Reading: Lesson 2 - Transactions affecting the income statement and/or balance sheet

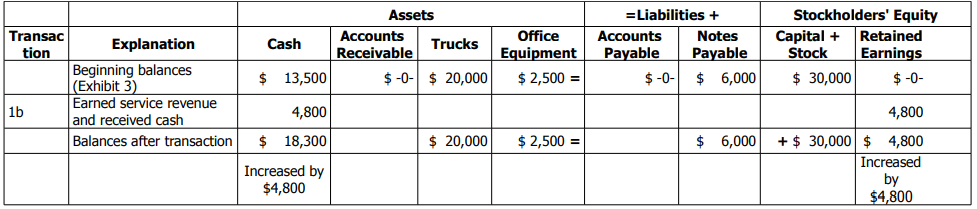

1b. Earned service revenue and received cash

As its first transaction in July, Metro performed delivery services for customers and received USD

4,800 cash. This transaction increased an asset (cash) by USD 4,800. Stockholders’ equity (retained

earnings) also increased by USD 4,800, and the accounting equation was in balance.

The USD 4,800 is a revenue earned by the business and, as such, increases stockholders’ equity (in

the form of retained earnings) because stockholders prosper when the business earns profits. Likewise,

if the corporation sustains a loss, the loss would reduce retained earnings. Revenues increase the amount of retained earnings while expenses and dividends decrease them.

(In this first chapter, we show all of these items as immediately affecting retained earnings. In later

chapters, the revenues, expenses, and dividends are accounted for separately from retained earnings

during the accounting period and are transferred to retained earnings only at the end of the accounting

period as part of the closing process described in Chapter 4.) The effects of this USD 4,800 transaction

on the financial position of Metro are:

Metro would record the increase in stockholders’ equity brought about by the revenue transaction

as a separate account, retained earnings. This does not increase capital stock because the Capital Stock

account increases only when the company issues shares of stock. The expectation is that revenue

transactions will exceed expenses and yield net income. If net income is not distributed to

stockholders, it is in fact retained. Later chapters show that because of complexities in handling large

numbers of transactions, revenues and expenses affect retained earnings only at the end of an

accounting period. The preceding procedure is a shortcut used to explain why the accounting equation

remains in balance.

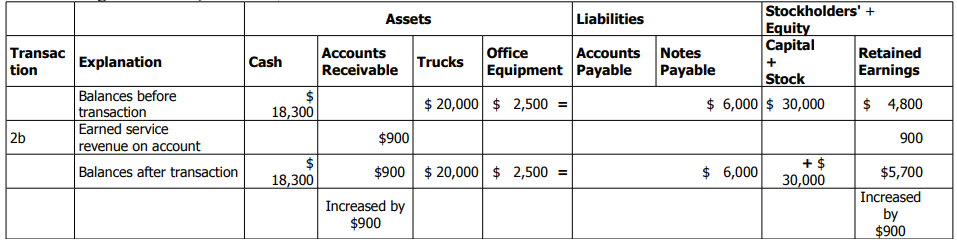

2b. Service revenue earned on account (for credit)

Metro performed courier delivery services for a customer who agreed to pay USD 900 at a later

date. The company granted credit rather than requiring the customer to pay cash immediately. This is

called earning revenue on account. The transaction consists of exchanging services for the customer’s

promise to pay later. This transaction is similar to the preceding transaction in that stockholders’

equity (retained earnings) increases because the company has earned revenues. However, the

transaction differs because the company has not received cash. Instead, the company has received

another asset, an account receivable. As noted earlier, an account receivable is the amount due from a

customer for goods or services already provided. The company has a legal right to collect from the

customer in the future. Accounting recognizes such claims as assets. The accounting equation,

including this USD 900 item, is as follows:

3b. Collected cash on accounts receivable

Metro collected USD 200 on account from the customer in transaction 2b. The customer will pay

the remaining USD 700 later. This transaction affects only the balance sheet and consists of giving up a

claim on a customer in exchange for cash. The transaction increases cash by USD 200 and decreases

accounts receivable by USD 200. Note that this transaction consists solely of a change in the

composition of the assets. When the company performed the services, it recorded the revenue.

Therefore, the company does not record the revenue again when collecting the cash.

4b. Paid salaries

Metro paid employees USD 2,600 in salaries. This transaction is an exchange of cash for employee

services. Typically, companies pay employees for their services after they perform their work. Salaries

(or wages) are costs companies incur to produce revenues, and companies consider them an expense.

Thus, the accountant treats the transaction as a decrease in an asset (cash) and a decrease in

stockholders’ equity (retained earnings) because the company has incurred an expense. Expense

transactions reduce net income. Since net income becomes a part of the retained earnings balance,

expense transactions also reduce the retained earnings.

5b. Paid rent

In July, Metro paid USD 400 cash for office space rental. This transaction causes a decrease in cash

of USD 400 and a decrease in retained earnings of USD 400 because of the incurrence of rent expense.

Transaction 5b has the following effects on the amounts in the accounting equation:

6b. Received bill for gas and oil used

At the end of the month, Metro received a USD 600 bill for gas and oil consumed during the month.

This transaction involves an increase in accounts payable (a liability) because Metro has not yet paid

the bill and a decrease in retained earnings because Metro has incurred an expense. Metro’s accounting

equation now reads:

Summary of balance sheet and income statement

transactions

Part A of Exhibit 4 summarizes the effects of all the preceding transactions on the assets, liabilities, and stockholders’ equity of Metro Courier, Inc., in July. The beginning balances are the ending balances in Part A of Exhibit 3. The summary shows subtotals after each transaction; these subtotals are optional and may be omitted. Note how the accounting equation remains in balance after each transaction and at the end of the month.

The ending balances in each of the columns in Part A of Exhibit 4 are the dollar amounts in Part B and those reported earlier in the balance sheet in Part C of Exhibit 2. The itemized data in the Retained Earnings column are the revenue and expense items in Part C of Exhibit 4 and those reported earlier in the income statement in Part A of Exhibit 2. The beginning balance in the Retained Earnings column (USD 0) plus net income for the month (USD 2,100) is equal to the ending balance in retained earnings (USD 2,100) shown earlier in Part B of Exhibit 2. Remember that the financial statements are not an end in themselves, but are prepared to assist users of those statements to make informed decisions. Throughout the text we show how people use accounting information in decision making.