Reading: You Need an Innovation Strategy

You Need an Innovation Strategy

By Gary P. Pisano

https://hbr.org/2015/06/you-need-an-innovation-strategy

Despite massive investments of management time and money, innovation remains a frustrating pursuit in many companies. Innovation initiatives frequently fail, and successful innovators have a hard time sustaining their performance—as Polaroid, Nokia, Sun Microsystems, Yahoo, Hewlett-Packard, and countless others have found. Why is it so hard to build and maintain the capacity to innovate? The reasons go much deeper than the commonly cited cause: a failure to execute. The problem with innovation improvement efforts is rooted in the lack of an innovation strategy.

A strategy is nothing more than a commitment to a set of coherent, mutually reinforcing policies or behaviors aimed at achieving a specific competitive goal. Good strategies promote alignment among diverse groups within an organization, clarify objectives and priorities, and help focus efforts around them. Companies regularly define their overall business strategy (their scope and positioning) and specify how various functions—such as marketing, operations, finance, and R&D—will support it. But during my more than two decades studying and consulting for companies in a broad range of industries, I have found that firms rarely articulate strategies to align their innovation efforts with their business strategies.

Without an innovation strategy, innovation improvement efforts can easily become a grab bag of much-touted best practices: dividing R&D into decentralized autonomous teams, spawning internal entrepreneurial ventures, setting up corporate venture-capital arms, pursuing external alliances, embracing open innovation and crowdsourcing, collaborating with customers, and implementing rapid prototyping, to name just a few. There is nothing wrong with any of those practices per se. The problem is that an organization’s capacity for innovation stems from an innovation system: a coherent set of interdependent processes and structures that dictates how the company searches for novel problems and solutions, synthesizes ideas into a business concept and product designs, and selects which projects get funded. Individual best practices involve trade-offs. And adopting a specific practice generally requires a host of complementary changes to the rest of the organization’s innovation system. A company without an innovation strategy won’t be able to make trade-off decisions and choose all the elements of the innovation system.

Aping someone else’s system is not the answer. There is no one system that fits all companies equally well or works under all circumstances. There is nothing wrong, of course, with learning from others, but it is a mistake to believe that what works for, say, Apple (today’s favorite innovator) is going to work for your organization. An explicit innovation strategy helps you design a system to match your specific competitive needs.

Finally, without an innovation strategy, different parts of an organization can easily wind up pursuing conflicting priorities—even if there’s a clear business strategy. Sales representatives hear daily about the pressing needs of the biggest customers. Marketing may see opportunities to leverage the brand through complementary products or to expand market share through new distribution channels. Business unit heads are focused on their target markets and their particular P&L pressures. R&D scientists and engineers tend to see opportunities in new technologies. Diverse perspectives are critical to successful innovation. But without a strategy to integrate and align those perspectives around common priorities, the power of diversity is blunted or, worse, becomes self-defeating.

Despite massive investments of management time and money, innovation remains a frustrating pursuit in many companies. Innovation initiatives frequently fail, and successful innovators have a hard time sustaining their performance—as Polaroid, Nokia, Sun Microsystems, Yahoo, Hewlett-Packard, and countless others have found. Why is it so hard to build and maintain the capacity to innovate? The reasons go much deeper than the commonly cited cause: a failure to execute. The problem with innovation improvement efforts is rooted in the lack of an innovation strategy.

A strategy is nothing more than a commitment to a set of coherent, mutually reinforcing policies or behaviors aimed at achieving a specific competitive goal. Good strategies promote alignment among diverse groups within an organization, clarify objectives and priorities, and help focus efforts around them. Companies regularly define their overall business strategy (their scope and positioning) and specify how various functions—such as marketing, operations, finance, and R&D—will support it. But during my more than two decades studying and consulting for companies in a broad range of industries, I have found that firms rarely articulate strategies to align their innovation efforts with their business strategies.

Without an innovation strategy, innovation improvement efforts can easily become a grab bag of much-touted best practices: dividing R&D into decentralized autonomous teams, spawning internal entrepreneurial ventures, setting up corporate venture-capital arms, pursuing external alliances, embracing open innovation and crowdsourcing, collaborating with customers, and implementing rapid prototyping, to name just a few. There is nothing wrong with any of those practices per se. The problem is that an organization’s capacity for innovation stems from an innovation system: a coherent set of interdependent processes and structures that dictates how the company searches for novel problems and solutions, synthesizes ideas into a business concept and product designs, and selects which projects get funded. Individual best practices involve trade-offs. And adopting a specific practice generally requires a host of complementary changes to the rest of the organization’s innovation system. A company without an innovation strategy won’t be able to make trade-off decisions and choose all the elements of the innovation system.

