Reading: Lesson 3 - Initial recording of plant assets

The next sections discuss which costs are capitalized (debited to an asset account)

for: (1) land and land improvements; (2) buildings; (3) group purchases of assets; (4)

machinery and other equipment; (5) self-constructed assets; (6) noncash acquisitions;

and (7) gifts of plant assets.

The cost of land includes its purchase price and other costs such as option cost, real

estate commissions, title search and title transfer fees, and title insurance premiums.

Also included are an existing mortgage note or unpaid taxes (back taxes) assumed by

the purchaser; costs of surveying, clearing, and grading; and local assessments for

sidewalks, streets, sewers, and water mains. Sometimes land purchased as a building

site contains an unusable building that must be removed. Then, the accountant debits

the entire purchase price to Land, including the cost of removing the building less any

cash received from the sale of salvaged items while the land is being readied for use.

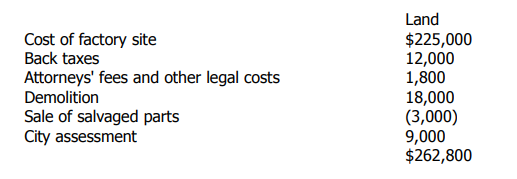

To illustrate, assume that Spivey Company purchased an old farm on the outskirts

of San Diego, California,USA, as a factory site. The company paid USD 225,000 for the

property. In addition, the company agreed to pay unpaid property taxes from previous

periods (called back taxes) of USD 12,000. Attorneys' fees and other legal costs relating

to the purchase of the farm totaled USD 1,800. Spivey demolished (razed) the farm

buildings at a cost of USD 18,000. The company salvaged some of the structural pieces

of the building and sold them for USD 3,000. Because the firm was constructing a new

building at the site, the city assessed Spivey Company USD 9,000 for water mains,

sewers, and street paving. Spivey computed the cost of the land as follows:

Accountants assigned all costs relating to the farm purchase and razing of the old

buildings to the Land account because the old buildings purchased with the land were

not usable. The real goal was to purchase the land, but the land was not available

without the buildings. Land is considered to have an unlimited life and is therefore not depreciable.

However, land improvements, including driveways, temporary landscaping,

parking lots, fences, lighting systems, and sprinkler systems, are attachments to the

land. They have limited lives and therefore are depreciable. Owners record depreciable

land improvements in a separate account called Land Improvements. They record the

cost of permanent landscaping, including leveling and grading, in the Land account.

When a business buys a building, its cost includes the purchase price, repair and

remodeling costs, unpaid taxes assumed by the purchaser, legal costs, and real estate

commissions paid.

Determining the cost of constructing a new building is often more difficult. Usually

this cost includes architect's fees; building permits; payments to contractors; and the

cost of digging the foundation. Also included are labor and materials to build the

building; salaries of officers supervising the construction; and insurance, taxes, and

interest during the construction period. Any miscellaneous amounts earned from the

building during construction reduce the cost of the building. For example, an owner

who could rent out a small completed portion during construction of the remainder of

the building, would credit the rental proceeds to the Buildings account rather than to a

revenue account.

Sometimes a company buys land and other assets for a lump sum. When land and

buildings purchased together are to be used, the firm divides the total cost and

establishes separate ledger accounts for land and for buildings. This division of cost

establishes the proper balances in the appropriate accounts. This is especially

important later because the depreciation recorded on the buildings affects reported

income, while no depreciation is taken on the land.

Returning to our example of Spivey Company, suppose one of the farm buildings

was going to be remodeled for use by the company. Then, Spivey would determine

what portion of the purchase price of the farm, back taxes, and legal fees (USD

225,000 + USD 12,000 + USD 1,800 = USD 238,800) it could assign to the buildings

and what portion to the land. (The net cost of demolition would not be incurred, and

the city assessment would be incurred at a later time.) Spivey would assign the USD

238,800 to the land and the buildings on the basis of their appraised values. For

example, assume that the land was appraised at USD 162,000 and the buildings at USD 108,000. Spivey would determine the cost assignable to each of these plant assets

as follows:

When the city eventually assessed the charges for the water mains, sewers, and

street paving, the company would still debit these costs to the Land account as in the

previous example.

