Reading: Lesson 5 - The closing process

In Unit 3, you learned that revenue, expense, and dividends accounts are nominal (temporary)

accounts that are merely subclassifications of a real (permanent) account, Retained Earnings. You also

learned that we prepare financial statements for certain accounting periods. The closing process

transfers (1) the balances in the revenue and expense accounts to a clearing account called Income Summary and then to Retained Earnings and (2) the balance in the Dividends account to the Retained

Earnings account. The closing process reduces revenue, expense, and Dividends account balances to

zero so they are ready to receive data for the next accounting period. Accountants may perform the

closing process monthly or annually.

The Income Summary account is a clearing account used only at the end of an accounting

period to summarize revenues and expenses for the period. After transferring all revenue and expense

account balances to Income Summary, the balance in the Income Summary account represents the net

income or net loss for the period. Closing or transferring the balance in the Income Summary account

to the Retained Earnings account results in a zero balance in Income Summary.

Also closed at the end of the accounting period is the Dividends account containing the dividends

declared by the board of directors to the stockholders. We close the Dividends account directly to the

Retained Earnings account and not to Income Summary because dividends have no effect on income or

loss for the period.

In accounting, we often refer to the process of closing as closing the books. Remember that only

revenue, expense, and Dividend accounts are closed—not asset, liability, Capital Stock, or Retained

Earnings accounts. The four basic steps in the closing process are:

- Closing the revenue accounts—transferring the balances in the revenue accounts to a

clearing account called Income Summary.

- Closing the expense accounts—transferring the balances in the expense accounts to a

clearing account called Income Summary.

- Closing the Income Summary account—transferring the balance of the Income Summary

account to the Retained Earnings account.

- Closing the Dividends account—transferring the balance of the Dividends account to the

Retained Earnings account.

Revenues appear in the Income Statement credit column of the work sheet. The two revenue

accounts in the Income Statement credit column for MicroTrain Company are service revenue of USD

13,200 and interest revenue of USD 600 (Exhibit 20). Because revenue accounts have credit balances,

you must debit them for an amount equal to their balance to bring them to a zero balance. When you

debit Service Revenue and Interest Revenue, credit Income Summary (Account No. 600). Enter the

account numbers in the Posting Reference column when the journal entry has been posted to the

ledger. Do this for all other closing journal entries.

After the closing entries have been posted, the Service Revenue and Interest Revenue accounts (in

T-account format) of MicroTrain appear as follows. Note that the accounts now have zero balances.

As a result of the previous entry, you would credit the Income Summary account for USD 13,800.

We show the Income Summary account in Step 3.

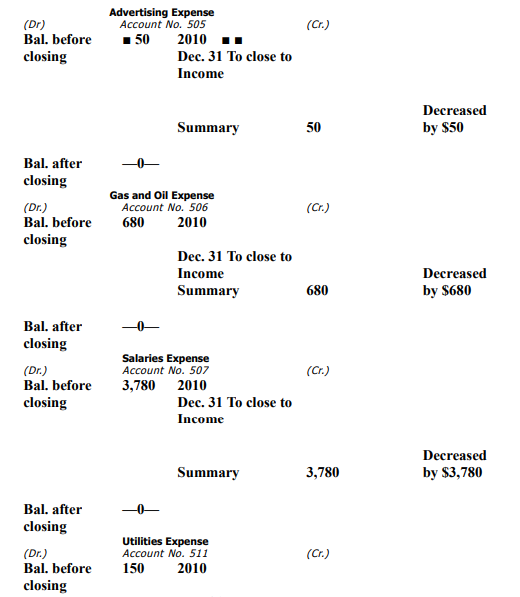

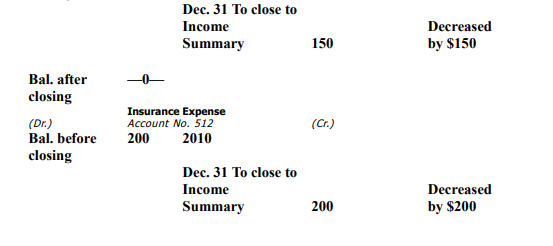

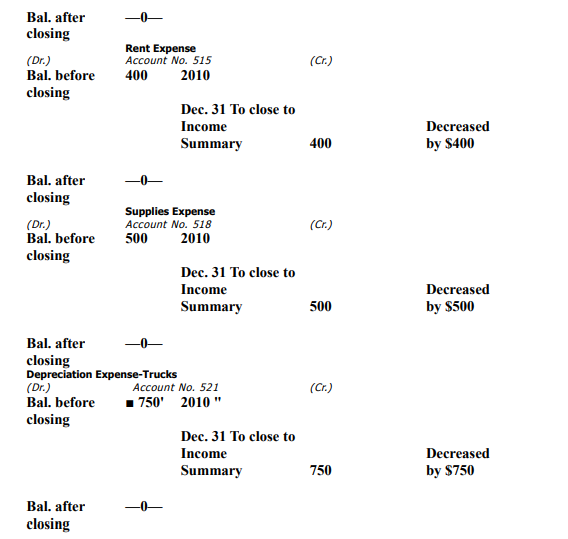

Expenses appear in the Income Statement debit column of the work sheet. MicroTrain Company

