Reading: Lesson 5 - Analyzing and using the financial results—Accounts receivable turnover

Accounts receivable turnover is the number of times per year that the average

amount of accounts receivable is collected. To calculate this ratio divide net credit

sales, or net sales, by the average net accounts receivable (accounts receivable after

deducting the allowance for uncollectible accounts):

Ideally, average net accounts receivable should represent weekly or monthly

averages; often, however, beginning and end-of-year averages are the only amounts

available to users outside the company. Although analysts should use net credit sales,

frequently net credit sales are not known to those outside the company. Instead, they

use net sales in the numerator.

Generally, the faster firms collect accounts receivable, the better. A company with a

high accounts receivable turnover ties up a smaller proportion of its funds in accounts

receivable than a company with a low turnover. Both the company's credit terms and

collection policies affect turnover. For instance, a company with credit terms of 2/10,

n/30 would expect a higher turnover than a company with terms of n/60. Also, a

company that aggressively pursues overdue accounts receivable has a higher turnover

of accounts receivable than one that does not.

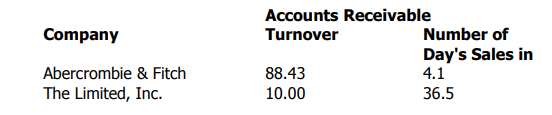

For example, we calculated these accounts receivable turnovers for the following

hypothetical companies:

We calculate the number of days' sales in accounts receivable (also called the

average collection period for accounts receivable) as follows:

This ratio measures the average liquidity of accounts receivable and gives an

indication of their quality. The faster a firm collects receivables, the more liquid (the

closer to being cash) they are and the higher their quality. The longer accounts

receivable remain outstanding, the greater the probability they never will be collected.

As the time period increases, so does the probability that customers will declare

bankruptcy or go out of business.

Based on 365 days, we calculated the number of days' sales for each of these

hypothetical companies:

These companies have collection periods ranging from 4.1 to 36.5 days. Assuming

credit terms of 2/10, n/30, one would expect the average collection period to be under

30 days. If customers do not pay within 10 days and take the discount offered, they

incur an annual interest rate of 36.5 percent on these funds. (They lose a 2 percent

discount and get to use the funds another 20 days, which is equivalent to an annual

rate of 36.5 percent.)

Having studied receivables and payables in this chapter, you will study plant assets

in the next chapter. These long-term assets include land and depreciable assets such as

buildings, machinery, and equipment.