Reading: Lesson 3 - Recording changes in assets, liabilities, and stockholders' equity

Assets = Liabilities + Stockholders' Equity

Recording transactions into the T-accounts is easier when you focus on the equal sign in the

accounting equation. Assets, which are on the left of the equal sign, increase on the left side of the T -accounts.

Liabilities and stockholders' equity, to the right of the equal sign, increase on the right side of

the T-accounts. You already know that the left side of the T-account is the debit side and the right side is the credit side. So you should be able to fill in the rest of the rules of increases and decreases by

deduction, such as:

To summarize:

- Assets increase by debits (left side) to the T-account and decrease by credits (right side) to the Taccount.

- Liabilities and stockholders' equity decrease by debits (left side) to the T-account and increase

by credits (right side) to the T-account.

Applying these two rules keeps the accounting equation in balance. Now we apply the debit and

credit rules for assets, liabilities, and stockholders' equity to business transactions.

Assume a corporation issues shares of its capital stock for USD 10,000 in transaction 1. (Note the

figure in parentheses is the number of the transaction and ties the two sides of the transaction

together.) The company records the receipt of USD 10,000 as follows:

![]()

This transaction increases the asset, cash, which is recorded on the left side of the Cash account.

Then, the transaction increases stockholders' equity, which is recorded on the right side of the Capital

Stock account.

Assume the company borrowed USD 5,000 from a bank on a note (transaction 2). A note is an

unconditional written promise to pay to another party (the bank) the amount owed either when

demanded or at a specified date, usually with interest at a specified rate. The firm records this

transaction as follows:

Observe that liabilities, Notes Payable, increase with an entry on the right (credit) side of the

account.

Recording changes in revenues and expenses In Unit 2, we recorded the revenues and expenses directly in the Retained Earnings account. However, this is not done in practice because of the volume of revenue and expense transactions. Instead, businesses treat the expense accounts as if they were subclassifications of the debit side of the Retained Earnings account, and the revenue accounts as if they were subclassifications of the credit side. Since firms need the amounts of revenues and expenses to prepare the income statement, they keep a separate account for each type of revenue and expense. The recording rules for revenues and expenses are:

- Record increases in revenues on the right (credit) side of the T-account and decreases on the

left (debit) side. The reasoning behind this rule is that revenues increase retained earnings, and

increases in retained earnings are recorded on the right side.

- Record increases in expenses on the left (debit) side of the T-account and decreases on the

right (credit) side. The reasoning behind this rule is that expenses decrease retained earnings,

and decreases in retained earnings are recorded on the left side.

To illustrate these rules, assume the same company received USD 1,000 cash from a customer for

services rendered (transaction 3). The Cash account, an asset, increases on the left (debit) side of the Taccount;

and the Service Revenue account, an increase in retained earnings, increases on the right

(credit) side.

Now assume this company paid USD 600 in salaries to employees (transaction 4). The Cash

account, an asset, decreases on the right (credit) side of the T-account; and the Salaries Expense

account, a decrease in retained earnings, increases on the left (debit) side.

Recording changes in dividends Since dividends decrease retained earnings, increases appear on the left side of the

Dividends account and decreases on the right side. Thus, the firm records payment of a USD 2,000 cash dividend (transaction

5) as follows:

(2) Certain deductions are normally taken out of employees' pay for social security taxes, federal and

state withholding, and so on. Those deductions are ignored here.

At the end of the accounting period, the accountant transfers any balances in the expense, revenue,

and Dividends accounts to the Retained Earnings account. This transfer occurs only after the

information in the expense and revenue accounts has been used to prepare the income statement.

To determine the balance of any T-account, total the debits to the account, total the credits to the

account, and subtract the smaller sum from the larger. If the sum of the debits exceeds the sum of the

credits, the account has a debit balance. For example, the following Cash account uses information

from the preceding transactions. The account has a debit balance of USD 13,400, computed as total

debits of USD 16,000 less total credits of USD 2,600.

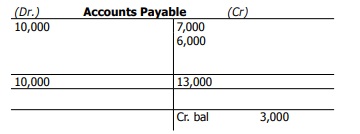

If, on the other hand, the sum of the credits exceeds the sum of the debits, the account has a credit

balance. For instance, assume that a company has an Accounts Payable account with a total of USD

10,000 in debits and USD 13,000 in credits. The account has a credit balance of USD 3,000, as shown

in the following T-account:

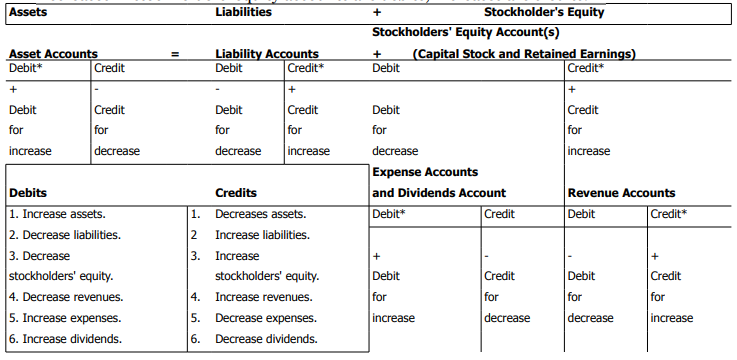

Normal balances Since debits increase asset, expense, and dividend accounts, they normally have debit (or left-side) balances. Conversely, because credits increase liability, capital stock, retained earnings, and revenue accounts, they normally have credit (or right-side) balances. The following chart shows the normal balances of the seven accounts we have used:

At this point, you should memorize the six rules of debit and credit. Later, as you proceed in your

study of accounting, the rules will become automatic. Then, you will no longer ask yourself, "Is this

increase a debit or credit?"

Asset accounts increase on the debit side, while liability and stockholders' equity accounts increase

on the credit side. When the account balances are totaled, they conform to the following independent

equations:

Assets = Liabilities + Stockholders' Equity

Debits = Credits

The arrangement of these two formulas gives the first three rules of debit and credit:

- Increases in asset accounts are debits; decreases are credits.

- Decreases in liability accounts are debits; increases are credits.

- Decreases in stockholders' equity accounts are debits; increases are credits.

Exhibit 6: Rules of debit and credit

The debit and credit rules for expense and Dividends accounts and for revenue accounts follow

logically if you remember that expenses and dividends are decreases in stockholders' equity and

revenues are increases in stockholders' equity. Since stockholders' equity accounts decrease on the debit side, expense and Dividend accounts increase on the debit side. Since stockholders' equity

accounts increase on the credit side, revenue accounts increase on the credit side. The last three debit

and credit rules are:

- Decreases in revenue accounts are debits; increases are credits.

- Increases in expense accounts are debits; decreases are credits.

- Increases in Dividends accounts are debits; decreases are credits.

In Exhibit 6, we depict these six rules of debit and credit. Note first the treatment of expense and Dividends accounts as if they were subclassifications of the debit side of the Retained Earnings account. Second, note the treatment of the revenue accounts as if they were subclassifications of the credit side of the Retained Earnings account.