Aping someone else’s system is not the answer. There is no one system that fits all companies equally well or works under all circumstances. There is nothing wrong, of course, with learning from others, but it is a mistake to believe that what works for, say, Apple (today’s favorite innovator) is going to work for your organization. An explicit innovation strategy helps you design a system to match your specific competitive needs.

Finally, without an innovation strategy, different parts of an organization can easily wind up pursuing conflicting priorities—even if there’s a clear business strategy. Sales representatives hear daily about the pressing needs of the biggest customers. Marketing may see opportunities to leverage the brand through complementary products or to expand market share through new distribution channels. Business unit heads are focused on their target markets and their particular P&L pressures. R&D scientists and engineers tend to see opportunities in new technologies. Diverse perspectives are critical to successful innovation. But without a strategy to integrate and align those perspectives around common priorities, the power of diversity is blunted or, worse, becomes self-defeating.

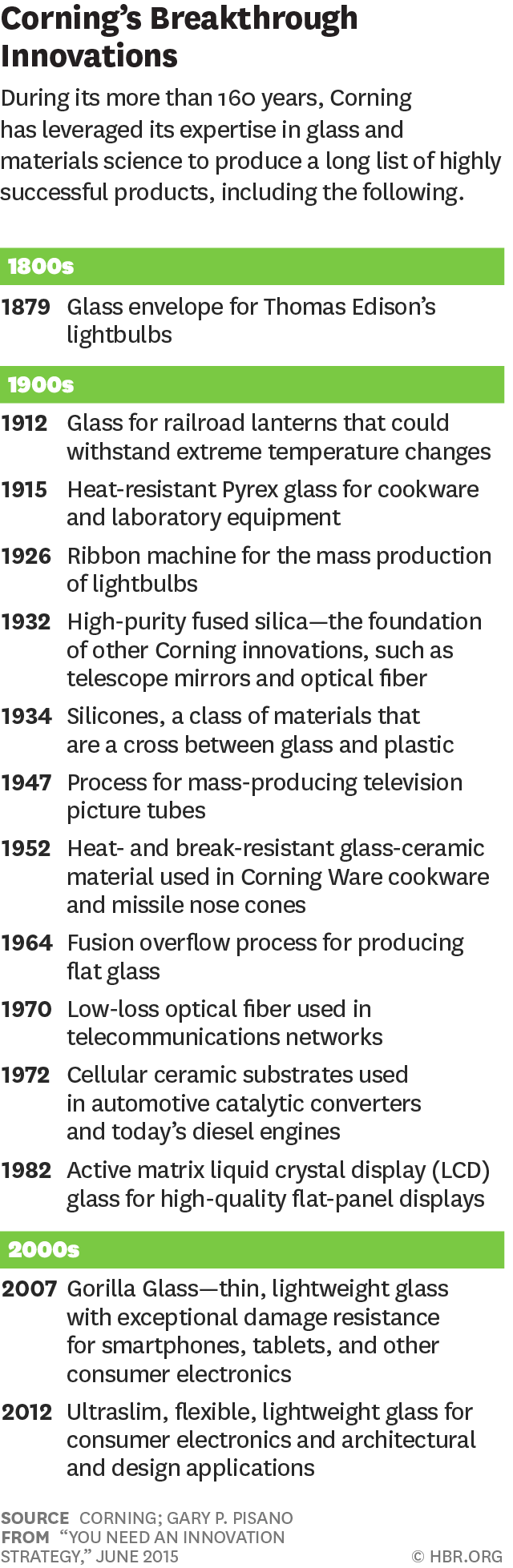

A good example of how a tight connection between business strategy and innovation can drive long-term innovation leadership is found in Corning, a leading manufacturer of specialty components used in electronic displays, telecommunications systems, environmental products, and life sciences instruments. (Disclosure: I have consulted for Corning, but the information in this article comes from the 2008 HBS case study “Corning: 156 Years of Innovation,” by H. Kent Bowen and Courtney Purrington.) Over its more than 160 years Corning has repeatedly transformed its business and grown new markets through breakthrough innovations. When judged against current best practices, Corning’s approach seems out of date. The company is one of the few with a centralized R&D laboratory (Sullivan Park, in rural upstate New York). It invests a lot in basic research, a practice that many companies gave up long ago. And it invests heavily in manufacturing technology and plants and continues to maintain a significant manufacturing footprint in the United States, bucking the trend of wholesale outsourcing and offshoring of production.

