Reading: Lesson 4 - Classes and types of adjusting entries

Adjusting entries fall into two broad classes: deferred (meaning to postpone or delay) items and

accrued (meaning to grow or accumulate) items. Deferred items consist of adjusting entries

involving data previously recorded in accounts. These entries involve the transfer of data already

recorded in asset and liability accounts to expense and revenue accounts, respectively. Accrued items

consist of adjusting entries relating to activity on which no data have been previously recorded in the

accounts. These entries involve the initial, or first, recording of assets and liabilities and the related

revenues and expenses (see Exhibit 16).

Deferred items consist of two types of adjusting entries: asset/expense adjustments and

liability/revenue adjustments. For example, prepaid insurance and prepaid rent are assets until they

are used up; then they become expenses. Also, unearned revenue is a liability until the company

renders the service; then the unearned revenue becomes earned revenue.

Accrued items consist of two types of adjusting entries: asset/revenue adjustments and

liability/expense adjustments. For example, assume a company performs a service for a customer but

has not yet billed the customer. The accountant records this transaction as an asset in the form of a

receivable and as revenue because the company has earned a revenue. Also, assume a company owes its employees salaries not yet paid. The accountant records this transaction as a liability and an

expense because the company has incurred an expense.

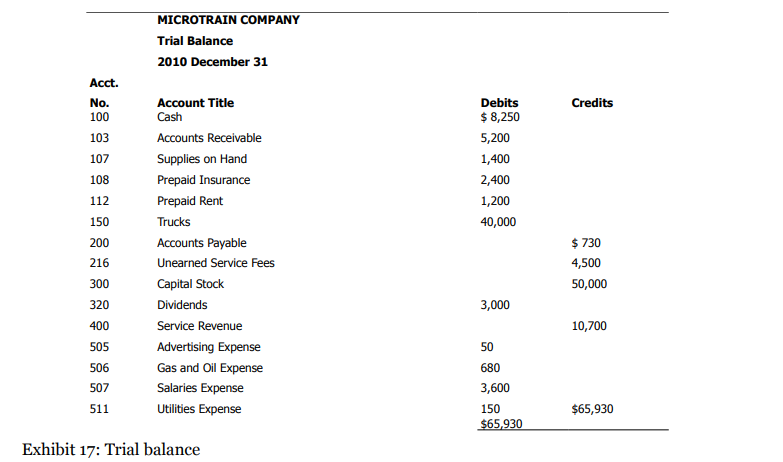

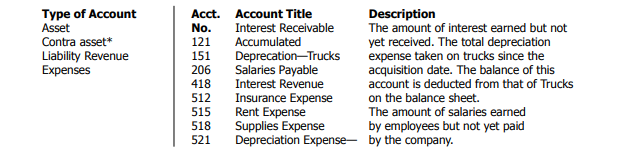

In this chapter, we illustrate each of the four types of adjusting entries: asset/expense, liability/revenue, asset/revenue, and liability/expense. Look at Exhibit 17, the trial balance of the MicroTrain Company at 2010 December 31. As you can see, MicroTrain must adjust several accounts before it can prepare accurate financial statements. The adjustments for these accounts involve data already recorded in the company’s accounts. In making adjustments for MicroTrain Company, we must add several accounts to the company’s chart of accounts shown in Chapter 2. These new accounts are:

Now you are ready to follow as MicroTrain Company makes its adjustments for deferred items. If you find the process confusing, review the beginning of this chapter so you clearly understand the purpose of adjusting entries.