Reading: Lesson 6 - Raising Capital Through Stock Sales

完成条件

8.6.A - Raising Capital Through Stock Sales

1. TYPES OF STOCK

- By far the greatest amount of equity investment in U.S. businesses comes from the sale of stock. The World Bank tracks the total amount invested in the stocks of U.S. corporations. The value in 2012 was $18.7 trillion. In 2013, 52 percent of all Americans owned stock in some form—individual stocks, stock mutual funds, or stock holdings as a part of a retirement fund. That level of investment is down from 65 percent in 2007. Corporations use several types of equity and debt financing to raise money, but about 44 percent of the total equity in the average corporation is made up of stock. Stockholders are the owners of corporations, but their ownership rights and responsibilities vary based on the type of stock they hold. Two kinds of stock are issued by corporations—common stock and preferred stock.

- Common stock is ownership that gives holders the right to participate in managing the business through voting privileges plus the right to share in any profits through dividends. Owners of common stock can vote on basic issues at the corporation’s annual meeting, including the election of the board of directors. Holders of common stock receive one vote per share of stock owned. As owners they also can share in the corporation’s profits. When the corporation makes a profit, some or all of that profit may be paid back to stockholders as dividends. The corporation’s board of directors makes the decision about whether holders of common stock will receive a dividend and the amount of any dividend per share of stock. The board of directors decides on the number of shares of common stock that will be issued by the corporation. If they decide to issue new shares, they assign a value to those shares, known as par value. The par value is somewhat arbitrary in that it may not be the price that stockholders pay for the shares. If stockholders believe the company is a good investment, they may pay more than par value. The price at which stock is actually bought and sold is its market value. The price of a share of stock goes up and down based on the financial performance of the company and general economic conditions. Investors purchase shares with the expectation that the company’s financial performance will be strong, dividends will be paid, and the share price will increase. They hope to sell the stock in the future for a much greater value than originally paid.

- Common stockholders have the right to purchase any new shares issued before they are offered for sale on the open market. That right protects the interests of the current stockholders. Otherwise it would be possible for management of the corporation to take control away from existing stockholders by issuing and purchasing a large block of new stock.

- Preferred stock is stock that gives holders first claim on corporate dividends if a company earns a profit. In addition, if a business fails, preferred stockholders have priority over common stockholders on any remaining assets after other creditors have been paid. However, preferred stockholders typically have no voting rights. A corporation must use its earnings first to pay its debts. Then some or all of the remaining profits can be used to pay dividends. Preferred stock carries a guaranteed fixed dividend. Any dividends declared by the board of directors go first to preferred stockholders, who may receive these dividend payments in future years if profits were not sufficient in the previous year. If any profits remain, the corporation can then choose to pay dividends to common stockholders.

- For example, suppose that a corporation issues $1,000,000 of 7 percent preferred stock and $1,000,000 of common stock. Further assume that dividends for the year are $100,000. The preferred stockholders would receive 7 percent of $1,000,000, or $70,000. The remaining $30,000 would be left for the holders of common stock. Their return on $1,000,000 would yield only 3 percent ($30,000/1,000,000). Even that return is not guaranteed because the board of directors may choose not to declare a dividend for common stockholders, instead keeping retained earnings. A special class of preferred stock is cumulative preferred stock. If there is no profit in a particular year, the guarantee remains in place for cumulative preferred stockholders, so the dividend will have to be made up in future years when the company is profitable again.

- A special class of preferred stock is cumulative preferred stock. If there is no profit in a particular year, the guarantee remains in place for cumulative preferred stockholders, so the dividend will have to be made up in future years when the company is profitable again. Preferred stockholders have priority over common stockholders for the company’s assets in the case of corporation failure. If the corporation ceases operations, its assets belong to its owners, the stockholders. The assets are first distributed to preferred stockholders. Any remaining assets go to common stockholders.

- What would happen if a corporation with $500,000 of outstanding common stock and $500,000 of outstanding preferred stock ceased operating? Assume that after selling all of the assets and after paying all of its creditors, $600,000 in cash remains. The sum of $500,000 (the par value of the preferred stock) must be paid to the preferred stockholders, because their stock has asset priority. As a result, the common stockholders would receive only $100,000, which is 20 percent of the full value of their stock ($100,000/$500,000). If no stock had been issued as preferred, all stockholders would share equally in the $600,000.

