Reading: Lesson 1 - Inventories and cost of goods sold

Importance of proper inventory valuation

A merchandising company can prepare accurate income statements, statements of retained

earnings, and balance sheets only if its inventory is correctly valued. On the income statement, a

company using periodic inventory procedure takes a physical inventory to determine the cost of goods

sold. Since the cost of goods sold figure affects the company's net income, it also affects the balance of

retained earnings on the statement of retained earnings. On the balance sheet, incorrect inventory

amounts affect both the reported ending inventory and retained earnings. Inventories appear on the

balance sheet under the heading "Current Assets", which reports current assets in a descending order

of liquidity. Because inventories are consumed or converted into cash within a year or one operating

cycle, whichever is longer, inventories usually follow cash and receivables on the balance sheet.

Recall that under periodic inventory procedure we determine the cost of goods sold figure by adding

the beginning inventory to the net cost of purchases and deducting the ending inventory. In each

accounting period, the appropriate expenses must be matched with the revenues of that period to

determine the net income. Applied to inventory, matching involves determining (1) how much of the

cost of goods available for sale during the period should be deducted from current revenues and (2)

how much should be allocated to goods on hand and thus carried forward as an asset (merchandise

inventory) in the balance sheet to be matched against future revenues. Because we determine the cost

of goods sold by deducting the ending inventory from the cost of goods available for sale, a highly

significant relationship exists: Net income for an accounting period depends directly on the valuation

of ending inventory. This relationship involves three items:

First, a merchandising company must be sure that it has properly valued its ending inventory. If the

ending inventory is overstated, cost of goods sold is understated, resulting in an overstatement of gross

margin and net income. Also, overstatement of ending inventory causes current assets, total assets, and

retained earnings to be overstated. Thus, any change in the calculation of ending inventory is reflected,

dollar for dollar (ignoring any income tax effects), in net income, current assets, total assets, and

retained earnings.

Second, when a company misstates its ending inventory in the current year, the company carries

forward that misstatement into the next year. This misstatement occurs because the ending inventory

amount of the current year is the beginning inventory amount for the next year.

Third, an error in one period's ending inventory automatically causes an error in net income in the

opposite direction in the next period. After two years, however, the error washes out, and assets and

retained earnings are properly stated.

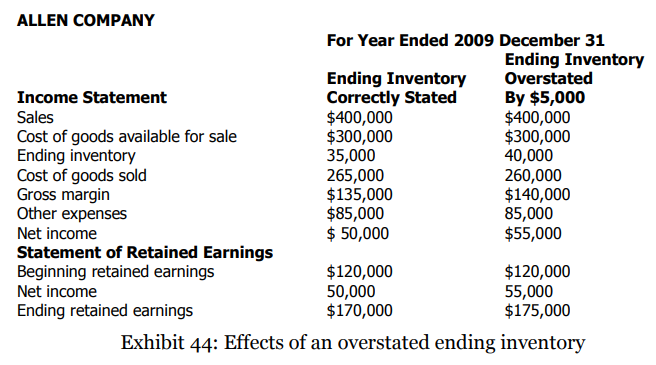

Exhibit 44 and Exhibit 45 prove that net income for an accounting period depends directly on the

valuation of the inventory. Allen Company's income statements and the statements of retained

earnings for years 2009 and 2010 show this relationship.

In Exhibit 44 the correctly stated ending inventory for the year 2009 is USD 35,000. As a result,

Allen has a gross margin of USD 135,000 and net income of USD 50,000. The statement of retained

earnings shows a beginning retained earnings of USD 120,000 and an ending retained earnings of USD

170,000. When the ending inventory is overstated by USD 5,000, as shown on the right in Exhibit 44,

the gross margin is USD 140,000, and net income is USD 55,000. The statement of retained earnings. then has an ending retained earnings of USD 175,000. The ending inventory overstatement of USD

5,000 causes a USD 5,000 overstatement of net income and a USD 5,000 overstatement of retained

earnings. The balance sheet would show both an overstated inventory and an overstated retained

earnings. Due to the error in ending inventory, both the stockholders and creditors may overestimate

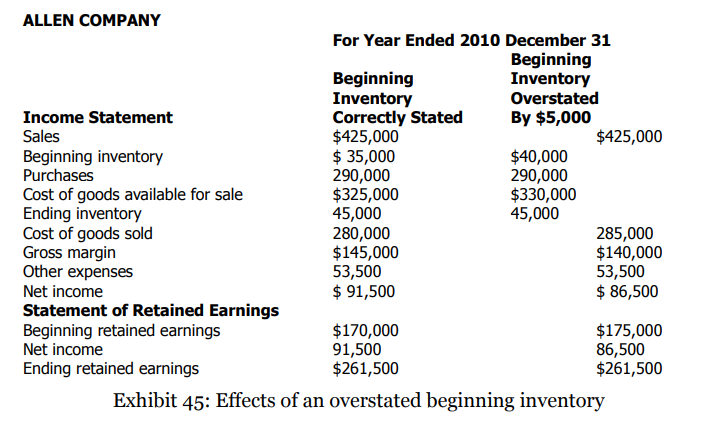

the profitability of the business. Exhibit 45 is a continuation of Exhibit 44 and contains Allen's operating results for the year ended

2010 December 31. Note that the ending inventory in Exhibit 44 now becomes the beginning inventory

of Exhibit 45. However, Allen's inventory at 2010 December 31, is now an accurate inventory of USD

45,000. As a result, the gross margin in the income statement with the beginning inventory correctly

stated is USD 145,000, and Allen Company has net income of USD 91,500 and an ending retained

earnings of USD 261,500. In the income statement columns at the right, in which the beginning

inventory is overstated by USD 5,000, the gross margin is USD 140,000 and net income is USD

86,500, with the ending retained earnings also at USD 261,500. Thus, in contrast to an overstated ending inventory, resulting in an overstatement of net income, an

overstated beginning inventory results in an understatement of net income. If the beginning inventory

is overstated, then cost of goods available for sale and cost of goods sold also are overstated.

Consequently, gross margin and net income are understated. Note, however, that when net income in

the second year is closed to retained earnings, the retained earnings account is stated at its proper

amount. The overstatement of net income in the first year is offset by the understatement of net

income in the second year. For the two years combined the net income is correct. At the end of the

second year, the balance sheet contains the correct amounts for both inventory and retained earnings.

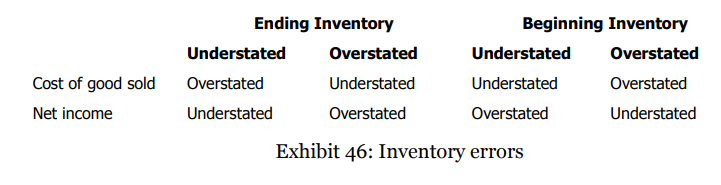

Exhibit 46 summarizes the effects of errors of inventory valuation: