Reading: Lesson 3 - Cost of goods sold

The second main division of an income statement for a merchandising business is cost of goods

sold. Cost of goods sold is the cost to the seller of the goods sold to customers. For a merchandising

company, the cost of goods sold can be relatively large. All merchandising companies have a quantity of

goods on hand called merchandise inventory to sell to customers. Merchandise inventory (or

inventory) is the quantity of goods available for sale at any given time. Cost of goods sold is determined

by computing the cost of (1) the beginning inventory, (2) the net cost of goods purchased, and (3) the

ending inventory.

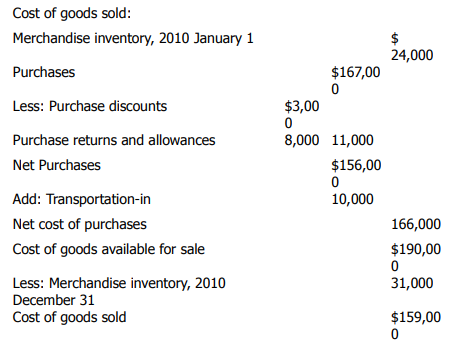

Look at the cost of goods sold section of Hanlon Retail Food Store's income statement in Exhibit 36.

The merchandise inventory on 2010 January 1, was USD 24,000. The net cost of purchases for the year was USD 166,000. Thus, Hanlon had USD 190,000 of merchandise available for sale during 2010. On

2010 December 31, the merchandise inventory was USD 31,000, meaning that this amount was left

unsold. Subtracting the unsold inventory (the ending inventory), USD 31,000, from the amount

Hanlon had available for sale during the year, USD 190,000, gives the cost of goods sold for the year of

USD 159,000. Understanding this relationship shown on Hanlon Retail Food Store's partial income

statement gives you the necessary background to determine the cost of goods sold as presented in this

section.

Exhibit 36: Determination of cost of goods sold for Hanlon Retail Food Store

To determine the cost of goods sold, accountants must have accurate merchandise inventory

figures. Accountants use two basic methods for determining the amount of merchandise inventory—

perpetual inventory procedure and periodic inventory procedure. We mention perpetual inventory

procedure only briefly here. In the next chapter, we emphasize perpetual inventory procedure and

further compare it with periodic inventory procedure.

When discussing inventory, we need to clarify whether we are referring to the physical goods on

hand or the Merchandise Inventory account, which is the financial representation of the physical goods

on hand. The difference between perpetual and periodic inventory procedures is the frequency with

which the Merchandise Inventory account is updated to reflect what is physically on hand. Under

perpetual inventory procedure, the Merchandise Inventory account is continuously updated to

reflect items on hand. For example, your supermarket uses a scanner to ring up your purchases. When

your box of Rice Krispies crosses the scanner, the Merchandise Inventory account shows that one less

box of Rice Krispies is on hand.

Under periodic inventory procedure, the Merchandise Inventory account is updated

periodically after a physical count has been made. Usually, the physical count takes place immediately

before the preparation of financial statements.

Perpetual inventory procedure Companies use perpetual inventory procedure in a variety of

business settings. Historically, companies that sold merchandise with a high individual unit value, such

as automobiles, furniture, and appliances, used perpetual inventory procedure. Today, computerized

cash registers, scanners, and accounting software programs automatically keep track of inflows and

outflows of each inventory item. Computerization makes it economical for many retail stores to use

perpetual inventory procedure even for goods of low unit value, such as groceries.

Under perpetual inventory procedure, the Merchandise Inventory account provides close control by

showing the cost of the goods that are supposed to be on hand at any particular time. Companies debit

the Merchandise Inventory account for each purchase and credit it for each sale so that the current

balance is shown in the account at all times. Usually, firms also maintain detailed unit records showing

the quantities of each type of goods that should be on hand. Company personnel also take a physical

inventory by actually counting the units of inventory on hand. Then they compare this physical count

with the records showing the units that should be on hand. Chapter 7 describes perpetual inventory

procedure in more detail.

