Reading: Lesson 5 - Modifying conventions

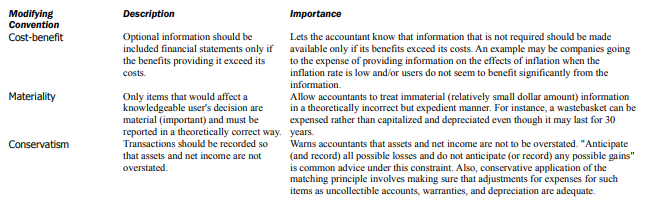

In certain instances, companies do not strictly apply accounting principles because of modifying

conventions (or constraints). Modifying conventions are customs emerging from accounting

practice that alter the results obtained from a strict application of accounting principles. Three

modifying conventions are cost-benefit, materiality, and conservatism.

Cost-benefit The cost-benefit consideration involves deciding whether the benefits of including

optional information in financial statements exceed the costs of providing the information. Users tend

to think information is cost free since they incur none of the costs of providing the information.

Preparers realize that providing information is costly. The benefits of using information should exceed

the costs of providing it. The measurement of benefits is inexact, which makes application of this

modifying convention difficult in practice.

Materiality Materiality is a modifying convention that allows accountants to deal with immaterial

(unimportant) items in an expedient but theoretically incorrect manner. The fundamental question

accountants must ask in judging the materiality of an item is whether a knowledgeable user's decisions

would be different if the information were presented in the theoretically correct manner. If not, the item is immaterial and may be reported in a theoretically incorrect but expedient manner. For

instance, because inexpensive items such as calculators often do not make a difference in a statement

user's decision to invest in the company, they are immaterial (unimportant) and may be expensed

when purchased. However, because expensive items such as mainframe computers usually do make a

difference in such a decision, they are material (important) and should be recorded as assets and

depreciated. Accountants should record all material items in a theoretically correct manner. They may

record immaterial items in a theoretically incorrect manner simply because it is more convenient and

less expensive to do so. For example, they may debit the cost of a wastebasket to an expense account

rather than an asset account even though the wastebasket has an expected useful life of 30 years. It

simply is not worth the cost of recording depreciation expense on such a small item over its life.

The FASB defines materiality as "the magnitude of an omission or misstatement of accounting

information that, in the light of surrounding circumstances, makes it probable that the judgment of a

reasonable person relying on the information would have been changed or influenced by the omission

or misstatement".3

The term magnitude in this definition suggests that the materiality of an item may

be assessed by looking at its relative size. A USD 10,000 error in an expense in a company with

earnings of USD 30,000 is material. The same error in a company earning USD 30,000,000 may not

be material.

Materiality involves more than the relative dollar amounts. Often the nature of the item makes it

material. For example, it may be quite significant to know that a company is paying bribes or making

illegal political contributions, even if the dollar amounts of such items are relatively small.

Conservatism Conservatism means being cautious or prudent and making sure that assets and

net income are not overstated. Such overstatements can mislead potential investors in the company

and creditors making loans to the company. We apply conservatism when the lower-of-cost-or-market

rule is used for inventory. Accountants must realize a fine line exists between

conservative and incorrect accounting.

The next section of this Unit discusses the conceptual framework project of the Financial Accounting Standards Board. The FASB designed the conceptual framework project to resolve some disagreements about the proper theoretical foundation for accounting. We present only the portions of the project relevant to this text.