Reading: Lesson 2 - Current liabilities

Note the definition of a current liability uses the term operating cycle. An

operating cycle (or cash cycle) is the time it takes to begin with cash, buy necessary

items to produce revenues (such as materials, supplies, labor, and/or finished goods),

sell goods or services, and receive cash by collecting the resulting receivables. For most

companies, this period is no longer than a few months. Service companies generally

have the shortest operating cycle, since they have no cash tied up in inventory.

Manufacturing companies generally have the longest cycle because their cash is tied up

in inventory accounts and in accounts receivable before coming back. Even for

manufacturing companies, the cycle is generally less than one year. Thus, as a practical matter, current liabilities are due in one year or less, and long-term liabilities are due

after one year from the balance sheet date.

Current liabilities fall into these three groups:

- Clearly determinable liabilities. The existence of the liability and its

amount are certain. Examples include most of the liabilities discussed previously,

such as accounts payable, notes payable, interest payable, unearned delivery fees,

and wages payable. Sales tax payable, federal excise tax payable, current portions

of long-term debt, and payroll liabilities are other examples.

- Estimated liabilities. The existence of the liability is certain, but its amount

only can be estimated. An example is estimated product warranty payable.

- Contingent liabilities. The existence of the liability is uncertain and usually

the amount is uncertain because contingent liabilities depend (or are contingent)

on some future event occurring or not occurring. Examples include liabilities

arising from lawsuits, discounted notes receivable, income tax disputes, penalties

that may be assessed because of some past action, and failure of another party to

pay a debt that a company has guaranteed.

The following table summarizes the characteristics of current liabilities:

Clearly determinable liabilities have clearly determinable amounts. In this section,

we describe liabilities not previously discussed that are clearly determinable—sales tax

payable, federal excise tax payable, current portions of long-term debt, and payroll

liabilities. Later in this chapter, we discuss clearly determinable liabilities such as notes

payable.

Sales tax payable Many states have a state sales tax on items purchased by

consumers. The company selling the product is responsible for collecting the sales tax

from customers. When the company collects the taxes, the debit is to Cash and the

credit is to Sales Tax Payable. Periodically, the company pays the sales taxes collected

to the state. At that time, the debit is to Sales Tax Payable and the credit is to Cash.

To illustrate, assume that a company sells merchandise in a state that has a 6

percent sales tax. If it sells goods with a sales price of USD 1,000 on credit, the

company makes this entry:

Now assume that sales for the entire period are USD 100,000 and that USD 6,000 is

in the Sales Tax Payable account when the company remits the funds to the state taxing

agency. The following entry shows the payment to the state:

An alternative method of recording sales taxes payable is to include these taxes in

the credit to Sales. For instance, the previous company could record sales as follows:

When recording sales taxes in the same account as sales revenue, the firm must

separate the sales tax from sales revenue at the end of the accounting period. To make

this separation, it adds the sales tax rate to 100 percent and divides this percentage

into recorded sales revenue. For instance, assume that total recorded sales revenues for

an accounting period are USD 10,600, and the sales tax rate is 6 percent. To find the

sales revenue, use the following formula:

The sales revenue is USD 10,000 for the period. Sales tax is equal to the recorded

sales revenue of USD 10,600 less actual sales revenue of USD 10,000, or USD 600.

Federal excise tax payable Consumers pay federal excise tax on some goods,

such as alcoholic beverages, tobacco, gasoline, cosmetics, tires, and luxury

automobiles. The entries a company makes when selling goods subject to the federal

excise tax are similar to those made for sales taxes payable. For example, assume that

the Dixon Jewelry Store sells a diamond ring to a young couple for USD 2,000. The

sale is subject to a 6 percent sales tax and a 10 percent federal excise tax. The entry to

record the sale is:

The company records the remittance of the taxes to the federal taxing agency by

debiting Federal Excise Tax Payable and crediting Cash.

