Reading: Lesson 2 - Sales revenues

The sale of goods occurs between two parties. The seller of the goods transfers them to the buyer in

exchange for cash or a promise to pay at a later date. This exchange is a relatively simple business transaction. Sellers make sales to create revenues; this inflow of assets in the form of cash or accounts

receivable results from selling goods to customers.

In Exhibit 32, we show a condensed income statement to emphasize its major divisions. Next, we describe the more complete income statement actually prepared by accountants. The merchandising company that we use to illustrate the income statement is Hanlon Retail Food Store. This section explains how to record sales revenues, including the effect of trade discounts. Then, we explain how to record two deductions from sales revenues—sales discounts and sales returns and allowances (Exhibit 33). The amount that remains is net sales.

The formula for determining net sales is:

Net sales = Gross sales - (Sales discounts + Sales returns and allowances)

Exhibit 33: Partial income statement of merchandising company

Exhibit 34: Invoice

In a sales transaction, the seller transfers the legal ownership (title) of the goods to the buyer.

Usually, the physical delivery of the goods occurs at the same time as the sale of the goods. A business

document called an invoice (a sales invoice for the seller and a purchase invoice for the buyer) becomes

the basis for recording the sale.

An invoice is a document prepared by the seller of merchandise and sent to the buyer. The invoice

contains the details of a sale, such as the number of units sold, unit price, total price billed, terms of

sale, and manner of shipment. A retail company prepares the invoice at the point of sale. A wholesale

company, which supplies goods to retailers, prepares the invoice after the shipping department notifies

the accounting department that it has shipped the goods to the retailer. Exhibit 34 is an example of an

invoice prepared by a wholesale company for goods sold to a retail company.

Using the invoice as the source document, a wholesale company records the revenue from the sale

at the time of the sale for the following reasons:

- The seller has passed legal title of the goods to the buyer, and the goods are now the responsibility and property of the buyer.

- The seller has established the selling price of the goods.

- The seller has completed its obligation.

- The seller has exchanged the goods for another asset, such as cash or accounts receivable.

- The seller can determine the costs incurred in selling the goods.

Each time a company makes a sale, the company earns revenue. This revenue increases a revenue

account called Sales. Recall from Unit 3 that credits increase revenues. Therefore, the firm credits

the Sales account for the amount of the sale.

Usually sales are for cash or on account. When a sale is for cash, the company credits the Sales

account and debits Cash. For example, it records a USD 20,000 sale for cash as follows:

When a sale is on account, it credits the Sales account and debits Accounts Receivable. The

following entry records a USD 20,000 sale on account:

Usually, a seller quotes the gross selling price, also called the invoice price, of goods to the buyer.

However, sometimes a seller quotes a list price of goods along with available trade discounts. In this

latter situation, the buyer must calculate the gross selling price. The list price less all trade discounts is

the gross selling price. Merchandising companies that sell goods use the gross selling price as the

credit to sales.

A trade discount is a percentage deduction, or discount, from the specified list price or catalog

price of merchandise. Companies use trade discounts to:

- Reduce the cost of catalog publication. A seller can use a catalog for a longer time by printing list prices in the catalog and giving separate discount sheets to salespersons whenever prices change.

- Grant quantity discounts.

- Allow quotation of different prices to various customers, such as retailers and wholesalers.

The seller's invoice may show trade discounts. However, sellers do not record trade discounts in

their accounting records because the discounts are used only to calculate the gross selling price. Nor do

trade discounts appear on the books of the purchaser. To illustrate, assume an invoice contains the

following data:

The seller records a sale of USD 3,360. The purchaser records a purchase of USD 3,360. Thus,

neither the seller nor the purchaser enters list prices and trade discounts on their books.

