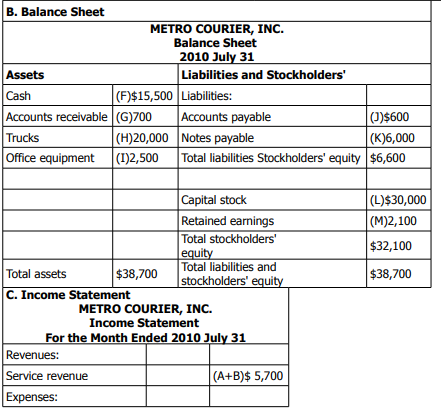

Reading: Lesson 3 - Dividends paid to owners and the equity ratio

Stockholders’ equity is (1) increased by capital contributed by stockholders and by revenues earned

through operations and (2) decreased by expenses incurred in producing revenues. The payment of

cash or other assets to stockholders in the form of dividends also reduces stockholders’ equity. Thus, if

the owners receive a cash dividend, the effect would be to reduce the retained earnings part of

stockholders’ equity; the amount of dividends is not an expense but a distribution of income.

Analyzing and using the financial results—the equity ratio

The two basic sources of equity in a company are stockholders and creditors; their combined

interests are called total equities. To find the equity ratio, divide stockholders’ equity by total equities

or total assets, since total equities equals total assets. In formula format:

![]()

The higher the proportion of equities (or assets) supplied by the owners, the more solvent the

company. However, a high portion of debt may indicate higher profitability because quite often the

interest rate on debt is lower than the rate of earnings realized from using the proceeds of the debt.

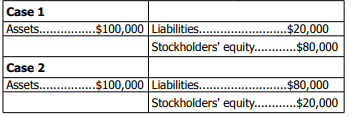

An example illustrates this concept: Suppose that a company with USD 100,000 in assets could

have raised the funds to acquire those assets in these two ways:

When a company suffers operating losses, its assets decrease. In Case 1, the assets would have to shrink by 80 per cent before the liabilities would equal the assets. In Case 2, the assets would have to shrink only 20 per cent before the liabilities would equal the assets. When the liabilities exceed the assets, the company is said to be insolvent. Therefore, creditors are safer in Case 1 and will more readily lend money to the company.

However, if funds borrowed at 10 per cent are used to produce earnings at a 20 per cent rate, Case 2

is preferable in terms of profitability. Therefore, owners are better off in Case 2 if the borrowed funds

can earn more than they cost.

Next, we examine the recent equity ratios of some actual companies:

As you can see from the preceding data, the equity ratios of actual companies vary widely.

Companies such as Johnson & Johnson and 3M Corporation employ a higher proportion of

stockholders’ equity (a lower proportion of debt) than GE in an effort to have stronger balance sheets

(more solvency). GE employs a greater proportion of debt, possibly in an attempt to increase

profitability. Every company must strike a balance between solvency and profitability to ensure longrun

survival. The correct balance between proportions of stockholder and creditor equities depends on

the industry, general business conditions, and management philosophy.

Chapter 1 has introduced two important components of the accounting process—the accounting

equation and the business transaction. In Chapter 3, you learn about debits and credits and how

accountants use them in recording transactions. Understanding how data are accumulated, classified,

and reported in financial statements helps you understand how to use financial statement data in

making decisions.