Periodic inventory procedure Merchandising companies selling low unit value merchandise

(such as nuts and bolts, nails, Christmas cards, or pencils) that have not computerized their inventory

systems often find that the extra costs of record-keeping under perpetual inventory procedure more

than outweigh the benefits. These merchandising companies often use periodic inventory procedure.

Under periodic inventory procedure, companies do not use the Merchandise Inventory account to

record each purchase and sale of merchandise. Instead, a company corrects the balance in the

Merchandise Inventory account as the result of a physical inventory count at the end of the accounting

period. Also, the company usually does not maintain other records showing the exact number of units

that should be on hand. Although periodic inventory procedure reduces record-keeping, it also reduces

control over inventory items.

Companies using periodic inventory procedure make no entries to the Merchandise Inventory

account nor do they maintain unit records during the accounting period. Thus, these companies have

no up-to-date balance against which to compare the physical inventory count at the end of the period.

Also, these companies make no attempt to determine the cost of goods sold at the time of each sale.

Instead, they calculate the cost of all the goods sold during the accounting period at the end of the

period. To determine the cost of goods sold, a company must know:

- Beginning inventory (cost of goods on hand at the beginning of the period).

- Net cost of purchases during the period.

- Ending inventory (cost of unsold goods at the end of the period).

The company would show this information as follows:

In this schedule, notice that the company began the accounting period with USD 34,000 of

merchandise and purchased an additional USD 140,000, making a total of USD 174,000 of goods that

could have been sold during the period. Then, a physical inventory showed that USD 20,000 remained

unsold, which implies that USD 154,000 was the cost of goods sold during the period. Of course, the

USD 154,000 is not necessarily the precise amount of goods sold because no actual record was made of

the dollar cost of the goods sold. Periodic inventory procedure basically assumes that everything not on

hand at the end of the period has been sold. This method disregards problems such as theft or breakage

because the Merchandise Inventory account contains no up-to-date balance at the end of the

accounting period against which to compare the physical count.

Under periodic inventory procedure, a merchandising company uses the Purchases account to

record the cost of merchandise bought for resale during the current accounting period. The Purchases

account, which is increased by debits, appears with the income statement accounts in the chart of

accounts.

To illustrate entries affecting the Purchases account, assume that Hanlon Retail Food Store made

two purchases of merchandise from Smith Wholesale Company. Hanlon purchased USD 30,000 of

merchandise on credit (on account) on May 4, and on May 21 purchased USD 20,000 of merchandise

for cash. The required journal entries for Hanlon are:

The buyer deducts purchase discounts and purchase returns and allowances from purchases to

arrive at net purchases. The accountant records these items in contra accounts to the Purchases

account.

Purchase discounts Often companies purchase merchandise under credit terms that permit

them to deduct a stated cash discount if they pay invoices within a specified time. Assume that credit

terms for Hanlon's May 4 purchase are 2/10, n/30. If Hanlon pays for the merchandise by May 14, the

store may take a 2 per cent discount. Thus, Hanlon must pay only USD 29,400 to settle the USD

30,000 account payable. The entry to record the payment of the invoice on May 14 is:

The buyer records the purchase discount only when the invoice is paid within the discount period

and the discount is taken. The Purchase Discounts account is a contra account to Purchases that

reduces the recorded invoice price of the goods purchased to the price actually paid. Hanlon reports

purchase discounts in the income statement as a deduction from purchases.

Companies base purchase discounts on the invoice price of goods. If an invoice shows purchase

returns or allowances, they must be deducted from the invoice price before calculating purchase

discounts. For example, in the previous transaction, the invoice price of goods purchased was USD

30,000. If Hanlon returned USD 2,000 of the goods, the seller calculates the 2 per cent purchase

discount on USD 28,000.

Interest rate implied in cash discounts To decide whether you should take advantage of

discounts by using your cash or borrowing, make this simple analysis. Assume that you must pay USD

10,000 within 30 days or USD 9,800 within 10 days to settle a USD 10,000 invoice with terms of 2/10,

n/30. By advancing payment 20 days from the final due date, you can secure a discount of USD 200.