Sometimes the list price of a product is subject to several trade discounts; this series of discounts is

a chain discount. Chain discounts exist, for example, when a wholesaler receives two trade discounts

for services performed, such as packaging and distributing. When more than one discount is given, the

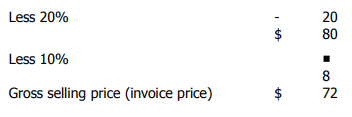

buyer applies each discount to the declining balance successively. If a product has a list price of USD

100 and is subject to trade discounts of 20 per cent and 10 per cent, the gross selling price (invoice

price) would be USD 100 - 0.2(USD 100) = USD 80; USD 80 - 0.1(USD 80) = USD 72, computed as

follows:

![]()

You could obtain the same results by multiplying the list price by the complements of the trade

discounts allowed. The complement of 20 per cent is 80 per cent because 20 per cent + 80 per cent =

100 per cent. The complement of 10 per cent is 90 per cent because 10 per cent + 90 per cent = 100 per

cent. Thus, the gross selling price is USD 100 X 0.8 X 0.9 = USD 72.

Two common deductions from gross sales are (1) sales discounts and (2) sales returns and

allowances. Sellers record these deductions in contra revenue accounts to the Sales account. Contra

accounts have normal balances that are opposite to the balance of the account they reduce. For

example, since the Sales account normally has a credit balance, the Sales Discounts account and Sales

Returns and Allowances account have debit balances. We explain the methods of recording these

contra revenue accounts next.

Sales discounts Whenever a company sells goods on account, it clearly specifies terms of payment

on the invoice. For example, the invoice in Exhibit 34 states the terms of payment as "net 30".

Net 30 is sometimes written as "n/30". Either way, this term means that the buyer may not take a

discount and must pay the entire amount of the invoice (USD 20,000) on or before 30 days after 2010

December 19 (invoice date)—or 2011 January 18. In Exhibit 34, if the terms had read "n/10/EOM"

(EOM means end of month), the buyer could not take a discount, and the invoice would be due on the

10th day of the month following the month of sale—or 2011 January 10. Credit terms vary from

industry to industry.

In some industries, credit terms include a cash discount of 1 per cent to 3 per cent to induce early

payment of an amount due. A cash discount is a deduction from the invoice price that can be taken

only if the invoice is paid within a specified time. A cash discount differs from a trade discount in that a

cash discount is a deduction from the gross selling price for the prompt payment of an invoice. In

contrast, a trade discount is a deduction from the list price to determine the gross selling price (or

invoice price). Sellers call a cash discount a sales discount and buyers call it a purchase discount.

Companies often state cash discount terms as follows:

- 2/10, n/30—means a buyer who pays within 10 days following the invoice date may deduct a

discount of 2 per cent of the invoice price. If payment is not made within the discount period, the

entire invoice price is due 30 days from the invoice date.

- 2/EOM, n/60—means a buyer who pays by the end of the month of purchase may deduct a 2

per cent discount from the invoice price. If payment is not made within the discount period, the

entire invoice price is due 60 days from the invoice date.

- 2/10/EOM, n/60—means a buyer who pays by the 10th of the month following the month of

purchase may deduct a 2 per cent discount from the invoice price. If payment is not made within

the discount period, the entire invoice price is due 60 days from the invoice date.

Sellers cannot record the sales discount before they receive the payment since they do not know

when the buyer will pay the invoice. A cash discount taken by the buyer reduces the cash that the seller

actually collects from the sale of the goods, so the seller must indicate this fact in its accounting

records. The following entries show how to record a sale and a subsequent sales discount.

Assume that on July 12, a business sold merchandise for USD 2,000 on account; terms are 2/10,

n/30. On July 21 (nine days after invoice date), the business received a USD 1,960 check in payment of

the account. The required journal entries for the seller are:

The Sales Discounts account is a contra revenue account to the Sales account. In the income

statement, the seller deducts this contra revenue account from gross sales. Sellers use the Sales

Discounts account (rather than directly reducing the Sales account) so management can examine the

sales discounts figure to evaluate the company's sales discount policy. Note that the Sales Discounts

account is not an expense incurred in generating revenue. Rather, the purpose of the account is to

reduce recorded revenue to the amount actually realized from the sale.