has eight expenses in the Income Statement debit column. As shown by the column subtotal, these

expenses add up to USD 6,510. Since expense accounts have debit balances, credit each account to

bring it to a zero balance. Then, make the debit in the closing entry to the Income Summary account

for USD 6,510. Thus, to close the expense accounts, MicroTrain makes the following entry:

The debit of USD 6,510 to the Income Summary account agrees with the Income Statement debit

column subtotal in the work sheet. This comparison with the work sheet serves as a check that all

revenue and expense items have been listed and closed. If the debit in the preceding entry was made

for a different amount than the column subtotal, the company would have an error in the closing entry

for expenses.

After they have been closed, MicroTrain's expense accounts appear as follows. Note that each

account has a zero balance after closing.

The expense accounts could be closed before the revenue accounts; the end result is the same.

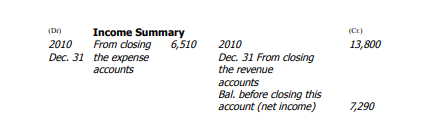

As the result of closing the revenues and expenses of MicroTrain, the total revenues and expenses

have been transferred to the Income Summary account.

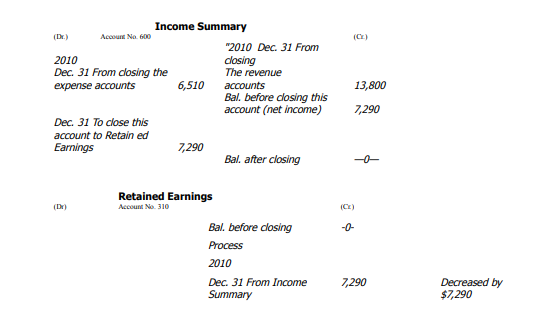

MicroTrain's Income Summary account now has a credit balance of USD 7,290, the company's net

income for December.

Next, close MicroTrain's Income Summary account to its Retained Earnings account. The journal

entry to do this is:

After its Income Summary account is closed, the company's Income Summary and Retained

Earnings accounts appear as follows:

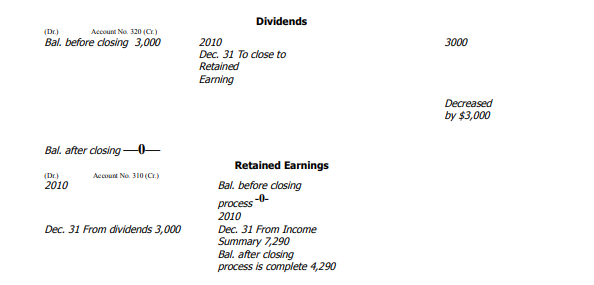

The last closing entry closes MicroTrain's Dividends account. This account has a debit balance

before closing. To close the account, credit the Dividends account and debit the Retained Earnings

account. The Dividends account is not closed to the Income Summary because it is not an expense and does not enter into income determination. The journal entry to close MicroTrain's Dividends account

is:

After this closing entry is posted, the company's Dividends and Retained Earnings accounts appear

as follows:

After you have completed the closing process, the only accounts in the general ledger that have not

been closed are the permanent balance sheet accounts. Because these accounts contain the opening

balances for the coming accounting period, debit balance totals must equal credit balance totals. The

preparation of a post-closing trial balance serves as a check on the accuracy of the closing process and

ensures that the books are in balance at the start of the new accounting period. The post-closing trial

balance differs from the adjusted trial balance in only two important respects: (1) it excludes all

temporary accounts since they have been closed; and (2) it updates the Retained Earnings account to

its proper ending balance.

A post-closing trial balance is a trial balance taken after the closing entries have been posted.

The only accounts that should be open are assets, liabilities, capital stock, and Retained Earnings

accounts. List all the account balances in the debit and credit columns and total them to make sure

debits and credits are equal.

Look at Exhibit 24, a post-closing trial balance for MicroTrain Company as of 2010 December 31.

The amounts in the post-closing trial balance are from the ledger after the closing entries have been

posted.

The next section briefly describes the evolution of accounting systems from the one-journal, oneledger manual system you have been studying to computerized systems. Then, we discuss the role of an accounting system.