Reading: Lesson 2 - Forecasting Operations

متطلبات الإكمال

10.2.A - Forecasting Operations

1. Projecting Financial Statements

- A key output of a financial plan is the set of projected financial statements. The basic approach in projecting statements is a simple, three-step process: (1) forecast the operating items, (2) forecast the amounts of debt, equity, and dividends that are determined by the company’s preliminary short-term financial policy, and (3) ensure that the company has sufficient but not excess financing to fund the operating plan.

- Despite the simple process, projecting financial statements can be similar to peeling onions—but not because it smells bad and brings tears to your eyes! Just as there are many different onions (white, purple, large, small, sweet, sour, etc.), there are many different variations on the basic approach. And just as onions have many layers, a financial plan can have many layers of complexity. It would be impossible for us to cover all the different methods and details used when projecting financial statements, so we are going to focus on the straightforward method MicroDrive’s CFO used, which is applicable to most companies.

- Here are the three steps in this method:

1. MicroDrive will project all the operating items that are part of the operating plan.

2. For the initial forecast, MicroDrive’s CFO applied the following preliminary short-term financial policy: (1) MicroDrive will not issue any long-term bonds, preferred stock, or common stock in the upcoming year; (2) MicroDrive will not pay off or increase notes payable; and (3) MicroDrive will increase regular dividends at the sustainable long-term growth rate discussed previously in the sales forecast.

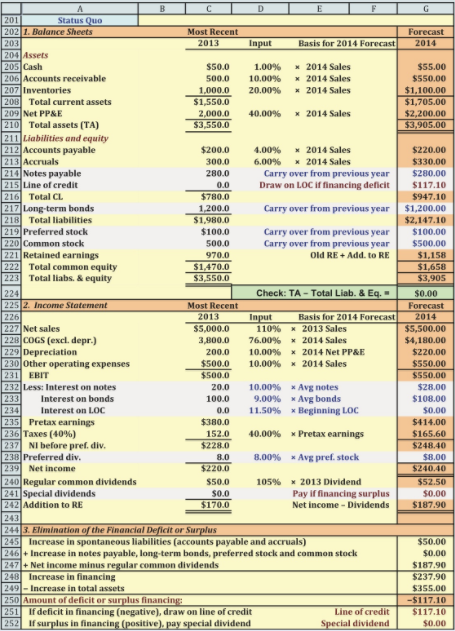

3. If the short-term financial policies described in the second step do not provide sufficient additional financing to fund the additional operating assets needed by the operating plan described in the first step, MicroDrive will draw on a special line of credit. If the financial policies provide surplus financing, MicroDrive will pay a special dividend. - The Figure below shows MicroDrive’s projected financial statements for the Status Quo scenario for the upcoming year. MicroDrive’s CFO forecast the operating plan in the previous Section, so it is an easy matter to replicate the process and forecast the corresponding operating items on the financial statement accounts. Column C shows the most recent year, Column D shows the inputs from the previous sections Figure, Columns E and F describe how the inputs are applied, and Column G shows the forecast for the upcoming year. Notice that the forecasts for the operating items in the Figure below are identical to those in the previous sections Figure.

2. Forecast Items Determined by the Preliminary Short-Term Financial Policy

- MicroDrive has a target capital structure and target dividend growth. Like most companies, MicroDrive is willing to deviate from those targets in the short term. For the purpose of this initial forecast, MicroDrive has a preliminary short- term financial policy that sets the projected values for notes payable, long-term debt, preferred stock, and common stock equal to their previous values. In other words, the preliminary short-term financial policy does not call for any change in these items. Keep in mind that financial planning is an iterative process—specify a plan, look at the results, modify if needed, and repeat the process until the plan is acceptable and achievable.

- The pale silver rows with blue print in the Figure above show the items determined by the preliminary short-term financial policy. Section 1 shows the projected balance sheets, with the projected values for notes payable, long-term debt, preferred stock, and common stock unchanged from their previous values. The basic approach for projecting financial statements would remain unchanged if the preliminary short-term financial policy had called for changes in these items, such as issuing new debt or equity. In fact, MicroDrive’s CFO plans on presenting long-term recommendations to the board regarding the possibility of issuing additional common stock, preferred stock, or long-term bonds after the preliminary forecast has been analyzed.

- Section 2 shows the projected income statement. The interest expense on notes payable is projected as the interest rate on notes payable multiplied by the average value of the notes payable outstanding during the year. For example, MicroDrive had $280 at the end of 2013 and projected $280 at the end of 2014, so the average balance during the year is $280 = ($280 + $280)/2. If MicroDrive’s plans had called for borrowing an addition $40 in notes payable during the year (resulting in an end-of-year balance of $320), the average balance would have been $300 = ($280+ $320)/2. The same process is applied to long- term bonds and preferred stock.

