Reading: Lesson 2 - Cash versus accrual basis accounting

Because the cash basis of accounting does not match expenses incurred and revenues earned, it is

generally considered theoretically unacceptable. The cash basis is acceptable in practice only under

those circumstances when it approximates the results that a company could obtain under the accrual

basis of accounting. Companies using the cash basis do not have to prepare any adjusting entries

unless they discover they have made a mistake in preparing an entry during the accounting period.

Under certain circumstances, companies may use the cash basis for income tax purposes.

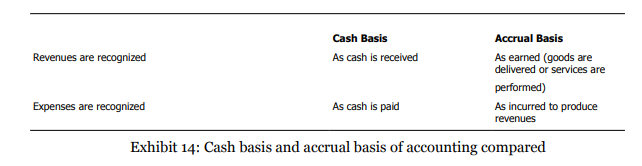

Throughout the text we use the accrual basis of accounting, which matches expenses incurred and

revenues earned, because most companies use the accrual basis. The accrual basis of accounting

recognizes revenues when sales are made or services are performed, regardless of when cash is

received. Expenses are recognized as incurred, whether or not cash has been paid out. For instance,

assume a company performs services for a customer on account. Although the company has received

no cash, the revenue is recorded at the time the company performs the service. Later, when the

company receives the cash, no revenue is recorded because the company has already recorded the

revenue. Under the accrual basis, adjusting entries are needed to bring the accounts up to date for

unrecorded economic activity that has taken place. In Exhibit 14, shown below, we show when

revenues and expenses are recognized under the cash basis and under the accrual basis.