Reading: Lesson 3 - Notes receivable and notes payable

A customer may give a note to a business for an amount due on an account

receivable or for the sale of a large item such as a refrigerator. Also, a business may give

a note to a supplier in exchange for merchandise to sell or to a bank or an individual for

a loan. Thus, a company may have notes receivable or notes payable arising from

transactions with customers, suppliers, banks, or individuals.

Companies usually do not establish a subsidiary ledger for notes. Instead, they

maintain a file of the actual notes receivable and copies of notes payable.

Most promissory notes have an explicit interest charge. Interest is the fee charged

for use of money over a period. To the maker of the note, or borrower, interest is an

expense; to the payee of the note, or lender, interest is a revenue. A borrower incurs

interest expense; a lender earns interest revenue. For convenience, bankers sometimes

calculate interest on a 360-day year; we calculate it on that basis in this text. (Some

companies use a 365-day year.)

Principal is the face value of the note. The rate is the stated interest rate on the

note; interest rates are generally stated on an annual basis. Time, which is the amount

of time the note is to run, can be either days or months.

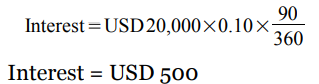

To show how to calculate interest, assume a company borrowed USD 20,000 from a

bank. The note has a principal (face value) of USD 20,000, an annual interest rate of 10

percent, and a life of 90 days. The interest calculation is:

Note that in this calculation we expressed the time period as a fraction of a 360-day

year because the interest rate is an annual rate.

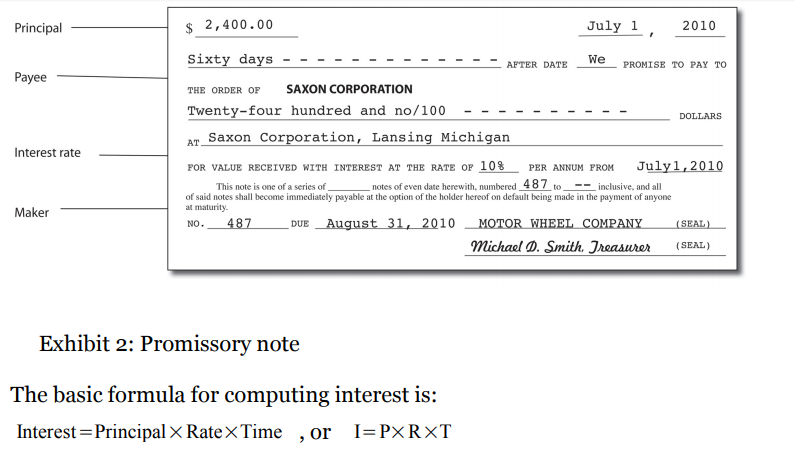

The maturity date is the date on which a note becomes due and must be paid.

Sometimes notes require monthly installments (or payments) but usually all of the

principal and interest must be paid at the same time as in Exhibit 2. The wording in the

note expresses the maturity date and determines when the note is to be paid. A note

falling due on a Sunday or a holiday is due on the next business day. Examples of the

maturity date wording are:

- On demand. "On demand, I promise to pay..." When the maturity date is on

demand, it is at the option of the holder and cannot be computed. The holder is the

payee, or another person who legally acquired the note from the payee.

- On a stated date. "On 2010 July 18, I promise to pay..." When the maturity date

is designated, computing the maturity date is not necessary.

- At the end of a stated period.

(a)"One year after date, I promise to pay..." When the maturity is expressed in years, the note matures on the same day of the same month as the date of the note in the year of maturity.

(b)"Four months after date, I promise to pay..." When the maturity is expressed in months, the note matures on the same date in the month of maturity. For example, one month from 2010 July 18, is 2010 August 18, and two months from 2010 July 18, is 2010 September 18. If a note is issued on the last day of a month and the month of maturity has fewer days than the month of issuance, the note matures on the last day of the month of maturity. A one-month note dated 2010 January 31, matures on 2010 February 28.

(c)“Ninety days after date, I promise to pay..." When the maturity is expressed in days, the exact number of days must be counted. The first day (date of origin) is omitted, and the last day (maturity date) is included in the count. For example, a 90-day note dated 2010 October 19, matures on 2008 January 17, as shown here:

Sometimes a company receives a note when it sells high-priced merchandise; more

often, a note results from the conversion of an overdue account receivable. When a

customer does not pay an account receivable that is due, the company (creditor) may

insist that the customer (debtor) gives a note in place of the account receivable. This

action allows the customer more time to pay the balance due, and the company earns interest on the balance until paid. Also, the company may be able to sell the note to a

bank or other financial institution. To illustrate the conversion of an account receivable to a note, assume that Price

Company (maker) had purchased USD 18,000 of merchandise on August 1 from

Cooper Company (payee) on account. The normal credit period has elapsed, and Price

cannot pay the invoice. Cooper agrees to accept Price's USD 18,000, 15 percent, 90-day

note dated September 1 to settle Price's open account. Assuming Price paid the note at

maturity and both Cooper and Price have a December 31 year-end, the entries on the

books of the payee and the maker are:

The USD 18,675 paid by Price to Cooper is called the maturity value of the note.

Maturity value is the amount that the maker must pay on a note on its maturity date;

typically, it includes principal and accrued interest, if any. Sometimes the maker of a note does not pay the note when it becomes due. The next

section describes how to record a note not paid at maturity.