Sales returns and allowances Merchandising companies usually allow customers to return

goods that are defective or unsatisfactory for a variety of reasons, such as wrong color, wrong size,

wrong style, wrong amounts, or inferior quality. In fact, when their policy is satisfaction guaranteed,

some companies allow customers to return goods simply because they do not like the merchandise. A

sales return is merchandise returned by a buyer. Sellers and buyers regard a sales return as a

cancellation of a sale. Alternatively, some customers keep unsatisfactory goods, and the seller gives them an allowance off the original price. A sales allowance is a deduction from the original invoiced

sales price granted when the customer keeps the merchandise but is dissatisfied for any of a number of

reasons, including inferior quality, damage, or deterioration in transit. When a seller agrees to the sales

return or sales allowance, the seller sends the buyer a credit memorandum indicating a reduction

(crediting) of the buyer's account receivable. A credit memorandum is a document that provides space

for the name and address of the concerned parties, followed by a space for the reason for the credit and

the amount to be credited. A credit memorandum becomes the basis for recording a sales return or a

sales allowance.

In theory, sellers could record both sales returns and sales allowances as debits to the Sales account

because they cancel part of the recorded selling price.

However, because the amount of sales returns and sales allowances is useful information to

management, it should be shown separately. The amount of returns and allowances in relation to

goods sold can indicate the quality of the goods (high-return percentage, equals low quality) or of

pressure applied by salespersons (high-return percentage, equals high-pressure sales). Thus, sellers

record sales returns and sales allowances in a separate Sales Returns and Allowances account. The

Sales Returns and Allowances account is a contra revenue account (to Sales) that records the

selling price of merchandise returned by buyers or reductions in selling prices granted. (Some

companies use separate accounts for sales returns and for sales allowances, but this text does not.)

Following are two examples illustrating the recording of sales returns in the Sales Returns and

Allowances account:

- Assume that a customer returns USD 300 of goods sold on account. If payment has not yet been

received, the required entry is:

- Assume that the customer has already paid the account and the seller gives the customer a cash

refund. Now, the credit is to Cash rather than to Accounts Receivable. If the customer has taken a

2 per cent discount when paying the account, the company would return to the customer the sales

price less the sales discount amount. For example, if a customer returns goods that sold for USD

300, on which a 2 per cent discount was taken, the following entry would be made:

The debit to the Sales Returns and Allowances account is for the full selling price of the purchase.

The credit of USD 6 reduces the balance of the Sales Discounts account.

Next, we illustrate the recording of a sales allowance in the Sales Returns and Allowances account.

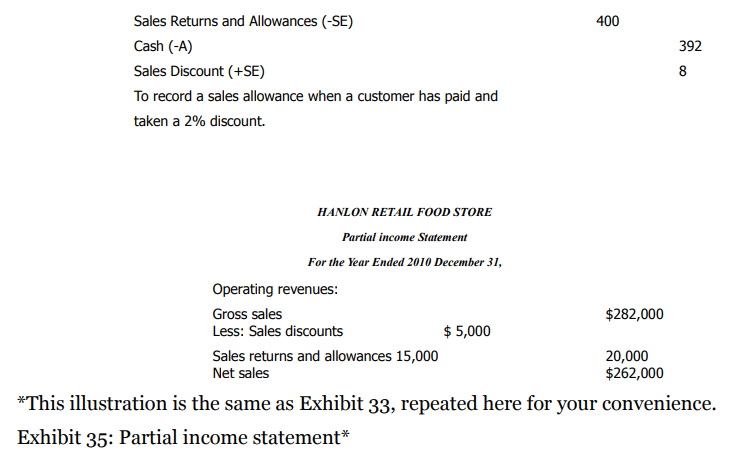

Assume that a company grants a USD 400 allowance to a customer for damage resulting from

improperly packed merchandise. If the customer has not yet paid the account, the required entry

would be:

If the customer has already paid the account, the credit is to Cash instead of Accounts Receivable. If

the customer took a 2 per cent discount when paying the account, the company would refund only the

net amount (USD 392). Sales Discounts would be credited for USD 8. The entry would be:

Exhibit 35 shows how a company could report sales, sales discounts, and sales returns and allowances in the income statement. More often, the income statement in a company's annual report begins with "Net sales" because sales details are not important to external financial statement users.