The interest expense incurred to borrow USD 9,800 at 12 per cent per year for 20 days is USD 65.33,

calculated as (USD 9,800 x .12 x 20/360). You would save USD 134.67 (USD 200 - USD 65.33) by

borrowing the money and paying the invoice within the discount period.

In terms of an annual rate of interest, the 2 per cent rate of discount for 20 days is equivalent to a

36 per cent annual rate: (360/20) X 2 per cent. The formula is:

You can convert all cash discount terms to their approximate annual interest rate equivalents by use

of this formula. Thus, a company could afford to pay up to 36 per cent [(360/20) X 2 per cent] on

borrowed funds to take advantage of discount terms of 2/10, n/ 30. The company could pay 18 per cent

on terms of 1/10, n/30.

Purchase returns and allowances A purchase return occurs when a buyer returns merchandise

to a seller. When a buyer receives a reduction in the price of goods shipped, a purchase allowance

results. Then, the buyer commonly uses a debit memorandum to notify the seller that the account

payable with the seller is being reduced (Accounts Payable is debited). The buyer may use a copy of a

debit memorandum to record the returns or allowances or may wait for confirmation, usually a credit

memorandum, from the seller.

Both returns and allowances reduce the buyer's debt to the seller and decrease the cost of the goods

purchased. The buyer may want to know the amount of returns and allowances as the first step in

controlling the costs incurred in returning unsatisfactory merchandise or negotiating purchase

allowances. For this reason, buyers record purchase returns and allowances in a separate Purchase

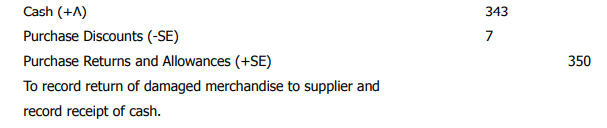

Returns and Allowances account. If Hanlon returned USD 350 of merchandise to Smith

Wholesale before paying for the goods, it would make this journal entry:

The entry would have been the same to record a USD 350 allowance. Only the explanation would

change.

If Hanlon had already paid the account, the debit would be to Cash instead of Accounts Payable,

since Hanlon would receive a refund of cash. If the company took a discount at the time it paid the

account, only the net amount would be refunded. For instance, if a 2 per cent discount had been taken,

Hanlon's journal entry for the return would be:

Purchase returns and allowances is a contra account to the Purchases account, and the income

statement shows it as a deduction from purchases. When both purchase discounts and purchase

returns and allowances are deducted from purchases, the result is net purchases.

Transportation costs are an important part of cost of goods sold. To understand how to account for

transportation costs, you must know the meaning of the following terms:

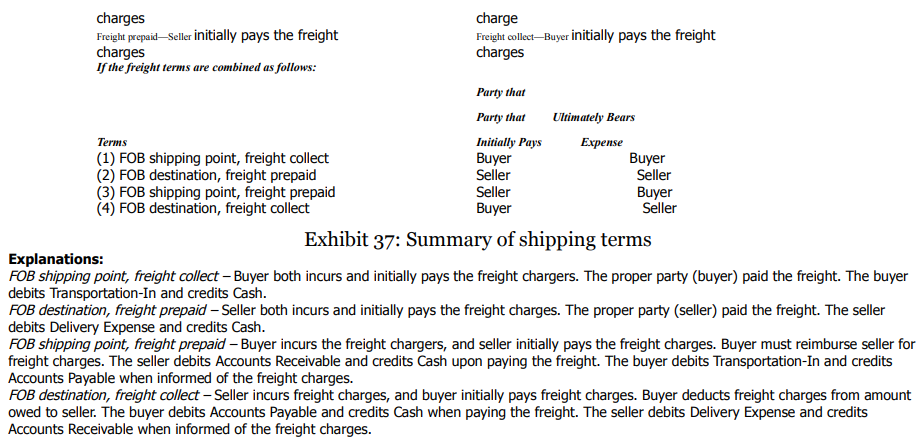

- FOB shipping point means "free on board at shipping point". The buyer incurs all transportation costs after the merchandise has been loaded on a railroad car or truck at the point of shipment. Thus, the buyer is responsible for ultimately paying the freight charges.