Yet when viewed through a strategic lens, Corning’s approach to innovation makes perfect sense. The company’s business strategy focuses on selling “keystone components” that significantly improve the performance of customers’ complex system products. Executing this strategy requires Corning to be at the leading edge of glass and materials science so that it can solve exceptionally challenging problems for customers and discover new applications for its technologies. That requires heavy investments in long-term research. By centralizing R&D, Corning ensures that researchers from the diverse disciplinary backgrounds underlying its core technologies can collaborate. Sullivan Park has become a repository of accumulated expertise in the application of materials science to industrial problems. Because novel materials often require complementary process innovations, heavy investments in manufacturing and technology are a must. And by keeping a domestic manufacturing footprint, the company is able to smooth the transfer of new technologies from R&D to manufacturing and scale up production.

Corning’s strategy is not for everyone. Long-term investments in research are risky: The telecommunications bust in the late 1990s devastated Corning’s optical fiber business. But Corning shows the importance of a clearly articulated innovation strategy—one that’s closely linked to a company’s business strategy and core value proposition. Without such a strategy, most initiatives aimed at boosting a firm’s capacity to innovate are doomed to fail.

Connecting Innovation to Strategy

Connecting Innovation to Strategy

About 10 years ago Bristol-Myers Squibb (BMS), as part of a broad strategic repositioning, decided to emphasize cancer as a key part of its pharmaceutical business. Recognizing that biotechnology-derived drugs such as monoclonal antibodies were likely to be a fruitful approach to combating cancer, BMS decided to shift its repertoire of technological capabilities from its traditional organic-chemistry base toward biotechnology. The new business strategy (emphasizing the cancer market) required a new innovation strategy (shifting technological capabilities toward biologics). (I have consulted for BMS, but the information in this example comes from public sources.)

Like the creation of any good strategy, the process of developing an innovation strategy should start with a clear understanding and articulation of specific objectives related to helping the company achieve a sustainable competitive advantage. This requires going beyond all-too-common generalities, such as “We must innovate to grow,” “We innovate to create value,” or “We need to innovate to stay ahead of competitors.” Those are not strategies. They provide no sense of the types of innovation that might matter (and those that won’t). Rather, a robust innovation strategy should answer the following questions:

How will innovation create value for potential customers?

Unless innovation induces potential customers to pay more, saves them money, or provides some larger societal benefit like improved health or cleaner water, it is not creating value. Of course, innovation can create value in many ways. It might make a product perform better or make it easier or more convenient to use, more reliable, more durable, cheaper, and so on. Choosing what kind of value your innovation will create and then sticking to that is critical, because the capabilities required for each are quite different and take time to accumulate. For instance, Bell Labs created many diverse breakthrough innovations over a half century: the telephone exchange switcher, the photovoltaic cell, the transistor, satellite communications, the laser, mobile telephony, and the operating system Unix, to name just a few. But research at Bell Labs was guided by the strategy of improving and developing the capabilities and reliability of the phone network. The solid-state research program—which ultimately led to the invention of the transistor—was motivated by the need to lay the scientific foundation for developing newer, more reliable components for the communications system. Research on satellite communications was motivated in part by the limited bandwidth and the reliability risks of undersea cables. Apple consistently focuses its innovation efforts on making its products easier to use than competitors’ and providing a seamless experience across its expanding family of devices and services. Hence its emphasis on integrated hardware-software development, proprietary operating systems, and design makes total sense.

How will the company capture a share of the value its innovations generate?

Value-creating innovations attract imitators as quickly as they attract customers. Rarely is intellectual property alone sufficient to block these rivals. Consider how many tablet computers appeared after the success of Apple’s iPad. As imitators enter the market, they create price pressures that can reduce the value that the original innovator captures. Moreover, if the suppliers, distributors, and other companies required to deliver an innovation are dominant enough, they may have sufficient bargaining power to capture most of the value from an innovation. Think about how most personal computer manufacturers were largely at the mercy of Intel and Microsoft.

