Reading: Lesson 1 - Transactions affecting only the balance sheet

1a. Owners invested cash

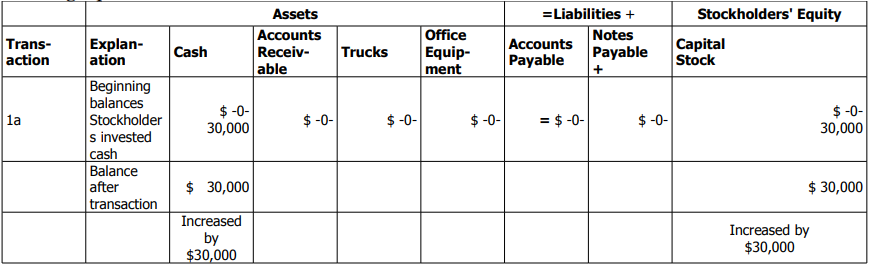

When Metro Courier, Inc., was organized as a corporation on 2010 June 1, the company issued

shares of capital stock for USD 30,000 cash to Ron Chaney, his wife, and their son. This transaction

increased assets (cash) of Metro by USD 30,000 and increased equities (the capital stock element of

stockholders’ equity) by USD 30,000. Consequently, the transaction yields the following basic

accounting equation:

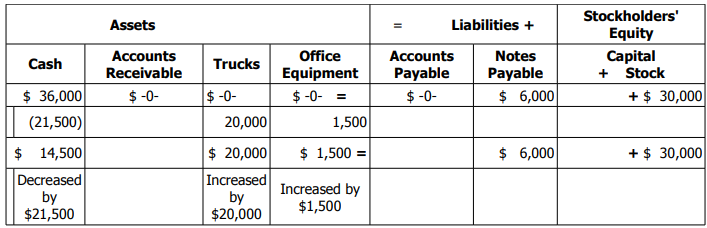

2a. Borrowed money The company borrowed USD 6,000 from Chaney’s father. Chaney signed the note for the company.

The note bore no interest and the company promised to repay (recorded as a note payable) the amount

borrowed within one year. After including the effects of this transaction, the basic accounting equation

is: 3a. Purchased trucks and office equipment for cash Metro paid USD 20,000 cash for two used delivery trucks and USD 1,500 for office equipment.

Trucks and office equipment are assets because the company uses them to earn revenues in the future.

Note that this transaction does not change the total amount of assets in the basic equation but only

changes the composition of the assets. This transaction decreased cash and increased trucks and office equipment (assets) by the total amount of the cash decrease. Metro received two assets and gave up

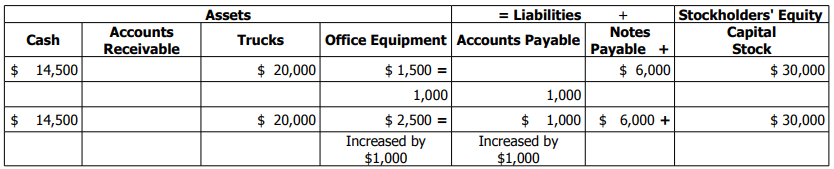

one asset of equal value. Total assets are still USD 36,000. The accounting equation now is: 4a. Purchased office equipment on account (for credit) Metro purchased an additional USD 1,000 of office equipment on account, agreeing to pay within

10 days after receiving the bill. (To purchase an item on account means to buy it on credit.) This

transaction increased assets (office equipment) and liabilities (accounts payable) by USD 1,000. As

stated earlier, accounts payable are amounts owed to suppliers for items purchased on credit. Now you

can see the USD 1,000 increase in the assets and liabilities as follows:

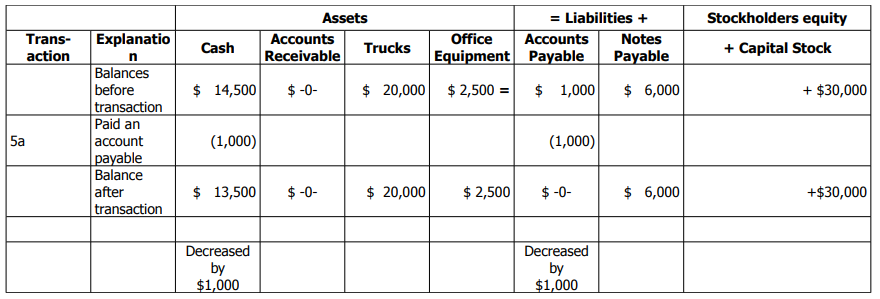

5a. Paid an account payable

Eight days after receiving the bill, Metro paid USD 1,000 for the office equipment purchased on

account (transaction 4a). This transaction reduced cash by USD 1,000 and reduced accounts payable

by USD 1,000. Thus, the assets and liabilities both are reduced by USD 1,000, and the equation again

balances as follows:

Part A, is a summary of transactions prepared in accounting equation form for June. A summary of transactions is a teaching tool used to show the effects of transactions on the accounting equation. Note that the stockholders’ equity has remained at USD 30,000. This amount changes as the business begins to earn revenues or incur expenses. You can see how the totals at the bottom of Part A of Exhibit 3 tie into the balance sheet shown in Part B. The date on the balance sheet is 2010 June 30. These totals become the beginning balances for July 2010.

Thus far, all transactions have consisted of exchanges or acquisitions of assets either by borrowing

or by owner investment. We used this procedure to help you focus on the accounting equation as it

relates to the balance sheet. However, people do not form a business only to hold existing assets. They

form businesses so their assets can generate greater amounts of assets. Thus, a business increases its

assets by providing goods or services to customers. The results of these activities appear in the income

statement. The section that follows shows more of Metro’s transactions as it began earning revenues

and incurring expenses.