- Basing interest expense on the average amount of debt outstanding during the year implies that the debt is added (or repaid) smoothly during the year. However, if debt is not added until the last day of the year, that year’s interest expense should be based on just the debt at the beginning of the year (i.e., the debt at the end of the previous year), because virtually no interest would have accrued on the new debt. On the other hand, if the new debt is added on the first day of the year, interest would accrue all year, so the interest expense should be based on the amount of debt shown at the end of the year.

- MicroDrive’s preliminary short-term financial policy calls for dividend growth of 5%. The only items on the projected statements that have not been forecast by the operating plan or the preliminary short-term financial plan are the line of credit (LOC), interest on the LOC, and the item for special dividends. These are shown in dark red ink in the pale gray rows.

3. Identify and Eliminate the Financing Deficit or Surplus in the Projected Balance Sheets

- At this point in the projection, it would be extremely unlikely for the balance sheets to balance because the increase in assets required by the operating plan probably is not equal to the increase in liabilities and financing caused by the operating plan and the preliminary short-term financial policy. There will be a financing deficit if the additional financing is less than the additional assets, and a financing surplus if the additional assets are greater than the additional financing. If there is a financing deficit, MicroDrive will not be able to afford its operating plan; if there is a financing surplus, MicroDrive must use it in some manner. Therefore, a realistic projection requires balance sheets that balance.

- The first step in making the sheets balance is to identify the amount of financing surplus or deficit resulting from the operating plan and the preliminary short-term financial policy. The second step is to eliminate the deficit or surplus.

- Preliminary additional financing comes from three sources: (1) spontaneous liabilities, (2) external financing (such as issuing new long-term bonds or common equity), and (3) internal financing (which is the amount of earnings that are reinvested rather than paid out as dividends). Following is an explanation of how to calculate the additional financing for MicroDrive.

- Section 3 in the Figure above begins by adding up the additional financing in the forecast relative to the previous year. For example, MicroDrive’s spontaneous liabilities (accounts payable and accruals) went from a total of $500 to $550, an increase of $50. Due to MicroDrive’s preliminary short-term financial policy, there were no changes in the external financing provided by notes payable, long-term bonds, preferred stock, or common stock. MicroDrive’s preliminary policy calls for no changes in external financing, but it would be easy to modify this assumption. In fact, the CFO did make changes in external financing in a final plan that we discuss later. The preliminary amount of internal financing is the difference between net income and regular common dividends—this is the amount of earnings that are being reinvested. MicroDrive projects a total increase in financing of $237.9, as shown in Section 3 of the Figure above.

- Is this enough financing, too much, or just right? To answer this question, start by calculating MicroDrive’s projected increase in total assets: $355 = $3,905 − $3,550. The difference between MicroDrive’s increase in financing and its increase in projected assets is $237.9 − $355 = −$117.1. This amount is negative because the increase in MicroDrive’s projected assets is greater than the increase in MicroDrive’s projected financing. Therefore, MicroDrive has a preliminary financing deficit—MicroDrive needs more financing to support its operating plan. Had this value been positive, MicroDrive would have had a financing surplus. How should a company handle a financing deficit or surplus?

- There are an infinite number of answers to that question, which is why financial modeling can be complicated. MicroDrive’s CFO chose a simple but effective answer—if there is a deficit, draw on a line of credit even though it has a high interest rate (the rate on the LOC is 1.5 percentage points higher than the rate on notes payable); if there is a surplus, pay a special dividend. Keep in mind that this is a preliminary plan and that MicroDrive might choose a different source of financing in its final plan.

- The last two rows in Section 3 of the Figure above apply this logic. The cell for the LOC in the balance sheet in Section 1 (Cell C215) is linked to the cell in Section 3 (G251). The next step is to estimate the interest expense on the LOC. MicroDrive’s CFO made a simplifying assumption for the preliminary projection: The LOC will be drawn upon on the last day of the year. Therefore, the LOC will not accrue interest, so the interest expense on the LOC is equal to the interest rate multiplied by the balance of the LOC at the beginning of the year rather than the end of the year.

- The CFO realizes that the projected interest expense will understate the true interest expense if MicroDrive draws on the LOC earlier in the year. However, the CFO wanted to keep the model simple for the preliminary presentations at the retreat. The CFO actually made more realistic (but more complex) assumptions in another model.

آخر تعديل: الثلاثاء، 14 أغسطس 2018، 8:52 AM