Companies must think through what complementary assets, capabilities, products, or services could prevent customers from defecting to rivals and keep their own position in the ecosystem strong. Apple designs complementarities between its devices and services so that an iPhone owner finds it attractive to use an iPad rather than a rival’s tablet. And by controlling the operating system, Apple makes itself an indispensable player in the digital ecosystem. Corning’s customer-partnering strategy helps defend the company’s innovations against imitators: Once the keystone components are designed into a customer’s system, the customer will incur switching costs if it defects to another supplier.

One of the best ways to preserve bargaining power in an ecosystem and blunt imitators is to continue to invest in innovation. I recently visited a furniture company in northern Italy that supplies several of the largest retailers in the world from its factories in its home region. Depending on a few global retailers for distribution is risky from a value-capture perspective. Because these megaretailers have access to dozens of other suppliers around the world, many of them in low-cost countries, and because furniture designs are not easily protected through patents, there is no guarantee of continued business. The company has managed to thrive, however, by investing both in new designs, which help it win business early in the product life cycle, and in sophisticated process technologies, which allow it to defend against rivals from low-cost countries as products mature.

What types of innovations will allow the company to create and capture value, and what resources should each type receive?

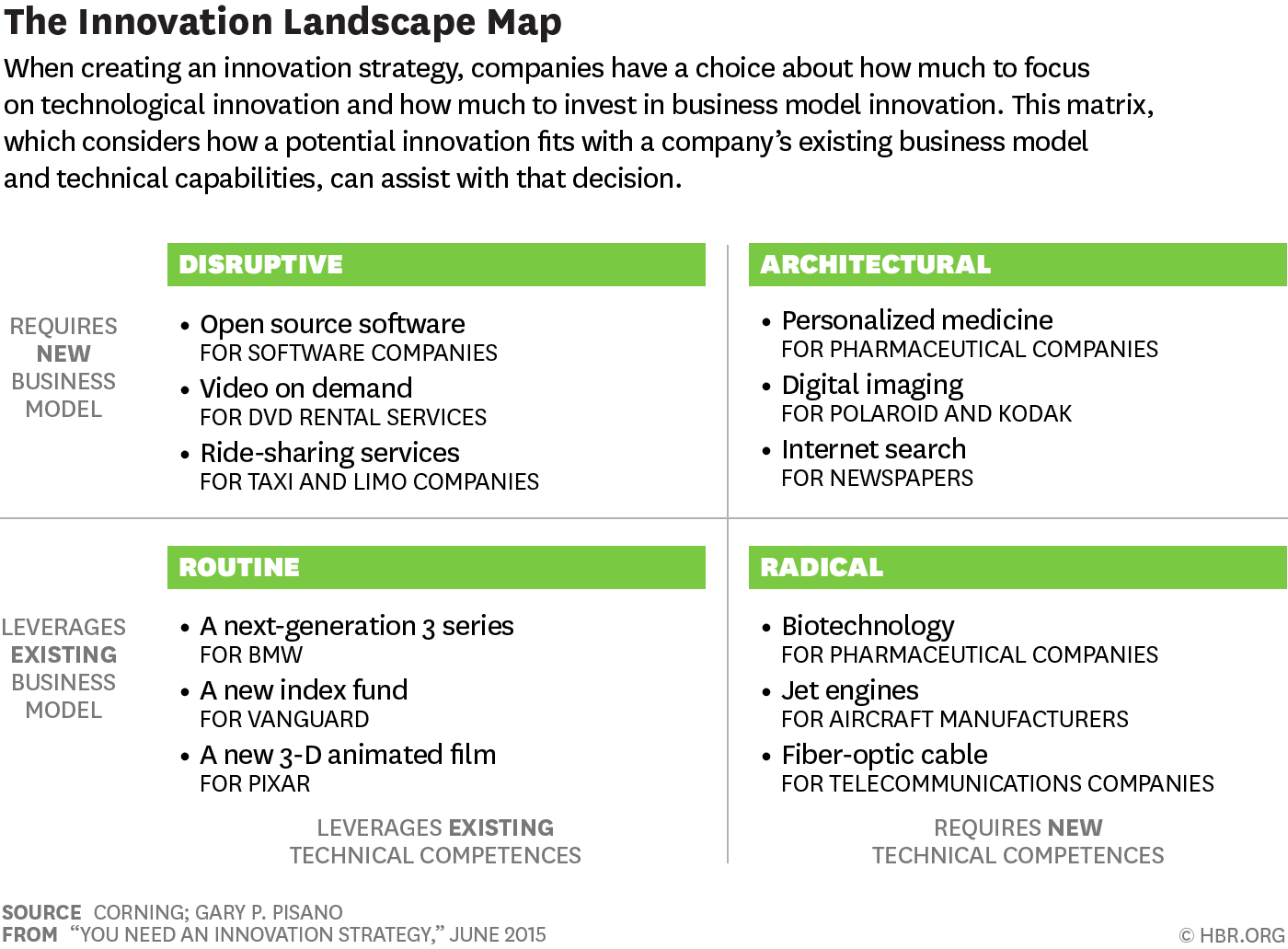

Certainly, technological innovation is a huge creator of economic value and a driver of competitive advantage. But some important innovations may have little to do with new technology. In the past couple of decades, we have seen a plethora of companies (Netflix, Amazon, LinkedIn, Uber) master the art of business model innovation. Thus, in thinking about innovation opportunities, companies have a choice about how much of their efforts to focus on technological innovation and how much to invest in business model innovation.

Routine innovation is often called myopic or suicidal. That thinking is simplistic.

A helpful way to think about this is depicted in the exhibit “The Innovation Landscape Map.” The map, based on my research and that of scholars such as William Abernathy, Kim Clark, Clayton Christensen, Rebecca Henderson, and Michael Tushman, characterizes innovation along two dimensions: the degree to which it involves a change in technology and the degree to which it involves a change in business model. Although each dimension exists on a continuum, together they suggest four quadrants, or categories, of innovation.

Routine innovation builds on a company’s existing technological competences and fits with its existing business model—and hence its customer base. An example is Intel’s launching ever-more-powerful microprocessors, which has allowed the company to maintain high margins and has fueled growth for decades. Other examples include new versions of Microsoft Windows and the Apple iPhone.

