Reading: Lesson 4 - The major principles

Generally accepted accounting principles (GAAP) set forth standards or methods for presenting financial accounting information. A standardized presentation format enables users to compare the financial information of different companies more easily. Generally accepted accounting principles have been either developed through accounting practice or established by authoritative organizations. Organizations that have contributed to the development of the principles are the American Institute of Certified Public Accountants (AICPA), the Financial Accounting Standards Board (FASB), the Securities and Exchange Commission (SEC), the American Accounting Association (AAA), the Financial Executives Institute (FEI), and the Institute of Management Accounting (IMA). This section explains the following major principles:

- Exchange-price (or cost) principle.

- Revenue recognition principle.

- Matching principle.

- Gain and loss recognition principle.

- Full disclosure principle.

Whenever resources are transferred between two parties, such as buying merchandise on account,

the accountant must follow the exchange-price (or cost) principle in presenting that information. The

exchange-price (or cost) principle requires an accountant to record transfers of resources at

prices agreed on by the parties to the exchange at the time of exchange. This principle sets forth (1)

what goes into the accounting system—transaction data; (2) when it is recorded—at the time of

exchange; and (3) the amounts—exchange prices—at which assets, liabilities, stockholders' equity,

revenues, and expenses are recorded.

As applied to most assets, this principle is often called the cost principle. It dictates that

purchased or self-constructed assets are initially recorded at historical cost. Historical cost is the

amount paid, or the fair market value of the liability incurred or other resources surrendered, to

acquire an asset and place it in a condition and position for its intended use. For instance, when the

cost of a plant asset (such as a machine) is recorded, its cost includes the net purchase price plus any

costs of reconditioning, testing, transporting, and placing the asset in the location for its intended use.

Accountants prefer the term exchange-price principle to cost principle because it seems inappropriate

to refer to liabilities, stockholders' equity, and such assets as cash and accounts receivable as being

measured in terms of cost.

More recently, the FASB in SFAS 157 has moved definitively towards fair market value accounting,

or “mark-to-market”, which records the value of an asset or liability at its current market value (also

known as a “fair value”) rather than its book value.

SFAS 157 defines “fair value” as “the price that would be received to sell an asset or paid to transfer

a liability in an orderly transaction between market participants at the measurement date”. It is also defined as “an exit price from the perspective of a market participant that holds the asset

or owes the liability”, whether or not the business plans to hold the asset/liability for investment, or

sell it.

“The fair value accounting standard SFAS 157 applies to financial assets of all publicly-traded

companies in the US as of 2007 Nov. 15. It also applies to non-financial assets and liabilities that are

recognized, or disclosed, at fair value on a recurring basis. Beginning in 2009, the standard will apply

to other non-financial assets. SFAS 157 applies to items for which other accounting pronouncements

require or permit fair value measurements except share-based payment transactions, such as stock

option compensation.

“SFAS 157 provides a hierarchy of three levels of input data for determining the fair value of an

asset or liability. This hierarchy ranks the quality and reliability of information used to determine fair

values, with level 1 inputs being the most reliable and level 3 inputs being the least reliable.

- Level 1 is quoted prices for identical items in active, liquid and visible markets such as stock

exchanges.

- Level 2 is observable information for similar items in active or inactive markets, such as two similarly situated buildings in a downtown real estate market.

- Level 3 are unobservable inputs to be used in situations where markets do not exist or are

illiquid such as the present credit crisis. At this point fair market valuation becomes highly

subjective.”

Fair value accounting has been a contentious topic since it was introduced, For example, “banks and

investment banks have had to reduce the value of the mortgages and mortgage-backed securities to

reflect current prices”. Those prices declined severely with the collapse of credit markets as mortgage

defaults escalated in the financial crisis of 2008-2009. Despite debate over the proper implementation

of fair market value accounting, International Financial Reporting Standards utilize this approach

much more than the Generally Accepted Accounting Principles of the United States.

Revenue is not difficult to define or measure; it is the inflow of assets from the sale of goods and

services to customers, measured by the cash expected to be received from customers. However, the

crucial question for the accountant is when to record a revenue. Under the revenue recognition

principle, revenues should be earned and realized before they are recognized (recorded).