- FOB destination means "free on board at destination". The seller ships the goods to their destination without charge to the buyer. Thus, the seller is ultimately responsible for paying the freight charges.

- Passage of title is a term that indicates the transfer of the legal ownership of goods. Title to the goods normally passes from seller to buyer at the FOB point. Thus, when goods are shipped FOB shipping point, title usually passes to the buyer at the shipping point. When goods are shipped FOB destination, title usually passes at the destination.

- Freight prepaid means the seller must initially pay the freight at the time of shipment.

- Freight collect indicates the buyer must initially pay the freight bill on the arrival of the goods.

To illustrate the use of these terms, assume that a company ships goods FOB shipping point, freight. collect. Title passes at the shipping point. The buyer is responsible for paying the USD 100 freight costs and does so. The seller makes no entry for freight charges; the entry on the buyer's books is:

The Transportation-In account records the inward freight costs of acquiring merchandise.

Transportation-In is an adjunct account in that it is added to net purchases to arrive at net cost of purchases. An adjunct account is closely related to another account (Purchases, in this instance),

and its balance is added to the balance of the related account in the financial statements. Recall that a

contra account is just the opposite of an adjunct account. Buyers deduct a contra account, such as

accumulated depreciation, from the related fixed asset account in the financial statements.

When shipping goods FOB destination, freight prepaid, the seller is responsible for and pays the

freight bill. Because the seller cannot bill a separate freight cost to the buyer, the buyer shows no entry

for freight on its books. The seller, however, has undoubtedly considered the freight cost in setting

selling prices. The following entry is required on the seller's books:

When the terms are FOB destination, the seller records the freight costs as delivery expense; this

selling expense appears on the income statement with other selling expenses.

FOB terms are especially important at the end of an accounting period. Goods in transit then belong

to either the seller or the buyer, and one of these parties must include these goods in its ending

inventory. Goods shipped FOB destination belong to the seller while in transit, and the seller includes

these goods in its ending inventory. Goods shipped FOB shipping point belong to the buyer while in

transit, and the buyer records these goods as a purchase and includes them in its ending inventory. For

example, assume that a seller ships goods on 2009 December 30, and they arrive at their destination

on 2010 January 5. If terms are FOB destination, the seller includes the goods in its 2009 December

31, inventory, and neither seller nor buyer records the exchange transaction until 2010 January 5. If

terms are FOB shipping point, the buyer includes the goods in its 2009 December 31, inventory, and

both parties record the exchange transaction as of 2009 December 30.

Sometimes the seller prepays the freight as a convenience to the buyer, even though the buyer is

ultimately responsible for it. The buyer merely reimburses the seller for the freight paid. For example,

assume that Wood Company sold merchandise to Loud Company with terms of FOB shipping point,

freight prepaid. The freight charges were USD 100. The following entries are necessary on the books of

the buyer and the seller:

Such entries are necessary because Wood initially paid the freight charges when not required to do

so. Therefore, Loud Company must reimburse Wood for the charges. If the buyer pays freight for the

seller (e.g. FOB destination, freight collect), the buyer merely deducts the freight paid from the amount

owed to the seller. The following entries are necessary on the books of the buyer and the seller:

Purchase discounts may be taken only on the purchase price of goods. Therefore, a buyer who owes

the seller for freight charges cannot take a discount on the freight charges owed, even if the buyer

makes payment within the discount period. We summarize our discussion of freight terms and the

resulting journal entries to record the freight charges in Exhibit 37.

Merchandise inventory is the cost of goods on hand and available for sale at any given time. To

determine the cost of goods sold in any accounting period, management needs inventory information.

Management must know its cost of goods on hand at the start of the period (beginning inventory), the

net cost of purchases during the period, and the cost of goods on hand at the close of the period

(ending inventory). Since the ending inventory of the preceding period is the beginning inventory for

the current period, management already knows the cost of the beginning inventory. Companies record

purchases, purchase discounts, purchase returns and allowances, and transportation-in throughout the

period. Therefore, management needs to determine only the cost of the ending inventory at the end of

the period in order to calculate cost of goods sold.