Disruptive innovation, a category named by my Harvard Business School colleague Clay Christensen, requires a new business model but not necessarily a technological breakthrough. For that reason, it also challenges, or disrupts, the business models of other companies. For example, Google’s Android operating system for mobile devices potentially disrupts companies like Apple and Microsoft, not because of any large technical difference but because of its business model: Android is given away free; the operating systems of Apple and Microsoft are not.

Radical innovation is the polar opposite of disruptive innovation. The challenge here is purely technological. The emergence of genetic engineering and biotechnology in the 1970s and 1980s as an approach to drug discovery is an example. Established pharmaceutical companies with decades of experience in chemically synthesized drugs faced a major hurdle in building competences in molecular biology. But drugs derived from biotechnology were a good fit with the companies’ business models, which called for heavy investment in R&D, funded by a few high-margin products.

Architectural innovation combines technological and business model disruptions. An example is digital photography. For companies such as Kodak and Polaroid, entering the digital world meant mastering completely new competences in solid-state electronics, camera design, software, and display technology. It also meant finding a way to earn profits from cameras rather than from “disposables” (film, paper, processing chemicals, and services). As one might imagine, architectural innovations are the most challenging for incumbents to pursue.

A company’s innovation strategy should specify how the different types of innovation fit into the business strategy and the resources that should be allocated to each. In much of the writing on innovation today, radical, disruptive, and architectural innovations are viewed as the keys to growth, and routine innovation is denigrated as myopic at best and suicidal at worst. That line of thinking is simplistic.

In fact, the vast majority of profits are created through routine innovation. Since Intel launched its last major disruptive innovation (the i386 chip), in 1985, it has earned more than $200 billion in operating income, most of which has come from next-generation microprocessors. Microsoft is often criticized for milking its existing technologies rather than introducing true disruptions. But this strategy has generated $303 billion in operating income since the introduction of Windows NT, in 1993 (and $258 billion since the introduction of the Xbox, in 2001). Apple’s last major breakthrough (as of this writing), the iPad, was launched in 2010. Since then Apple has launched a steady stream of upgrades to its core platforms (Mac, iPhone, and iPad), generating an eye-popping $190 billion in operating income.

The point here is not that companies should focus solely on routine innovation. Rather, it is that there is not one preferred type. In fact, as the examples above suggest, different kinds of innovation can become complements, rather than substitutes, over time. Intel, Microsoft, and Apple would not have had the opportunity to garner massive profits from routine innovations had they not laid the foundations with various breakthroughs. Conversely, a company that introduces a disruptive innovation and cannot follow up with a stream of improvements will not hold new entrants at bay for long.