Current portions of long-term debt Accountants move any portion of longterm

debt that becomes due within the next year to the current liability section of the

balance sheet. For instance, assume a company signed a series of 10 individual notes

payable for USD 10,000 each; beginning in the 6th year, one comes due each year

through the 15th year. Beginning in the 5th year, an accountant would move a USD

10,000 note from the long-term liability category to the current liability category on

the balance sheet. The current portion would then be paid within one year.

Payroll liabilities In most business organizations, accounting for payroll is

particularly important because (1) payrolls often are the largest expense that a

company incurs, (2) both federal and state governments require maintaining detailed

payroll records, and (3) companies must file regular payroll reports with state and

federal governments and remit amounts withheld or otherwise due. Payroll liabilities

include taxes and other amounts withheld from employees' paychecks and taxes paid

by employers.

Employers normally withhold amounts from employees' paychecks for federal

income taxes; state income taxes; FICA (social security) taxes; and other items such as

union dues, medical insurance premiums, life insurance premiums, pension plans, and

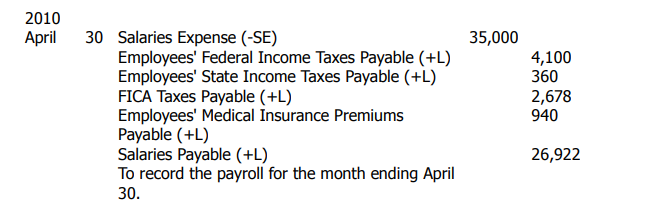

pledges to charities. Assume that a company had a payroll of USD 35,000 for the

month of April 2010. The company withheld the following amounts from the

employees' pay: federal income taxes, USD 4,100; state income taxes, USD 360; FICA

taxes, USD 2,678; and medical insurance premiums, USD 940. This entry records the

payroll:

All accounts credited in the entry are current liabilities and will be reported on the

balance sheet if not paid prior to the preparation of financial statements. When these

liabilities are paid, the employer debits each one and credits Cash.

Employers normally record payroll taxes at the same time as the payroll to which

they relate. Assume the payroll taxes an employer pays for April are FICA taxes, USD

2,678; state unemployment taxes, USD 1,890; and federal unemployment taxes, USD

280. The entry to record these payroll taxes would be:

These amounts are in addition to the amounts withheld from employees' paychecks.

The credit to FICA Taxes Payable is equal to the amount withheld from the employees'

paychecks. The company can credit both its own and the employees' FICA taxes to the

same liability account, since both are payable at the same time to the same agency.

When these liabilities are paid, the employer debits each of the liability accounts and

credits Cash.

Managers of companies that have estimated liabilities know these liabilities exist but

can only estimate the amount. The primary accounting problem is to estimate a

reasonable liability as of the balance sheet date. An example of an estimated liability is

product warranty payable.

Estimated product warranty payable When companies sell products such as

computers, often they must guarantee against defects by placing a warranty on their

products. When defects occur, the company is obligated to reimburse the customer or

repair the product. For many products, companies can predict the number of defects

based on experience. To provide for a proper matching of revenues and expenses, the

accountant estimates the warranty expense resulting from an accounting period's sales.

The debit is to Product Warranty Expense and the credit to Estimated Product

Warranty Payable.

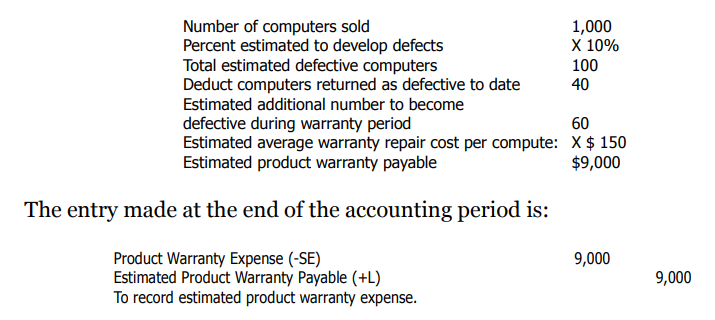

To illustrate, assume that a company sells personal computers and warrants all

parts for one year. The average price per computer is USD 1,500, and the company

sells 1,000 computers in 2010. The company expects 10 percent of the computers to develop defective parts within one year. By the end of 2010, customers have returned

40 computers sold that year for repairs, and the repairs on those 40 computers have

been recorded. The estimated average cost of warranty repairs per defective computer

is USD 150. To arrive at a reasonable estimate of product warranty expense, the

accountant makes the following calculation:

When a customer returns one of the computers purchased in 2010 for repair work in

2008 (during the warranty period), the company debits the cost of the repairs to

Estimated Product Warranty Payable. For instance, assume that Evan Holman returns

his computer for repairs within the warranty period. The repair cost includes parts,

USD 40, and labor, USD 160. The company makes the following entry:

When liabilities are contingent, the company usually is not sure that the liability

exists and is uncertain about the amount. FASB Statement No. 5 defines a contingency

as "an existing condition, situation, or set of circumstances involving uncertainty as to

possible gain or loss to an enterprise that will ultimately be resolved when one or more

future events occur or fail to occur".

According to FASB Statement No. 5, if the liability is probable and the amount can

be reasonably estimated, companies should record contingent liabilities in the

accounts. However, since most contingent liabilities may not occur and the amount

often cannot be reasonably estimated, the accountant usually does not record them in

the accounts. Instead, firms typically disclose these contingent liabilities in notes to

their financial statements.

Many contingent liabilities arise as the result of lawsuits. In fact, 469 of the 957

companies contacted in the AICPA's annual survey of accounting practices reported

contingent liabilities resulting from litigation.

The following two examples from annual reports are typical of the disclosures made

in notes to the financial statements. Be aware that just because a suit is brought, the

company being sued is not necessarily guilty. One company included the following note

in its annual report to describe its contingent liability regarding various lawsuits

against the company:

Contingent liabilities:

Various lawsuits and claims, including those involving ordinary routine litigation

incidental to its business, to which the Company is a party, are pending, or have been

asserted, against the Company. In addition, the Company was advised...that the United

States Environmental Protection Agency had determined the existence of PCBs in a

river and harbor near Sheboygan, Wisconsin,USA, and that the Company, as well as

others, allegedly contributed to that contamination. It is not presently possible to

determine with certainty what corrective action, if any, will be required, what portion

of any costs thereof will be attributable to the Company, or whether all or any portion

of such costs will be covered by insurance or will be recoverable from others. Although

the outcome of these matters cannot be predicted with certainty, and some of them

may be disposed of unfavorably to the Company, management has no reason to believe

that their disposition will have a materially adverse effect on the consolidated financial

position of the Company.

Another company dismissed an employee and included the following note to

disclose the contingent liability resulting from the ensuing litigation:

Contingencies:

A jury awarded USD 5.2 million to a former employee of the Company for an

alleged breach of contract and wrongful termination of employment. The Company has

appealed the judgment on the basis of errors in the judge's instructions to the jury and

insufficiency of evidence to support the amount of the jury's award. The Company is

vigorously pursuing the appeal.

The Company and its subsidiaries are also involved in various other litigation

arising in the ordinary course of business.

Since it presently is not possible to determine the outcome of these matters, no

provision has been made in the financial statements for their ultimate resolution. The

resolution of the appeal of the jury award could have a significant effect on the

Company's earnings in the year that a determination is made; however, in

management's opinion, the final resolution of all legal matters will not have a material

adverse effect on the Company's financial position.

Contingent liabilities may also arise from discounted notes receivable, income tax

disputes, penalties that may be assessed because of some past action, and failure of

another party to pay a debt that a company has guaranteed.

The remainder of this chapter discusses notes receivable and notes payable. Business transactions often involve one party giving another party a note.