2. THE VALUE OF STOCK

- The original sale of stock provides equity that a company needs to operate the business. It is used to finance long-and short-term assets and pay operating expenses. Even though the value of stock may increase or decrease after the original sale, that change in value is not directly reflected in the equity resources the company has available to finance operations. The change in the price of a company’s stock is important to stockholders when they buy and sell the stock, so the company’s management wants to maximize the value of its stock to make the company attractive to investors. If a corporation wants to increase its capital, it must issue additional stock or keep profits for use in the company rather than using those profits to pay stockholder dividends.

- If an existing corporation needs additional equity and decides to raise it through the sale of new stock, known as a secondary stock issuance, that decision will need to be approved by the board of directors. Common stockholders will have the first right to purchase the stock. Stockholders will be concerned about the effect of the sale of new stock on the price of their current shares because having more shares available can lower the stock price. In addition, having more shares of a company available decreases the voting power of each share, as each share would now represent a smaller percentage of ownership. Corporations must determine the kind of stock to issue. The certificate of incorporation states whether all authorized stock is common stock or whether a proportion is common and another proportion preferred. Corporations cannot issue other stock unless they receive authorization from the state granting the corporate charter. It is usually a good practice to issue only common stock when starting a business. That provides more flexibility to the board of directors in the way they use any profits earned in the first years of the company. Even if the new corporation earns profits immediately, it is often wise to use those profits to improve the financial strength of the business, rather than distribute the profits as dividends to preferred shareholders. Although a corporation often pays dividends to holders of common stock, it is not required to do so. If the corporation issues preferred stock, however, it is obligated to pay the specified dividend from its profits. If it issues only common stock initially and later wants to expand, it may then issue preferred stock to encourage others to invest in the business. Investors may be attracted to a company whose stock price is not expected to increase only if they can be assured of a regular dividend.

- The par value of a stock share does not necessarily reflect the stockholder’s equity in the company. A company’s stock certificates may show a par value of $5 but may have a current price on a stock exchange of over $100, depending on how well the company has performed financially. The real value of stock to stockholders is not the par value but the amount buyers are willing to pay for it (market value). In the same way, the value of a share of stock to the company is neither its par value nor its market value. The value of stock to the company relates to the financial health of the company, which is measured by the stock’s book value. The book value of a share of stock is calculated by dividing the corporation’s net worth (assets minus liabilities) by the total number of shares outstanding. Thus, if the corporation’s net worth is $75,000,000 and the number of shares of stock outstanding is 1,000,000, the book value per share is $75 ($75,000,000/1,000,000), regardless of the stock’s par value or market value. The lower the net worth of a company, the lower the book value of its stock. If the net worth is high, meaning the value of assets is much greater than the value of liabilities, the book value of the stock will also be high. Book value is an important tool when making judgments about the worth of a business. It is used as one measure to determine the value of a business that may be sold. It can be useful in a comparison of businesses by potential investors. Book value may also be used, in part, to estimate the amount of money that can be distributed to shareholders if a corporation fails.

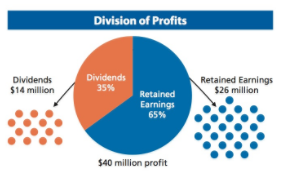

- Normally, a good policy for a firm is not to distribute all of its profits. A business can hold some of its profits in reserve for use in the business through retained earnings. If the corporation distributes all of its profits as dividends to stockholders, it may later need to borrow money for operations and unforeseen events. As illustrated in the Figure below, corporations usually distribute some of their profits as dividends and keep some in the business as retained earnings. In addition, if the corporation earns no profit during a particular period, it can use retained earnings to pay dividends for that period. If the corporation pays out all of its profits to stockholders, there are no retained earnings to fall back on during tough times. A business that retains some or all of its profits for use in the business is capable of reinvesting its earnings. A business retains earnings for some or all of the following reasons:

1. Replacement of buildings and equipment as the result of depreciation

2. Replacement of obsolete equipment

3. Purchase of new capital assets for expanding the business

4. Financial protection during periods of low sales and profits, such as recessions and tough competitive times.

- Even when the business is not making a profit, it should have financial plans to replace assets that decrease in value because of depreciation or obsolescence. For instance, a car rental company starts operations with all new cars. If the owners of the business do not develop an asset replacement fund through retained earnings and instead distribute all profits as dividends, funds will not be available to buy new cars when the original ones need to be replaced with new models. Retained earnings are not kept in the form of cash only. Retained earnings may be used for current assets such as inventories and accounts receivable, which can be quickly converted to cash if needed. These earnings should be invested in short or long-term securities that earn interest for the company. Because retained earnings are a part of owner’s equity, the earnings can be used for investment purposes and future expansion.

最后修改: 2018年08月14日 星期二 08:29