Executives often ask me, “What proportion of resources should be directed to each type of innovation?” Unfortunately, there is no magic formula. As with any strategic question, the answer will be company specific and contingent on factors such as the rate of technological change, the magnitude of the technological opportunity, the intensity of competition, the rate of growth in core markets, the degree to which customer needs are being met, and the company’s strengths. Businesses in markets where the core technology is evolving rapidly (like pharmaceuticals, media, and communications) will have to be much more keenly oriented toward radical technological innovation—both its opportunities and its threats. A company whose core business is maturing may have to seek opportunities through business model innovations and radical technological breakthroughs. But a company whose platforms are growing rapidly would certainly want to focus most of its resources on building and extending them.

In thinking strategically about the four types of innovation, then, the question is one of balance and mix. Google is certainly experiencing rapid growth through routine innovations in its advertising business, but it is also exploring opportunities for radical and architectural innovations, such as a driverless car, at its Google X facility. Apple is not resting on its iPhone laurels as it explores wearable devices and payment systems. And while incumbent automobile companies still make the vast majority of their revenue and profits from traditional fuel-powered vehicles, most have introduced alternative-energy vehicles (hybrid and all-electric) and have serious R&D efforts in advanced alternatives like hydrogen-fuel-cell motors.

Overcoming the Prevailing Winds

I liken routine innovation to a sports team’s home-field advantage: It’s where companies play to their strengths. Without an explicit strategy indicating otherwise, a number of organizational forces will tend to drive innovation toward the home field.

Some years ago I worked with a contact lens company whose leaders decided that it needed to focus less on routine innovations, such as adding color tints and modifying lens design, and be more aggressive in pursuing new materials that could dramatically improve visual acuity and comfort. After a few years, however, little progress had been made. A review of the R&D portfolio at a senior management meeting revealed that most of the company’s R&D expenditures were going to incremental refinements of existing products (demanded by marketing to stave off mounting short-term losses in share) and to process improvements (demanded by manufacturing to reduce costs, which was, in turn, demanded by finance to preserve margins as prices fell). Even worse, when R&D finally created a high-performing lens based on a new material, manufacturing could not produce it consistently at high volume, because it had not invested in the requisite capabilities. Despite a strategic intent to venture into new territory, the company was trapped on its home field.

The root of the problem was that business units and functions had continued to make resource allocation decisions, and each favored the projects it saw as the most pressing. Only after senior management created explicit targets for different types of innovations—and allocated a specific percentage of resources to radical innovation projects—did the firm begin to make progress in developing new offerings that supported its long-term strategy. As this company found, innovation strategy matters most when an organization needs to change its prevailing patterns.

Managing Trade-Offs

As I’ve noted, an explicit innovation strategy helps you understand which practices might be a good fit for your organization. It also helps you navigate the inherent trade-offs.

Consider one popular practice: crowdsourcing. The idea is that rather than relying on a few experts (perhaps your own employees) to solve specific innovation problems, you open up the process to anyone (the crowd). One common example is when an organization posts a problem on a web platform (like InnoCentive) and invites solutions, perhaps offering a financial prize. Another example is open source software projects, in which volunteers contribute to developing a product or a system (think of Linux). Crowdsourcing has a lot of merits: By inviting a vast number of people, most of whom you probably could not have found on your own, to address your challenges, you increase the probability of developing a novel solution. Research by my Harvard Business School colleague Karim Lakhani and his collaborator Kevin Boudreau, of the London Business School, provides strong evidence that crowdsourcing can lead to faster, more-efficient, and more-creative problem solving.

But crowdsourcing works better for some kinds of problems than for others. For instance, it requires fast and efficient ways to test a large number of potential solutions. If testing is very time-consuming and costly, you need some other approach, such as soliciting a handful of solutions from just a few experts or organizations. Similarly, crowdsourcing tends to work best for highly modular systems, in which different problem solvers can focus on specific components without worrying about others.

Crowdsourcing is not universally good or bad. It is simply a tool whose strength (exploiting large numbers of diverse problem solvers) is a benefit in some contexts (highly diffused knowledge base, relatively inexpensive ways to test proposed solutions, modular system) but not in others (concentrated knowledge base, expensive testing, system with integral architectures).

