Reading:Lesson 5 - Understanding the learning objectives

A single proprietorship is an unincorporated business owned by an individual and often managed by that individual.

A partnership is an unincorporated business owned by two or more persons associated as partners and is often managed by them.

A corporation is a business incorporated under the laws of a state and owned by a few stockholders or by thousands of stockholders.

Service companies perform services for a fee.

Merchandising companies purchase goods that are ready for sale and then sell them to

customers.

Manufacturing companies buy materials, convert them into products, and then sell the products to other companies or to final customers.

The income statement reports the revenues and expenses of a company and shows the profitability of that business organization for a stated period of time.

The statement of retained earnings shows the change in retained earnings between the beginning of the period (e.g. a month) and its end.

The balance sheet lists the assets, liabilities, and stockholders’ equity (including dollar amounts) of a business organization at a specific moment in time.

The statement of cash flows shows the cash inflows and cash outflows for a company for a stated period of time.

The accounting equation is Assets = Liabilities + Stockholders’ equity.

The left side of the equation represents the left side of the balance sheet and shows things of

value owned by the business.

The right side of the equation represents the right side of the balance sheet and shows who provided the funds to acquire the things of value (assets).

Some transactions affect only balance sheet items: assets (such as cash, accounts receivable, and equipment), liabilities (such as accounts payable and notes payable), and stockholders’ equity (capital stock). Other transactions affect both balance sheet items and income statement items (revenues, expenses, and eventually retained earnings).

Exhibit 3 (Part A) and Exhibit 4 (Part A) show the effects of business transactions on the accounting equation.

The income statement appears in Exhibit 2 (Part A) and Exhibit 4 (Part C).

The statement of retained earnings appears in Exhibit 2 (Part B).

The balance sheet appears in Exhibit 2 (Part C) and Exhibit 4 (Part B).

The equity ratio is the stockholders’ equity divided by total equities (or total assets).

The equity ratio shows the percentage that assets would have to shrink before a company would

become insolvent (liabilities exceed assets).

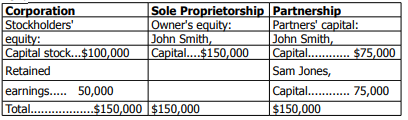

A comparison of corporate accounting with

accounting for a sole proprietorship and a partnership

As you learned in this chapter, the stockholders’ equity section of the balance sheet for a

corporation consists of capital stock and retained earnings. The owner’s equity section of the balance

sheet for a sole proprietorship consists only of the owner’s capital account. The owner’s equity section

of a partnership is similar to that of a single proprietorship except that it shows a capital account and

its balance for each partner.

The stockholders’ equity section of a corporate balance sheet can become more complex as you will

see later in the text. However, the items in the owner’s equity section of the balance sheets of a sole

proprietorship and a partnership always remain as just shown. In a sole proprietorship, the owner’s

capital balance consists of the owner’s investments in the business, plus cumulative net income since

the beginning of the business, less any amounts withdrawn by the owner. Thus, all of the amounts in

the various stockholders’ equity accounts for a corporation are in the owner’s capital account in a single

proprietorship. In a partnership, each partner’s capital account balance consists of that partner’s

investments in the business, plus that partner’s cumulative share of net income since that partner

became a partner, less any amounts withdrawn by that partner.

The Dividends account in a corporation is similar to an owner’s drawing account in a single

proprietorship. These accounts both show amounts taken out of the business by the owners. In a

partnership, each partner has a drawing account. Accountants treat asset, liability, revenue, and

expense accounts similarly in all three forms of organization.