Taking a physical inventory Under periodic inventory procedure, company personnel

determine ending inventory cost by taking a physical inventory. Taking a physical inventory

consists of counting physical units of each type of merchandise on hand. To calculate inventory cost,

they multiply the number of each kind of merchandise by its unit cost. Then, they combine the total

costs of the various kinds of merchandise to provide the total ending inventory cost.

In taking a physical inventory, company personnel must be careful to count all goods owned,

regardless of where they are located, and include them in the inventory.

Thus, companies should include goods shipped to potential customers on approval in their

inventories. Similarly, companies should not record consigned goods (goods delivered to another

party who attempts to sell them for a commission) as sold goods. These goods remain the property of

the owner (consignor) until sold by the consignee and must be included in the owner's inventory.

Merchandise in transit is merchandise in the hands of a freight company on the date of a

physical inventory. As stated above, buyers must record merchandise in transit at the end of the

accounting period as a purchase if the goods were shipped FOB shipping point and they have received

title to the merchandise. In general, the goods belong to the party who ultimately bears the

transportation charges.

When accounting personnel know the beginning and ending inventories and the various items

making up the net cost of purchases, they can determine the cost of goods sold. To illustrate, assume

the following account balances for Hanlon Retail Food Store as of 2010 December 31:

By taking a physical inventory, Hanlon determined the 2010 December 31, merchandise inventory

to be USD 31,000. Hanlon then calculated its cost of goods sold as shown in Exhibit 38. This

computation appears in a section of the income statement directly below the calculation of net sales.

In Exhibit 38, Hanlon's beginning inventory (USD 24,000) plus net cost of purchases (USD

166,000) is equal to cost of goods available for sale (USD 190,000). The firm deducts the ending

inventory cost (USD 31,000) from cost of goods available for sale to arrive at cost of goods sold (USD

159,000).

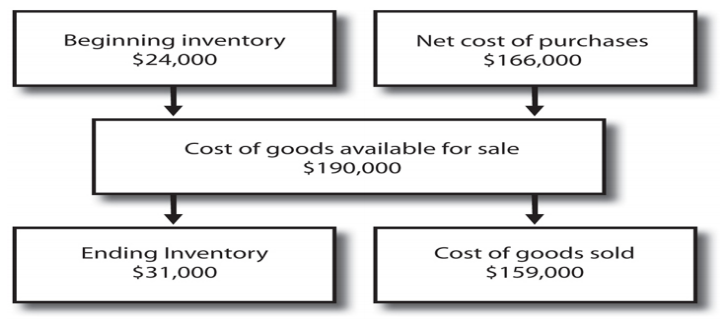

Another way of looking at this relationship is the following diagram:

Beginning inventory and net cost of purchases combine to form cost of goods available for sale.

Hanlon divides the cost of goods available for sale into ending inventory (which is the cost of goods not

sold) and cost of goods sold.

To continue the calculation appearing in Exhibit 38, net cost of purchases (USD 166,000) is equal

to purchases (USD 167,000), less purchase discounts (USD 3,000) and purchase returns and

allowances (USD 8,000), plus transportation-in (USD 10,000).

As shown in Exhibit 38, ending inventory cost (merchandise inventory) appears in the income

statement as a deduction from cost of goods available for sale to compute cost of goods sold. Ending

inventory cost (merchandise inventory) is also a current asset in the end-of-period balance sheet.

Companies use periodic inventory procedure because of its simplicity and relatively low cost.

However, periodic inventory procedure provides little control over inventory. Firms assume any items

not included in the physical count of inventory at the end of the period have been sold. Thus, they

mistakenly assume items that have been stolen have been sold and include their cost in cost of goods

sold.

To illustrate, suppose that the cost of goods available for sale was USD 200,000 and ending inventory was USD 60,000. These figures suggest that the cost of goods sold was USD 140,000. Now suppose that USD 2,000 of goods were actually shoplifted during the year. If such goods had not been stolen, the ending inventory would have been USD 62,000 and the cost of goods sold only USD 138,000. Thus, the USD 140,000 cost of goods sold calculated under periodic inventory procedure includes both the cost of the merchandise delivered to customers and the cost of merchandise stolen.