Another practice subject to trade-offs is customer involvement in the innovation process. Advocates of “co-creation” approaches argue that close collaboration with customers reveals insights that can lead to novel offerings. (See Venkat Ramaswamy and Francis Gouillart, “Building the Co-Creative Enterprise,” HBR, October 2010.) But others say that working too closely with customers will blind you to opportunities for truly disruptive innovation. Steve Jobs was adamant that customers do not always know what they want—the reason he cited for eschewing market research.

Choosing a side in this debate requires the cold calculus of strategy. Corning’s customer-centered approach to innovation is appropriate for a company whose business strategy is focused on creating critical components of highly innovative systems. It would be virtually impossible to develop such components without tapping customers’ deep understanding of their system. In addition, close collaboration enables Corning and its customers to mutually adapt the component and the system. This is critical when subtle changes in the component technology can affect the system, and vice versa.

But Corning’s demand-pull approach (finding customers’ highly challenging problems and then figuring out how the company’s cutting-edge technologies can solve them) is limited by customers’ imagination and willingness to take risks. It also hinges on picking the right customers; if Corning doesn’t, it can miss a market transformation.

Crowdsourcing, like other innovation practices, involves trade-offs.

A supply-push approach—developing technology and then finding or creating a market—can be more suitable when an identifiable market does not yet exist. A good example is the integrated circuit, invented in the late 1950s by Texas Instruments and Fairchild Semiconductor. Both came up with the idea of putting multiple transistors on a chip as a way to solve a reliability problem, not to spawn smaller computers. In fact, with the exception of the military, there was little demand for integrated circuits. Producers of computers, electronics equipment, and telecommunications systems preferred discrete transistors, which were cheaper and less risky. To help create demand, Texas Instruments invented and commercialized another device: the handheld calculator.

Some pharmaceutical companies, including Novartis (for whom I’ve consulted), explicitly shield their research groups from market input when deciding which programs to pursue. They believe that given the long lead times of drug development and the complexities of the market, accurate forecasts are impossible. (See the 2008 HBS case study “Novartis AG: Science-Based Business,” by H. Kent Bowen and Courtney Purrington.)

Again, the choice between a demand-pull and a supply-push approach involves weighing the trade-offs. If you choose the former, you risk missing out on technologies for which markets have not yet emerged. If you choose the latter, you may create technologies that never find a market.

Similar trade-offs are inherent in choices about innovation processes. For instance, many companies have adopted fairly structured “phase-gate” models for managing their innovation processes. Advocates argue that those models inject a degree of predictability and discipline into what can be a messy endeavor. Opponents counter that they destroy creativity. Who is right? Both are—but for different kinds of projects. Highly structured phase-gate processes, which tend to focus on resolving as much technical and market uncertainty as possible early on, work well for innovations involving a known technology for a known market. But they generally do not allow for the considerable iteration required for combinations of new markets and new technologies. Those uncertain and complex projects require a different kind of process, one that involves rapid prototyping, early experimentation, parallel problem solving, and iteration.

Clarity around which trade-offs are best for the company as a whole—something an innovation strategy provides—is extremely helpful in overcoming the barriers to the kind of organizational change innovation often requires. People don’t resist change because they are inherently stubborn or political but because they have different perspectives—including on how to weigh the trade-offs in innovation practices. Clarity around trade-offs and priorities is a critical first step in mobilizing the organization around an innovation initiative.

The Leadership Challenge

Creating a capacity to innovate starts with strategy. The question then arises, Whose job is it to set this strategy? The answer is simple: the most senior leaders of the organization. Innovation cuts across just about every function. Only senior leaders can orchestrate such a complex system. They must take prime responsibility for the processes, structures, talent, and behaviors that shape how an organization searches for innovation opportunities, synthesizes ideas into concepts and product designs, and selects what to do.

There are four essential tasks in creating and implementing an innovation strategy. The first is to answer the question “How are we expecting innovation to create value for customers and for our company?” and then explain that to the organization. The second is to create a high-level plan for allocating resources to the different kinds of innovation. Ultimately, where you spend your money, time, and effort isyour strategy, regardless of what you say. The third is to manage trade-offs. Because every function will naturally want to serve its own interests, only senior leaders can make the choices that are best for the whole company.

The final challenge facing senior leadership is recognizing that innovation strategies must evolve. Any strategy represents a hypothesis that is tested against the unfolding realities of markets, technologies, regulations, and competitors. Just as product designs must evolve to stay competitive, so too must innovation strategies. Like the process of innovation itself, an innovation strategy involves continual experimentation, learning, and adaptation.