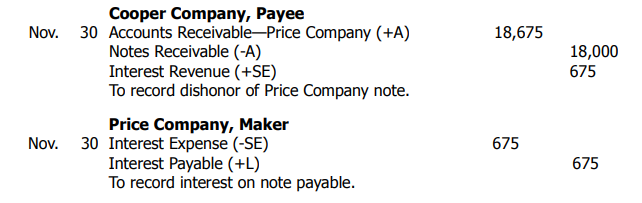

A dishonored note is a note that the maker failed to pay at maturity. Since the

note has matured, the holder or payee removes the note from Notes Receivable and

records the amount due in Accounts Receivable (or Dishonored Notes Receivable).

At the maturity date of a note, the maker should pay the principal plus interest. If

the interest has not been accrued in the accounting records, the maker of a dishonored

note should record interest expense for the life of the note by debiting Interest Expense

and crediting Interest Payable. The payee should record the interest earned and

remove the note from its Notes Receivable account. Thus, the payee of the note should

debit Accounts Receivable for the maturity value of the note and credit Notes

Receivable for the note's face value and Interest Revenue for the interest. After these

entries have been posted, the full liability on the note—principal plus interest—is

included in the records of both parties. Interest continues to accrue on the note until it

is paid, replaced by a new note, or written off as uncollectible. To illustrate, assume

that Price did not pay the note at maturity. The entries on each party's books are:

When unable to pay a note at maturity, sometimes the maker pays the interest on

the original note or includes the interest in the face value of a new note that replaces

the old note. Both parties account for the new note in the same manner as the old note.

However, if it later becomes clear that the maker of a dishonored note will never pay,

the payee writes off the account with a debit to Uncollectible Accounts Expense (or to

an account with a title such as Loss on Dishonored Notes) and a credit to Accounts

Receivable. The debit should be to the Allowance for Uncollectible Accounts if the

payee made an annual provision for uncollectible notes receivable.

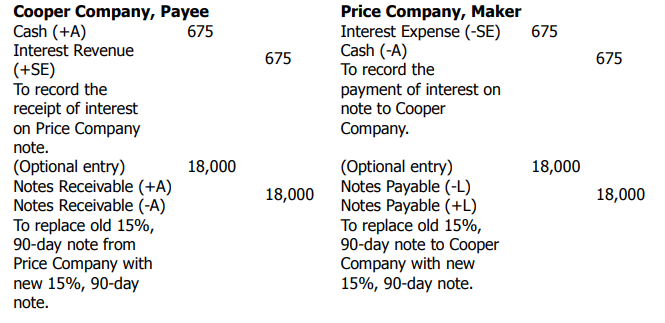

Assume that Price Company pays the interest at the maturity date and issues a new

15 percent, 90-day note for USD 18,000. The entries on both sets of books would be:

Although the second entry on each set of books has no effect on the existing account

balances, it indicates that the old note was renewed (or replaced). Both parties

substitute the new note, or a copy, for the old note in a file of notes.

Now assume that Price Company does not pay the interest at the maturity date but

instead includes the interest in the face value of the new note. The entries on both sets

of books would be:

On an interest-bearing note, even though interest accrues, or accumulates, on a dayto-day

basis, usually both parties record it only at the note's maturity date. If the note

is outstanding at the end of an accounting period, however, the time period of the

interest overlaps the end of the accounting period and requires an adjusting entry at

the end of the accounting period. Both the payee and maker of the note must make an

adjusting entry to record the accrued interest and report the proper assets and

revenues for the payee and the proper liabilities and expenses for the maker. Failure to

record accrued interest understates the payee's assets and revenues by the amount of

the interest earned but not collected and understates the maker's expenses and

liabilities by the interest expense incurred but not yet paid.

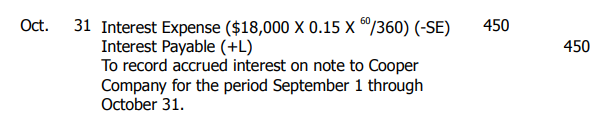

Payee's books To illustrate how to record accrued interest on the payee's books,

assume that the payee, Cooper Company, has a fiscal year ending on October 31 instead

of December 31. On October 31, Cooper would make the following adjusting entry

relating to the Price Company note:

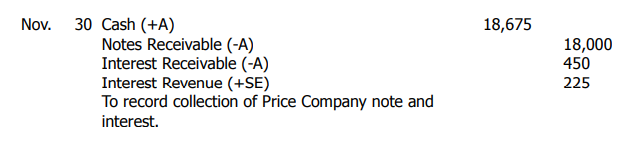

The Interest Receivable account shows the interest earned but not yet collected.

Interest receivable is a current asset in the balance sheet because the interest will be

collected in 30 days. The interest revenue appears in the income statement. When Price

pays the note on November 30, Cooper makes the following entry to record the

collection of the note's principal and interest:

Note that the entry credits the Interest Receivable account for the USD 450 interest

accrued from September 1 through October 31, which was debited to the account in the

previous entry, and credits Interest Revenue for the USD 225 interest earned in

November.

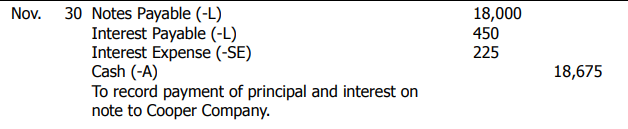

Maker's books Assume Price Company's accounting year also ends on October 31

instead of December 31. Price's accounting records would be incomplete unless the

company makes an adjusting entry to record the liability owed for the accrued interest

on the note it gave to Cooper Company. The required entry is:

The Interest Payable account, which shows the interest expense incurred but

not yet paid, is a current liability in the balance sheet because the interest will be paid

in 30 days. Interest expense appears in the income statement. When the note is paid,

Price makes the following entry:

In this illustration, Cooper's financial position made it possible for the company to carry the Price note to the maturity date. Alternatively, Cooper could have sold, or discounted, the note to receive the proceeds before the maturity date. This topic is reserved for a more advanced text.