stock and then use the proceeds to pay off debt, resulting in a capital structure with less debt and lower interest payments.