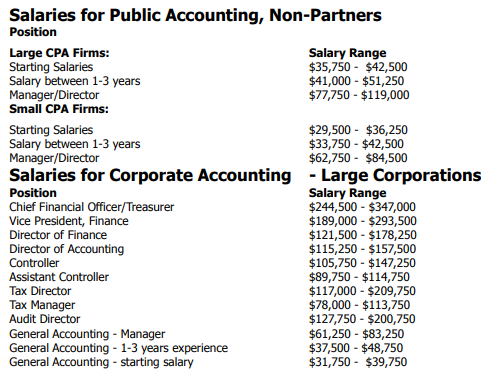

Reading: Lesson 1 - Salary potential of accountants

Selecting a major represents much more than the choice of courses a student takes in college. To a

significant degree, the student's major, along with academic performance, will determine the career

paths available upon graduation. Few professionals would recommend a specific career choice based

solely on salaries. However, as students select their major and map out their career path, it is

important that they make informed decisions with respect to the potential financial rewards of the

various options. Outlined below is information on selected salaries for many accounting-related

careers. These salaries, current as of 2009, should be viewed only as guidelines. Salaries at all levels

can vary significantly between locations. Also, one should add 10 to 15 per cent to the listed salary for

professional certifications (such as the CPA) or for a graduate degree (Masters of Accounting or MBA).

Students interested in a career in accounting and finance can find detailed information for these

and many other accounting related careers at Robert Half (www.roberthalf.com). Also, accounting

professors are generally familiar with starting salaries and job opportunities for accounting graduates,

so you may want to address more specific questions about potential careers and salaries with them.

In Chapter 1, we illustrated the income statement, statement of retained earnings, balance sheet,

and statement of cash flows. These statements are the end products of the financial accounting process,

which is based on the accounting equation. The financial accounting process quantifies past

management decisions. The results of these decisions are communicated to users—management,

creditors, and investors—and serve as a basis for making future decisions.

The raw data of accounting are the business transactions. We recorded the transactions in Unit 1

as increases or decreases in the assets, liabilities, and stockholders' equity items of the accounting

equation. This procedure showed you how various transactions affected the accounting equation.

When working through these sample transactions, you probably suspected that listing all transactions

as increases or decreases in the transactions summary columns would be too cumbersome in practice.

Most businesses, even small ones, enter into many transactions every day. Unit 3 teaches you how

to actually record business transactions in the accounting process.

To explain the dual procedure of recording business transactions with debits and credits, we

introduce you to some new tools: the T-account, the journal, and the ledger. Using these tools, you can

follow a company through its various business transactions. Like accountants, you can use a trial

balance to check the equality of your recorded debits and credits. This is the double-entry accounting system that the Franciscan monk, Luca Pacioli, described centuries ago. Understanding this system

enables you to better understand the content of financial statements so you can use the information

provided to make informed business decisions.