Reading: Lesson 3 - Financial statements of business organizations

Business entities may have many objectives and goals. For example, one of your objectives in owning a physical fitness center may be to improve your physical fitness. However, the two primary objectives of every business are profitability and solvency. Profitability is the ability to generate income. Solvency is the ability to pay debts as they become due. Unless a business can produce satisfactory income and pay its debts as they become due, the business cannot survive to realize its other objectives.

There are four basic financial statements. Together they present the profitability and strength of a company. The financial statement that reflects a company’s profitability is the income statement. The statement of retained earnings shows the change in retained earnings between the beginning and end of a period (e.g. a month or a year). The balance sheet reflects a company’s solvency and financial position. The statement of cash flows shows the cash inflows and outflows for a company over a period of time. The headings and elements of each statement are similar from company to company.

The income statement, sometimes called an earnings statement, reports the profitability of a business organization for a stated period of time. In accounting, we measure profitability for a period, such as a month or year, by comparing the revenues earned with the expenses incurred to produce these revenues. Revenues are the inflows of assets (such as cash) resulting from the sale of products or the rendering of services to customers. We measure revenues by the prices agreed on in the exchanges in which a business delivers goods or renders services. Expenses are the costs incurred to produce revenues. Expenses are measured by the assets surrendered or consumed in serving customers. If the revenues of a period exceed the expenses of the same period, net income results.

Thus,

Net income = Revenues – Expenses

Net income is often called the earnings of the company. When expenses exceed revenues, the business has a net loss, and it has operated unprofitably.

In Exhibit 2, Part A shows the income statement of Metro Courier, Inc., for July 2010. This

corporation performs courier delivery services of documents and packages in San Diego in the state of

California, USA.

Metro’s income statement for the month ended 2010 July 31, shows that the revenues (or delivery

fees) generated by serving customers for July totaled USD 5,700. Expenses for the month amounted to

USD 3,600. As a result of these business activities, Metro’s net income for July was USD 2,100. To

determine its net income, the company subtracts its expenses of USD 3,600 from its revenues of USD

5,700. Even though corporations are taxable entities, we ignore corporate income taxes at this point.

One purpose of the statement of retained earnings is to connect the income statement and the

balance sheet. The statement of retained earnings explains the changes in retained earnings

between two balance sheet dates. These changes usually consist of the addition of net income (or

deduction of net loss) and the deduction of dividends.

Dividends are the means by which a corporation rewards its stockholders (owners) for providing it

with investment funds. A dividend is a payment (usually of cash) to the owners of the business; it is a

distribution of income to owners rather than an expense of doing business. Corporations are not

required to pay dividends and, because dividends are not an expense, they do not appear on the income

statement.

The effect of a dividend is to reduce cash and retained earnings by the amount paid out. Then, the

company no longer retains a portion of the income earned but passes it on to the stockholders.

Receiving dividends is, of course, one of the primary reasons people invest in corporations.

The statement of retained earnings for Metro Courier, Inc., for July 2010 is relatively simple (see

Part B of Exhibit 2). Organized on June 1, Metro did not earn any revenues or incur any expenses

during June. So Metro’s beginning retained earnings balance on July 1 is zero. Metro then adds its USD 2,100 net income for July. Since Metro paid no dividends in July, the USD 2,100 would be the ending

balance of retained earnings. See below.

Exhibit 2:

Next, Metro carries this USD 2,100 ending balance in retained earnings to the balance sheet (Part

C). If there had been a net loss, it would have deducted the loss from the beginning balance on the

statement of retained earnings. For instance, if during the next month (August) there is a net loss of USD 500, the loss would be deducted from the beginning balance in retained earnings of USD 2,100.

The retained earnings balance at the end of August would be USD 1,600.

Dividends could also have affected the Retained Earnings balance. To give a more realistic

illustration, assume that (1) Metro Courier, Inc.’s net income for August was actually USD 1,500

(revenues of USD 5,600 less expenses of USD 4,100) and (2) the company declared and paid dividends

of USD 1,000. Then, Metro’s statement of retained earnings for August would be:

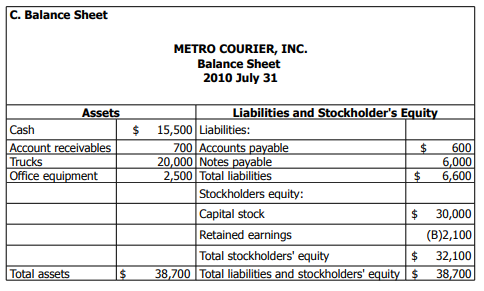

The balance sheet, sometimes called the statement of financial position, lists the company’s

assets, liabilities, and stockholders’ equity (including dollar amounts) as of a specific moment in time.