Earning of revenue All economic activities undertaken by a company to create revenues are part

of the earning process. Many activities may have preceded the actual receipt of cash from a customer,

including (1) placing advertisements, (2) calling on the customer several times, (3) submitting samples,

(4) acquiring or manufacturing goods, and (5) selling and delivering goods. For these activities, the

company incurs costs. Although revenue was actually being earned by these activities, accountants do

not recognize revenue until the time of sale because of the requirement that revenue be substantially

earned before it is recognized (recorded). This requirement is the earning principle.

Realization of revenue Under the realization principle, the accountant does not recognize

(record) revenue until the seller acquires the right to receive payment from the buyer. The seller

acquires this right from the buyer at the time of sale for merchandise transactions or when services

have been performed in service transactions. Legally, a sale of merchandise occurs when title to the

goods passes to the buyer. The time at which title passes normally depends on the shipping terms—

FOB shipping point or FOB destination (as we discuss in Chapter 6). As a practical matter, accountants

generally record revenue when goods are delivered.

The advantages of recognizing revenue at the time of sale are (1) the actual transaction—delivery of

goods—is an observable event; (2) revenue is easily measured; (3) risk of loss due to price decline or

destruction of the goods has passed to the buyer; (4) revenue has been earned, or substantially so; and

(5) because the revenue has been earned, expenses and net income can be determined. As discussed

later, the disadvantage of recognizing revenue at the time of sale is that the revenue might not be

recorded in the period during which most of the activity creating it occurred.

Exceptions to the realization principle The following examples are instances when practical

considerations may cause accountants to vary the point of revenue recognition from the time of sale.

These examples illustrate the effect that the business environment has on the development of

accounting principles and standards.

Cash collection as point of revenue recognition Some small companies record revenues and

expenses at the time of cash collection and payment, which may not occur at the time of sale. This

procedure is the cash basis of accounting. The cash basis is acceptable primarily in service enterprises

that do not have substantial credit transactions or inventories, such as business entities of doctors or

dentists.

Installment basis of revenue recognition When collecting the selling price of goods sold in

monthly or annual installments and considerable doubt exists as to collectibility, the company may use

the installment basis of accounting. Companies make these sales in spite of the doubtful collectibility of

the account because their margin of profit is high and the goods can be repossessed if the payments are

not received. Under the installment basis, the percentage of total gross margin (selling price of a

good minus its cost) recognized in a period is equal to the percentage of total cash from a sale that is

received in that period. Thus, the gross margin recognized in a period is equal to the cash received

times the gross margin percentage (gross margin divided by selling price). The formula to recognize

gross profit on cash collections made on installment sales of a certain year is:

Cash collections x Grossmargin percentage=Gross margin recognized

To be more precise, we expand the descriptions in the formula as follows:

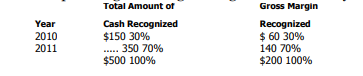

To illustrate, assume a company sold a stereo set. The facts of the sale are:

The buyer makes 10 equal monthly installment payments of USD 50 to pay for the set (10 X USD 50

= USD 500). If the company receives three monthly payments in 2010, the total amount of cash

received in 2010 is USD 150 (3 X USD 50). The gross margin to recognize in 2010 is:

The company collects the other installments when due so it receives a total of USD 350 in 2011 from

2010 installment sales. The gross margin to recognize in 2011 on these cash collections is as follows:

In summary, the total receipts and gross margin recognized in the two years are as follows:

Because the installment basis delays some revenue recognition beyond the time of sale, it is

acceptable for accounting purposes only when considerable doubt exists as to collectibility of the

installments.

Revenue recognition on long-term construction projects Companies recognize revenue

from a long-term construction project under two different methods: (1) the completed-contract method

or (2) the percentage-of-completion method. The completed-contract method does not recognize

any revenue until the project is completed. In that period, they recognize all revenue even though the

contract may have required three years to complete. Thus, the completed-contract method recognizes

revenues at the time of sale, as is true for most sales transactions. Companies carry costs incurred on

the project forward in an inventory account (Construction in Process) and charge them to expense in

the period in which the revenue is recognized.

Some accountants argue that waiting so long to recognize any revenue is unreasonable. They believe

that because revenue-producing activities have been performed during each year of construction,

revenue should be recognized in each year of construction even if estimates are needed. The

percentage-of-completion method recognizes revenue based on the estimated stage of completion

of a long-term project. To measure the stage of completion, firms compare actual costs incurred in a

period with the total estimated costs to be incurred on the project.

