Reading: Lesson 4 - Classified income statement

In preceding units, we illustrated the unclassified (or single-step) income statement. An

unclassified income statement has only two categories—revenues and expenses. In contrast, a

classified income statement divides both revenues and expenses into operating and nonoperating

items. The statement also separates operating expenses into selling and administrative expenses. A

classified income statement is also called a multiple-step income statement.

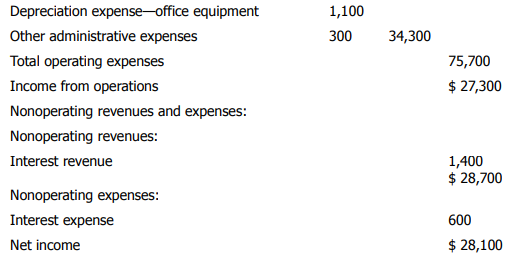

In Exhibit 39, we present a classified income statement for Hanlon Retail Food Store. This

statement uses the previously presented data on sales (Exhibit 35) and cost of goods sold (Exhibit 38), together with additional assumed data on operating expenses and other expenses and revenues. Note

in Exhibit 39 that a classified income statement has the following four major sections:

- Operating revenues.

- Cost of goods sold.

- Operating expenses

- Nonoperating revenues and expenses (other revenues and other expenses)

The classified income statement shows important relationships that help in analyzing how well the

company is performing. For example, by deducting cost of goods sold from operating revenues, you can

determine by what amount sales revenues exceed the cost of items being sold. If this margin, called

gross margin, is lower than desired, a company may need to increase its selling prices and/or decrease

its cost of goods sold. The classified income statement subdivides operating expenses into selling and

administrative expenses. Thus, statement users can see how much expense is incurred in selling the

product and how much in administering the business. Statement users can also make comparisons

with other years' data for the same business and with other businesses. Nonoperating revenues and

expenses appear at the bottom of the income statement because they are less significant in assessing

the profitability of the business.

Exhibit 39: Classified income statement for a merchandising company

Next, we explain the major headings of the classified income statement in Exhibit 39. The terms in

some of these headings are already familiar to you. Although future illustrations of classified income

statements may vary somewhat in form, we retain the basic organization.

- Operating revenues are the revenues generated by the major activities of the business—

usually the sale of products or services or both.

- Cost of goods sold is the major expense in merchandising companies. Note the cost of goods

sold section of the classified income statement in Exhibit 39. This chapter has already discussed

the items used in calculating cost of goods sold. Merchandisers usually highlight the amount by

which sales revenues exceed the cost of goods sold in the top part of the income statement. The

excess of net sales over cost of goods sold is the gross margin or gross profit. To express gross

margin as a percentage rate, we divide gross margin by net sales. In Exhibit 39, the gross margin

rate is approximately 39.3 per cent (USD 103,000/USD 262,000). The gross margin rate indicates

that out of each sales dollar, approximately 39 cents is available to cover other expenses and

produce income. Business owners watch the gross margin rate closely since a small percentage

fluctuation can cause a large dollar change in net income. Also, a downward trend in the gross

margin rate may indicate a problem, such as theft of merchandise. For instance, one Southeastern

sporting goods company, SportsTown, Inc., suffered significant gross margin deterioration from

increased shoplifting and employee theft.

- Operating expenses for a merchandising company are those expenses, other than cost of

goods sold, incurred in the normal business functions of a company. Usually, operating expenses

are either selling expenses or administrative expenses. Selling expenses are expenses a

company incurs in selling and marketing efforts. Examples include salaries and commissions of

salespersons, expenses for salespersons' travel, delivery, advertising, rent (or depreciation, if

owned) and utilities on a sales building, sales supplies used, and depreciation on delivery trucks

used in sales. Administrative expenses are expenses a company incurs in the overall

management of a business. Examples include administrative salaries, rent (or depreciation, if

owned) and utilities on an administrative building, insurance expense, administrative supplies

used, and depreciation on office equipment.

Certain operating expenses may be shared by the selling and administrative functions. For example,

a company might incur rent, taxes, and insurance on a building for both sales and administrative

purposes. Expenses covering both the selling and administrative functions must be analyzed and

prorated between the two functions on the income statement. For instance, if USD 1,000 of

depreciation expense relates 60 per cent to selling and 40 per cent to administrative based on the

square footage or number of employees, the income statement would show USD 600 as a selling

expense and USD 400 as an administrative expense.

- Nonoperating revenues (other revenues) and nonoperating expenses (other expenses)

are revenues and expenses not related to the sale of products or services regularly offered for sale

by a business. An example of a nonoperating revenue is interest that a business earns on notes receivable. An example of a nonoperating expense is interest incurred on money borrowed by the

company.

To summarize the more important relationships in the income statement of a merchandising firm

in equation form:

- Net sales = Gross sales - (Sales discounts + Sales returns and allowances).

- Net purchases = Purchases - (Purchase discounts + Purchase returns and allowances).

- Net cost of purchases = Net purchases + Transportation-in.

- Cost of goods sold = Beginning inventory + Net cost of purchases - Ending inventory.

- Gross margin = Net sales - Cost of goods sold.

- Income from operations = Gross margin - Operating (selling and administrative) expenses.

- Net income = Income from operations + Nonoperating revenues - Nonoperating expenses.

Each of these relationships is important because of the way it relates to an overall measure of

business profitability. For example, a company may produce a high gross margin on sales. However,

because of large sales commissions and delivery expenses, the owner may realize only a very small

percentage of the gross margin as profit. The classifications in the income statement allow a user to

focus on the whole picture as well as on how net income was derived (statement relationships).