That specific moment is the close of business on the date of the balance sheet. Notice how the heading

of the balance sheet differs from the headings on the income statement and statement of retained

earnings. A balance sheet is like a photograph; it captures the financial position of a company at a

particular point in time. The other two statements are for a period of time. As you study about the

assets, liabilities, and stockholders’ equity contained in a balance sheet, you will understand why this

financial statement provides information about the solvency of the business.

Assets are things of value owned by the business. They are also called the resources of the

business. Examples include cash, machines, and buildings. Assets have value because a business can

use or exchange them to produce the services or products of the business. In Part C of Exhibit 2 the

assets of Metro Courier, Inc., amount to USD 38,700. Metro’s assets consist of cash, accounts

receivable (amounts due from customers for services previously rendered), trucks, and office

equipment.

Liabilities are the debts owed by a business. Typically, a business must pay its debts by certain

dates. A business incurs many of its liabilities by purchasing items on credit. Metro’s liabilities consist

of accounts payable (amounts owed to suppliers for previous purchases) and notes payable

(written promises to pay a specific sum of money) totaling USD 6,600.

Metro Courier, Inc., is a corporation. The owners’ interest in a corporation is referred to as

stockholders’ equity. Metro’s stockholders’ equity consists of (1) USD 30,000 paid for shares of

capital stock and (2) retained earnings of USD 2,100. Capital stock shows the amount of the owners’

investment in the corporation. Retained earnings generally consists of the accumulated net income

of the corporation minus dividends distributed to stockholders. We discuss these items later in the

text. At this point, simply note that the balance sheet heading includes the name of the organization

and the title and date of the statement. Notice also that the dollar amount of the total assets is equal to

the claims on (or interest in) those assets. The balance sheet shows these claims under the heading

“Liabilities and Stockholders’ Equity”.

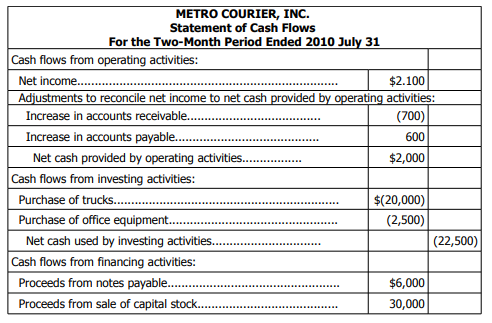

Management is interested in the cash inflows to the company and the cash outflows from the

company because these determine the company’s cash it has available to pay its bills when due. The

statement of cash flows shows the cash inflows and cash outflows from operating, investing, and

financing activities. Operating activities generally include the cash effects of transactions and other

events that enter into the determination of net income. Investing activities generally include business

transactions involving the acquisition or disposal of long-term assets such as land, buildings, and

equipment. Financing activities generally include the cash effects of transactions and other events

involving creditors and owners (stockholders).

Normally, a firm prepares a statement of cash flows for the same

time period as the income statement. The following statement, however, shows the cash inflows and

outflows for Metro Courier, Inc., since it was formed on 2010 June 1. Thus, this cash flow statement is

for two months.

At this point in the course, you need to understand what a statement of cash flows is rather than

how to prepare it. We do not ask you to prepare such a statement until you have studied Chapter 16.

The income statement, the statement of retained earnings, the balance sheet, and the statement of

cash flows of Metro Courier, Inc., show the results of management’s past decisions. They are the end

products of the accounting process, which we explain in the next section. These financial statements

give a picture of the solvency and profitability of the company. The accounting process details how this

picture was made. Management and other interested parties use these statements to make future

decisions. Management is the first to know the financial results; then, it publishes the financial

statements to inform other users. The most recent financial statements for most companies can be

found on their websites under “Investor Relations” or some similar heading.