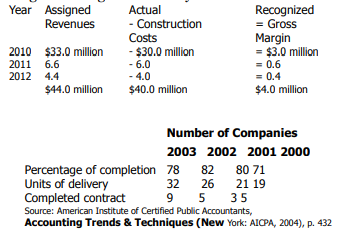

To illustrate, assume that a company has a contract to build a dam for USD 44 million. The

estimated construction cost is USD 40 million. You calculate the estimated gross margin as follows:

The firm recognizes the USD 4 million gross margin in the financial statements by recording the assigned revenue for the year and then deducting actual costs incurred that year. The formula to recognize revenue is:

![]()

Suppose that by the end of the first year (2010), the company had incurred actual construction costs

of USD 30 million. These costs are 75 per cent of the total estimated construction costs (USD 30

million/USD 40 million = 75 per cent). Under the percentage-of-completion method, the firm would

use the 75 per cent figure to assign revenue to the first year. In 2011, it incurs another USD 6 million of

construction costs. In 2012, it incurs the final USD 4 million of construction costs. The amount of

revenue to assign to each year is as follows:

The amount of gross margin to recognize in each year is as follows:

This company would deduct other costs incurred in the accounting period, such as general and

administrative expenses, from gross margin to determine net income. For instance, assuming general

and administrative expenses were USD 100,000 in 2010, net income would be (USD 3,000,000 - USD

100,000) = USD 2,900,000.

Expense recognition is closely related to, and sometimes discussed as part of, the revenue

recognition principle. The matching principle states that expenses should be recognized (recorded)

as they are incurred to produce revenues. An expense is the outflow or using up of assets in the

generation of revenue. Firms voluntarily incur expense to produce revenue. For instance, a television

set delivered by a dealer to a customer in exchange for cash is an asset consumed to produce revenue;

its cost becomes an expense. Similarly, the cost of services such as labor are voluntarily incurred to

produce revenue.

The measurement of expense Accountants measure most assets used in operating a business

by their historical costs. Therefore, they measure a depreciation expense resulting from the

consumption of those assets by the historical costs of those assets. They measure other expenses, such

as wages that are paid for currently, at their current costs.

The timing of expense recognition The matching principle implies that a relationship exists

between expenses and revenues. For certain expenses, such as costs of acquiring or producing the

products sold, you can easily see this relationship. However, when a direct relationship cannot be seen,

we charge the costs of assets with limited lives to expense in the periods benefited on a systematic and

rational allocation basis. Depreciation of plant assets is an example.

Product costs are costs incurred in the acquisition or manufacture of goods. As you will see in the

next chapter, included as product costs for purchased goods are invoice, freight, and insurance-intransit

costs. For manufacturing companies, product costs include all costs of materials, labor, and

factory operations necessary to produce the goods. Product costs attach to the goods purchased or

produced and remain in inventory accounts as long as the goods are on hand. We charge product costs

to expense when the goods are sold. The result is a precise matching of cost of goods sold expense to its

related revenue.

Period costs are costs not traceable to specific products and expensed in the period incurred.

Selling and administrative costs are period costs.

The gain and loss recognition principle states that we record gains only when realized, but

losses when they first become evident. Thus, we recognize losses at an earlier point than gains. This

principle is related to the conservatism concept.

Gains typically result from the sale of long-term assets for more than their book value. Firms

should not recognize gains until they are realized through sale or exchange. Recognizing potential

gains before they are actually realized is not allowed.

Losses consume assets, as do expenses. However, unlike expenses, they do not produce revenues.

Losses are usually involuntary, such as the loss suffered from destruction by fire on an uninsured building. A loss on the sale of a building may be voluntary when management decides to sell the

building even though incurring a loss.

The full disclosure principle states that information important enough to influence the decisions of an informed user of the financial statements should be disclosed. Depending on its nature, companies should disclose this information either in the financial statements, in notes to the financial statements, or in supplemental statements. In judging whether or not to disclose information, it is better to err on the side of too much disclosure rather than too little. Many lawsuits against CPAs and their clients have resulted from inadequate or misleading disclosure of the underlying facts.