Often companies purchase machinery or other equipment such as delivery or office

equipment. Its cost includes the seller's net invoice price (whether the discount is taken

or not), transportation charges incurred, insurance in transit, cost of installation, costs

of accessories, and testing and break-in costs. Also included are other costs needed to

put the machine or equipment in operating condition in its intended location. The cost

of machinery does not include removing and disposing of a replaced, old machine that

has been used in operations. Such costs are part of the gain or loss on disposal of the

old machine.

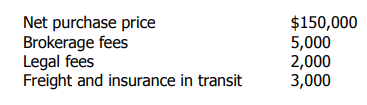

To illustrate, assume that Clark Company purchased new equipment to replace

equipment that it has used for five years. The company paid a net purchase price of

USD 150,000, brokerage fees of USD 5,000, legal fees of USD 2,000, and freight and

insurance in transit of USD 3,000. In addition, the company paid USD 1,500 to remove

old equipment and USD 2,000 to install new equipment. Clark would compute the cost

of new equipment as follows:

If a company builds a plant asset for its own use, the cost includes all materials and

labor directly traceable to construction of the asset. Also included in the cost of the

asset are interest costs related to the asset and amounts paid for utilities (such as heat,

light, and power) and for supplies used during construction. To determine how much

of these indirect costs to capitalize, the company compares utility and supply costs

during the construction period with those costs in a period when no construction

occurred. The firm records the increase as part of the asset's cost. For example, assume

a company normally incurred a USD 600 utility bill for June. This year, the company

constructed a machine during June, and the utility bill was USD 975. Thus, it records

the USD 375 increase as part of the machine's cost.

To illustrate further, assume that Tanner Company needed a new die-casting

machine and received a quote from Smith Company for USD 23,000, plus USD 1,000

freight costs. Tanner decided to build the machine rather than buy it. The company

incurred the following costs to build the machine: materials, USD 4,000; labor, USD

13,000; and indirect services of heat, power, and supplies, USD 3,000. Tanner would

record the machine at its cost of USD 20,000 (USD 4,000 + USD 13,000 + USD

3,000) rather than USD 24,000, the purchase price of the machine. The USD 20,000 is

the cost of the resources given up to construct the machine. Also, recording the

machine at USD 24,000 would require Tanner to recognize a gain on construction of

the assets. Accountants do not subscribe to the idea that a business can earn revenue

(or realize a gain), and therefore net income, by dealing with itself.

You can apply the general guidelines we have just discussed to other plant assets,

such as furniture and fixtures. The accounting methods are the same.

When a plant asset is purchased for cash, its acquisition cost is simply the agreed on

cash price. However, when a business acquires plant assets in exchange for other

noncash assets (shares of stock, a customer's note, or a tract of land) or as gifts, it is

more difficult to establish a cash price. This section discusses three possible asset

valuation bases.

The general rule on noncash exchanges is to value the noncash asset received at its

fair market value or the fair market value of what was given up, whichever is more

clearly evident. The reason for not using the book value of the old asset to value the

new asset is that the asset being given up is often carried in the accounting records at historical cost or book value. Neither amount may adequately represent the actual fair

market value of either asset. Therefore, if the fair market value of one asset is clearly

evident, a firm should record this amount for the new asset at the time of the exchange.

Appraised value Sometimes, neither of the items exchanged has a clearly

determinable fair market value. Then, accountants record exchanges of items at their

appraised values as determined by a professional appraiser. An appraised value is an

expert's opinion of an item's fair market price if the item were sold. Appraisals are used

often to value works of art, rare books, and antiques.

Book value The book value of an asset is its recorded cost less accumulated

depreciation. An old asset's book value is usually not a valid indication of the new

asset's fair market value. If a better basis is not available, however, a firm could use the

book value of the old asset.

Occasionally, a company receives an asset without giving up anything for it. For

example, to attract industry to an area and provide jobs for local residents, a city may

give a company a tract of land on which to build a factory. Although such a gift costs

the recipient company nothing, it usually records the asset (Land) at its fair market

value. Accountants record gifts of plant assets at fair market value to provide

information on all assets owned by the company. Omitting some assets may make

information provided misleading. They would credit assets received as gifts to a

stockholders' equity account titled Paid-in Capital—Donations.